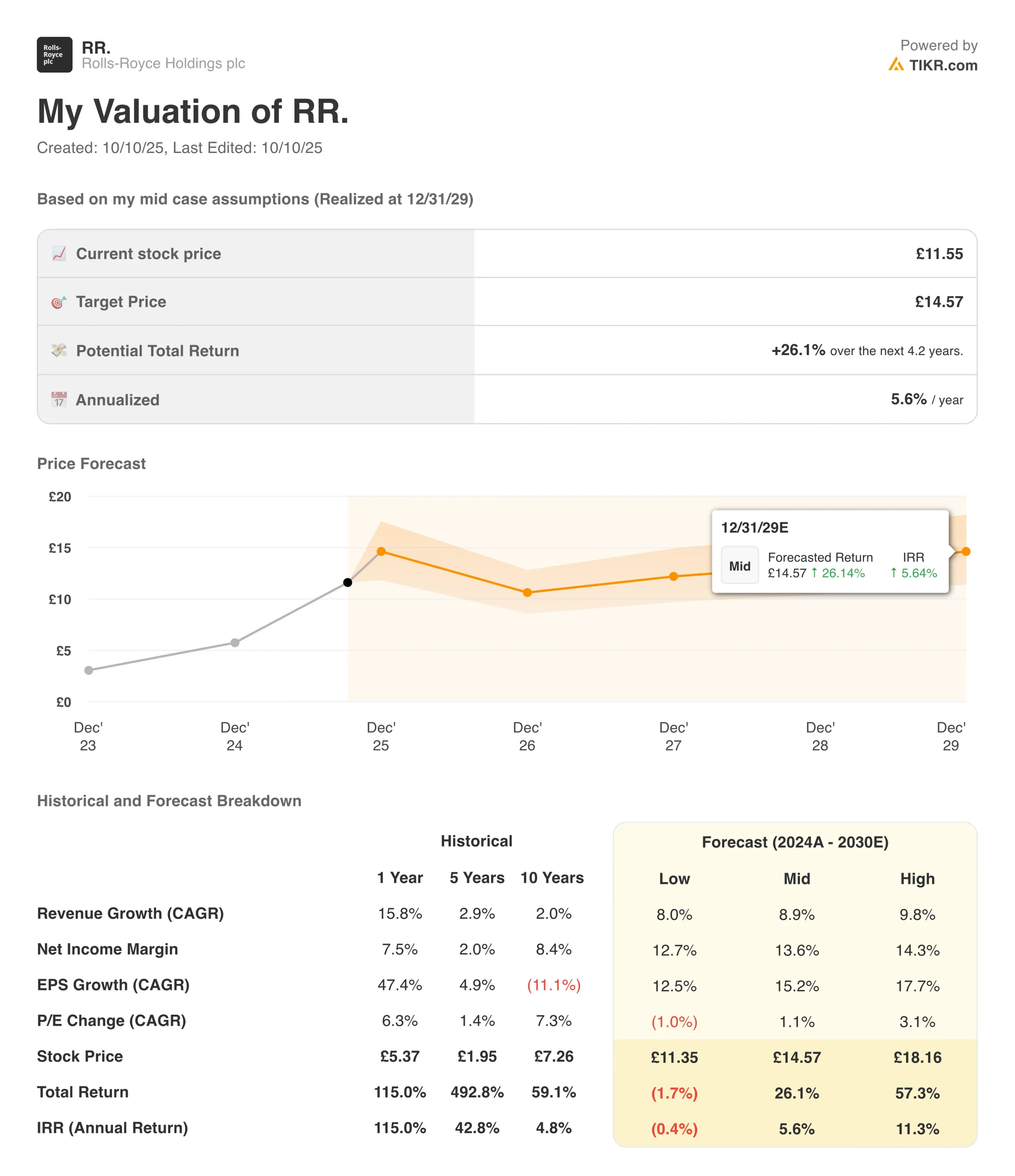

Rolls-Royce Holdings plc (RR.) has re-emerged as one of the FTSE 100’s standout performers in 2025, with shares up nearly 96% year-to-date. The company’s ongoing transformation, led by CEO Tufan Erginbilgiç, continues to reshape its balance sheet and operating model after years of volatility. Strong cost discipline, improved aftermarket profitability, and new efficiency measures have helped restore investor confidence in a business once synonymous with restructuring headlines.

