Walmart Inc. (NYSE: WMT) has been one of the market’s steadier performers. Shares now trade near $102, close to a 52-week high of $106, after gaining on strong e-commerce growth, rising advertising revenues, and resilient consumer demand. But with valuation already stretched and competition remaining fierce, analysts are divided on where the stock heads next.

Recently, Walmart has been making big moves to modernize its operations. The company is rolling out AI-powered supply chain technology across U.S. stores to improve efficiency, while also expanding drone delivery through a partnership with Alphabet’s Wing. These initiatives highlight Walmart’s push to stay ahead in logistics and e-commerce, reinforcing why investors are closely watching its growth strategy.

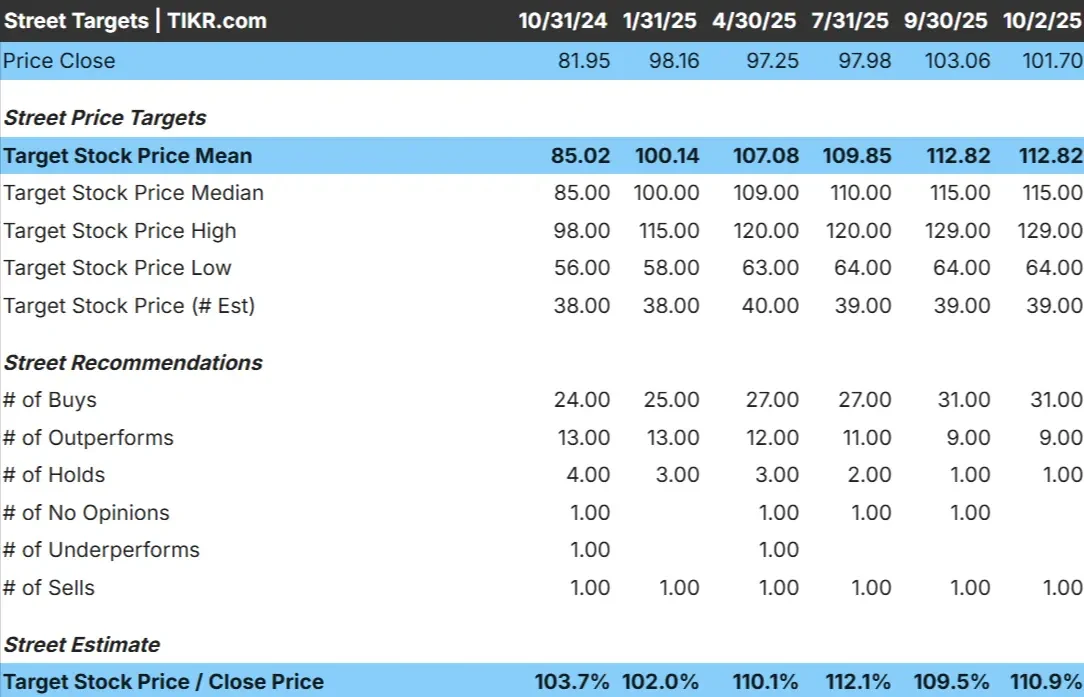

This article explores where Wall Street analysts think Walmart could trade by 2028. We have pulled together consensus targets and valuation models to get a sense of the stock’s potential trajectory. These figures reflect current analyst expectations and are not TIKR’s own predictions.

Unlock our Free Report: 5 AI compounders that analysts believe are undervalued and could deliver years of outperformance with accelerating AI adoption (Sign up for TIKR, it’s free) >>>

Analyst Price Targets Suggest Modest Upside

Walmart trades at about $102/share today. The average analyst price target is $113/share, which points to around 11% upside. Forecasts show a wide spread and reflect divided sentiment:

- High estimate: $129/share

- Low estimate: $64/share

- Median target: $115/share

- Ratings: 31 Buys, 9 Outperforms, 1 Hold, 1 Underperform, 1 Sell

It looks like analysts see modest gains, but the wide range of forecasts suggests conviction is weak. Some analysts believe Walmart’s scale and defensive position could push shares higher, while others think its premium multiple leaves little room to run.

For investors, the takeaway is that Walmart may deliver stability but not a breakout.

See analysts’ growth forecasts and price targets for Walmart (It’s free!) >>>

Walmart: Growth Outlook and Valuation

The company’s fundamentals show stability but limited growth:

- Based on analysts’ average estimates, revenue is expected to grow modestly

- Operating margins are forecasted to remain near 4–5%

- Shares currently trade at ~38x earnings, well above the 5-year average of ~26x

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a forward P/E of ~28x suggests ~$98/share by 2028

- That implies about a 4% decline from today’s price, or roughly –2% annualized returns

These forecasts suggest Walmart will continue to compound steadily, but much of this strength is already reflected in the current valuation. For investors, the key question is whether faster growth in e-commerce or advertising can provide enough of a boost to justify today’s premium multiple.

Value stocks like Walmart in as little as 60 seconds with TIKR (It’s free) >>>

What’s Driving the Optimism?

Walmart’s e-commerce and advertising businesses are growing quickly, creating new revenue streams that can offset its traditionally thin retail margins. Its Walmart+ subscription and grocery delivery service continue to expand, while international operations, especially in Mexico and India, provide steady long-term growth.

These strengths, combined with Walmart’s scale and pricing power, help explain why bulls see it as a reliable compounder. For investors, the optimism lies in Walmart’s ability to leverage technology and logistics to stay ahead of competitors.

Bear Case: Valuation and Competition

Despite the positives, Walmart’s valuation looks demanding relative to its growth profile. The stock already trades at a premium, which leaves little margin for error if results come in softer than expected.

Competition also remains fierce. Amazon continues to push deeper into groceries and logistics, while dollar stores and regional grocers compete aggressively on price. At the same time, higher labor and supply chain costs could weigh on profitability.

For investors, the risk is that Walmart’s defensive appeal is already reflected in the price. Without stronger growth or margin improvements, returns may struggle to keep pace with expectations.

Outlook for 2028: What Could Walmart Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a forward P/E of ~28x suggests Walmart could trade near $98/share by 2028.

That would represent a decline of about 4% from today’s level, or roughly –2% annualized returns.

For investors, Walmart looks like a safe and steady compounder, but upside appears modest. Unless the company outperforms on digital growth or margin expansion, returns may fall short of expectations.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Click here to sign up for TIKR and get your free copy of TIKR’s 5 AI Compounders report today.