Key Takeaways:

- Kimberly-Clark stock offers a rare mix of a 3.9% dividend yield and 53 straight years of dividend growth, supported by household brands like Huggies, Kleenex, and Cottonelle.

- While near-term growth has been pressured by inflation, our valuation model suggests the stock could have around 22% upside by the end of 2027 as earnings recover and multiples re-rate.

- With a strong dividend history, stable cash flows, and defensive product demand, Kimberly-Clark may appeal to income investors looking for yield, safety, and modest upside.

- Unlock our Free Report: 5 undervalued compounders with upside based on Wall Street’s growth estimates that could deliver market-beating returns (Sign up for TIKR, it’s free) >>>

Kimberly-Clark isn’t the most exciting stock at first glance.

But behind the scenes, the company dominates the global hygiene market with trusted brands like Huggies, Kleenex, Cottonelle, and Scott. These everyday products keep cash flowing even during downturns.

After facing inflation and margin headwinds in 2023, the stock now appears to trade at a slight discount, and analysts expect earnings to rebound in the years ahead.

For investors looking for a stable income stream with some upside, this overlooked blue-chip might be one of the safer dividend plays on the market today.

Analysts Think the Stock is Undervalued Today

Kimberly-Clark shares currently trade around $129, while our valuation model suggests the stock could be worth ~$158/share by the end of 2027.

That implies a potential total return of around 22% over the next 2.5 years, or about 8.3% annually, assuming earnings grow as projected and the valuation multiple improves slightly.

While it’s not the kind of upside that will make headlines, it’s still a decent return for a blue-chip dividend stock with 53 years of consecutive dividend growth.

Value Kimberly-Clark or any stock in less than 60 seconds with TIKR (It’s free) >>>

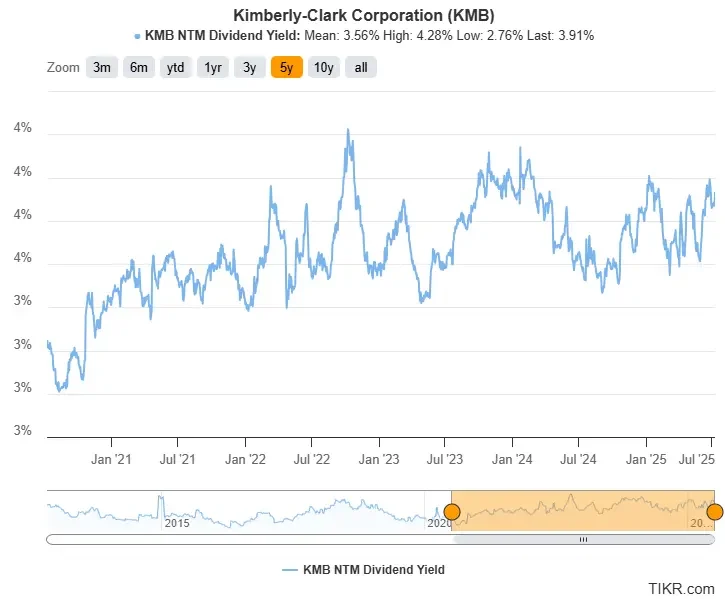

Kimberly-Clark’s Dividend Yield

Kimberly-Clark’s 3.9% dividend yield stands out, not just because it’s higher than usual, but because of what it says about the stock right now. It’s above the company’s 5-year average of 3.6%, which suggests the stock might be undervalued.

The reason the dividend yield is high is that the stock price has stayed just about flat over the past 3 years while the company kept raising its dividend. That’s led to the dividend yield rising over time and could be a signal that the market is underestimating a business with strong brands and reliable earnings.

Find high-quality dividend stocks that look even better than Kimberly-Clark today. (It’s free) >>>

Kimberly-Clark’s Dividend Safety

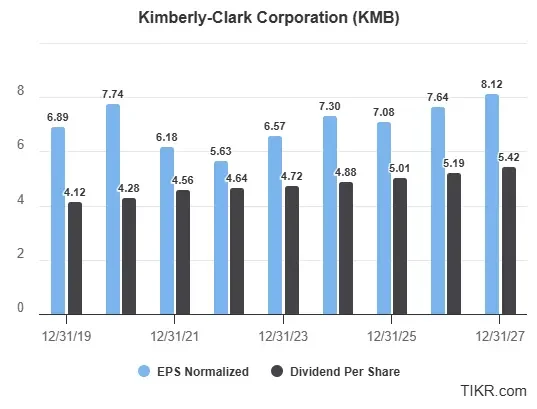

Kimberly-Clark’s most recent quarter showed continued strength, with earnings trending upward and dividend growth staying on track. For 2024, the company paid out $4.88 in dividends while generating $7.30 in normalized EPS, which puts the payout ratio near 67% and is a much healthier level than in prior years.

Despite inflation and supply chain noise, Kimberly-Clark has defended its margins through smart pricing and cost control. Management expects steady earnings growth through 2026, which should give the company room to keep raising its dividend.

The business is built around products people use every day. With staples like Huggies, Kleenex, and Cottonelle, demand stays consistent no matter what the economy looks like. That kind of resilience is what has powered 53 straight years of dividend increases and gives investors confidence looking forward.

See Kimberly-Clark’s full growth forecast and analyst estimates. (It’s free) >>>

TIKR Takeaway

Kimberly-Clark offers a 3.9% dividend yield, over 50 years of dividend growth, and a projected 22% upside based on our valuation model.

It’s a solid pick for conservative investors who value reliability over rapid growth.

The TIKR Terminal offers industry-leading financial data on over 100,000 stocks and was built for investors who think of buying stocks as buying a piece of a business.

Wall Street Analysts Are Bullish on These 5 Undervalued Compounders With Market-Beating Potential

TIKR just released a new free report on 5 compounders that appear undervalued, have beaten the market in the past, and could continue to outperform on a 1-5 year timeline based on analysts’ estimates.

Inside, you’ll get a breakdown of 5 high-quality businesses with:

- Strong revenue growth and durable competitive advantages

- Attractive valuations based on forward earnings and expected earnings growth

- Long-term upside potential backed by analyst forecasts and TIKR’s valuation models

These are the kinds of stocks that can deliver massive long-term returns, especially if you catch them while they’re still trading at a discount.

Whether you’re a long-term investor or just looking for great businesses trading below fair value, this report will help you zero in on high-upside opportunities.

Click here to sign up for TIKR and get our full report on 5 undervalued compounders completely free.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!