The first half of 2025 marked a decisive shift. Revenue rose to £9.06 billion, up from £8.18 billion a year earlier, while underlying operating profit jumped 51% to £1.73 billion. That translated into an operating margin of 19.1%, a dramatic improvement over 14% in H1 2024, as the company’s cost-cutting, productivity, and pricing efforts began to compound. Free cash flow reached £1.58 billion, more than covering dividend payouts and supporting the ongoing £1 billion share-buyback programme.

Rolls-Royce’s guidance for the full year has been lifted accordingly: management now expects underlying operating profit of £3.1 billion–£3.2 billion and free cash flow of £3.0 billion–£3.1 billion. With net cash of £1.08 billion as of June 2025, compared to net debt just 12 months ago, the company has clearly entered a new financial era.

Company Snapshot

Founded in 1906, Rolls-Royce is a global leader in complex power and propulsion systems. The group operates through three main divisions: Civil Aerospace, Defence, and Power Systems. Its civil segment produces and services jet engines for long-haul aircraft such as the Airbus A350 and Boeing 787, while its defence arm powers military transport and combat aircraft, and its Power Systems division focuses on distributed energy and data-centre engines.

The company also plays a key role in the UK’s energy transition through Rolls-Royce SMR, its small modular nuclear reactor venture, which recently advanced to preferred supplier status for the UK government’s civil nuclear programme. These diversification efforts, alongside improved performance in aftermarket contracts, are helping Rolls-Royce evolve from a cyclical aerospace supplier into a more predictable, cash-generative industrial player.

See Roll-Royce’s full financial results & estimates (It’s free) >>>

Financial Story: Rolls-Royce

H1 2025 results highlighted exceptional progress across all divisions. Revenue climbed 11% year-on-year to £9.06 billion, underpinned by strong growth in Civil Aerospace and Power Systems. Operating profit rose to £1.73 billion, lifting margins to 19.1%, the company’s highest level in over a decade.

| Metric | Period | Value | YoY Change | Commentary |

|---|---|---|---|---|

| Revenue | H1 2025 | £9.06 billion | +10.7% | Driven by strong growth in Civil Aerospace and Power Systems |

| Underlying Operating Profit | H1 2025 | £1.73 billion | +51% | Margin expansion from cost savings and higher aftermarket volumes |

| Operating Margin | H1 2025 | 19.1% | +5.1 pp | Highest margin level in a decade |

| Profit Before Tax | H1 2025 | £1.69 billion | +63% | Reflects improved operating performance and FX tailwinds |

| Basic EPS | H1 2025 | 15.74 p | +76% | Boosted by stronger profitability and lower finance costs |

| Free Cash Flow | H1 2025 | £1.58 billion | +36% | Driven by higher LTSA inflows and improved working capital |

| Return on Capital | H1 2025 | 16.9% | +3.1 pp | Reflects greater efficiency and asset utilization |

| Net Cash Position | 30 Jun 2025 | £1.08 billion | vs. £0.48 billion FY 2024 | Transitioned from net debt to positive cash position |

| FY 2025 Guidance | — | £3.1 – £3.2 billion operating profit; £3.0 – £3.1 billion FCF | ↑ from prior £2.8 bn target | Raised on continued strength in Civil Aerospace margins |

Profit before tax reached £1.69 billion, up from £1.04 billion, while basic earnings per share nearly doubled to 15.74 pence. Free cash flow surged to £1.58 billion, driven by higher LTSA (long-term service agreement) contributions and improved engine flying-hour recovery, now at 109% of 2019 levels. Return on capital improved to 16.9% from 13.8%, reflecting both margin expansion and asset optimisation.

With net cash of £1.08 billion and a strengthened liquidity position of £8.5 billion, Rolls-Royce now enjoys the financial flexibility to sustain dividends, repurchase shares, and fund capital projects such as its SMR initiative without compromising its balance-sheet resilience.

1. Margin Expansion and Operational Efficiency

Rolls-Royce’s margin recovery is at the centre of its turnaround. Civil Aerospace, the group’s largest division, posted an operating margin of 24.9%, up from 18.0% a year ago, driven by improved aftermarket mix and pricing power. Defence margins held steady at 15.4%, while Power Systems expanded to 15.3% from 10.3%, benefitting from strong demand in energy and governmental markets.

Management credits these gains to productivity initiatives and better cost control across the supply chain. Even with lingering inflation in components and labour, efficiency programmes are mitigating price pressure. Investors will be watching closely to see if margins can hold above 20% as new production volumes ramp up in 2026.

2. Free Cash Flow and Balance-Sheet Strength

Free cash flow remains a cornerstone of the Rolls-Royce investment thesis. The £1.58 billion delivered in H1 2025 underscores the business’s newfound financial discipline and the benefits of its long-term service contracts. Civil Aerospace alone contributed £472 million of LTSA balance-sheet growth, while ongoing working-capital normalisation supported stronger cash conversion.

At mid-year, gross debt stood at £3.5 billion, but with £6.0 billion in cash and equivalents, the company’s net cash position of £1.08 billion represents a complete turnaround from the £475 million balance recorded at year-end 2024. This stability has allowed Rolls-Royce to pay an interim dividend of 4.5 pence and to return £400 million to shareholders through its buyback, with a full £1 billion targeted for completion by year-end.

Value stocks in less than 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

3. Strategic Growth and the Next Chapter

Beyond its financial rebound, Rolls-Royce is investing in long-term relevance. The company’s SMR (small modular reactor) programme is gaining regulatory traction, with management targeting profitability and positive free cash flow by 2030. In Civil Aerospace, new aftermarket contracts are being structured with higher recurring margins, while the Defence segment is positioned to capture rising spending across NATO and the Indo-Pacific region.

Power Systems continues to see robust demand from data-centre and government clients, making it one of Rolls-Royce’s most dependable growth pillars. Collectively, these drivers suggest the company’s mid-term targets, £3.6–£3.9 billion of underlying profit and £4.2–£4.5 billion of free cash flow, are achievable within the next two years if execution remains consistent.

The TIKR Takeaway

Rolls-Royce’s 2025 performance confirms that its multi-year transformation is delivering tangible results. The business is generating sustainable profit, expanding margins, and strengthening its balance sheet faster than even optimistic forecasts anticipated. Investor sentiment has followed: shares have nearly doubled this year, restoring Rolls-Royce’s standing as one of the FTSE 100’s most closely watched recovery plays.

Still, valuation risk is emerging. With shares up nearly 100% in 2025 and trading at over 18× forward earnings, much of the near-term optimism appears priced in. Continued progress on SMR development, defence growth, and long-cycle cash generation will determine whether Rolls-Royce can sustain this trajectory into 2026.

Should You Buy, Sell, or Hold Rolls-Royce?

Rolls-Royce’s financials show a company that has not only stabilised but is now thriving. Revenue and profit growth are running well ahead of historical averages, cash flow is solid, and return on capital is improving. The group’s strengthened balance sheet provides flexibility for both shareholder returns and reinvestment in strategic projects.

Yet investors should temper expectations. The company’s turnaround momentum is impressive, but its valuation already discounts much of the 2025 upside. Execution risk in large-scale programmes like SMR, along with continued supply-chain pressures, could limit margin expansion in 2026.

Rolls-Royce remains a compelling long-term industrial turnaround story, but after such a strong rally, the best approach for investors may be to hold existing positions and monitor FY 2025 results for signs of sustained free cash flow.

Quickly value any stock with TIKR’s powerful new Valuation Model (It’s free!) >>>

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie in the AI application layer, where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Click here to sign up for TIKR and get your free copy of TIKR’s 5 AI Compounders report today.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!