Palo Alto Networks Inc. (NASDAQ: PANW) has been one of the strongest performers in cybersecurity. The stock now trades near $204/share, up about 19% over the past year, as demand for cloud-native and AI-driven security continues to accelerate. Surpassing $3 billion in annual recurring revenue and earning recognition as a Leader in Forrester’s SASE Wave (Q3 2025) have reinforced its market leadership. But with competition heating up and valuation already elevated, investors are divided on what comes next.

In July, Palo Alto made headlines by agreeing to acquire CyberArk in a $25 billion cash-and-stock deal, offering $45 in cash plus 2.2005 shares of PANW stock per CyberArk share, representing a premium of about 26% over the recent trading average. In its latest fiscal Q2 2025 report, Palo Alto posted $2.3 billion in revenue, up 14% year over year, and Next-Generation Security ARR climbed 37% to $4.8 billion. These moves underline Palo Alto’s ambition to expand from network security into identity and privileged access, while showing investors that its growth strategy remains aggressive.

This article explores where Wall Street analysts think Palo Alto could trade by 2028. We have reviewed consensus targets, growth forecasts, and valuation models to outline the stock’s potential path. These figures reflect current analyst expectations and are not TIKR’s own predictions.

Unlock our Free Report: 5 AI compounders that analysts believe are undervalued and could deliver years of outperformance with accelerating AI adoption (Sign up for TIKR, it’s free) >>>

Analyst Price Targets Suggest Limited Near-Term Upside

Palo Alto trades at about $204/share today. The average analyst price target is $215/share, which points to around 6% upside over the next year. Forecasts show a wide spread and reflect divided sentiment:

- High estimate: ~$245/share

- Low estimate: ~$131/share

- Median target: ~$224/share

- Ratings: majority Buys and Outperforms, very few Sells

Analysts see only modest room for near-term gains, and the wide range of targets suggests conviction is mixed. The takeaway is that expectations are already high, and Palo Alto may need to outperform on growth or margins to break meaningfully higher. For investors, this means the stock looks more attractive for those with a long-term horizon than for those focused on short-term price movements.

See analysts’ growth forecasts and price targets for Palo Alto (It’s free!) >>>

Palo Alto Networks: Growth Outlook and Valuation

The company’s fundamentals remain strong, with growth and profitability both expected to improve:

- Revenue projected to grow at a 13.8% CAGR over the next two years

- EPS compounding at about 13.4% over the same period

- Operating margins expected to rise from 27.3% today to 30.2% by 2028

- Shares trade at ~53.6x forward earnings, reflecting a premium valuation

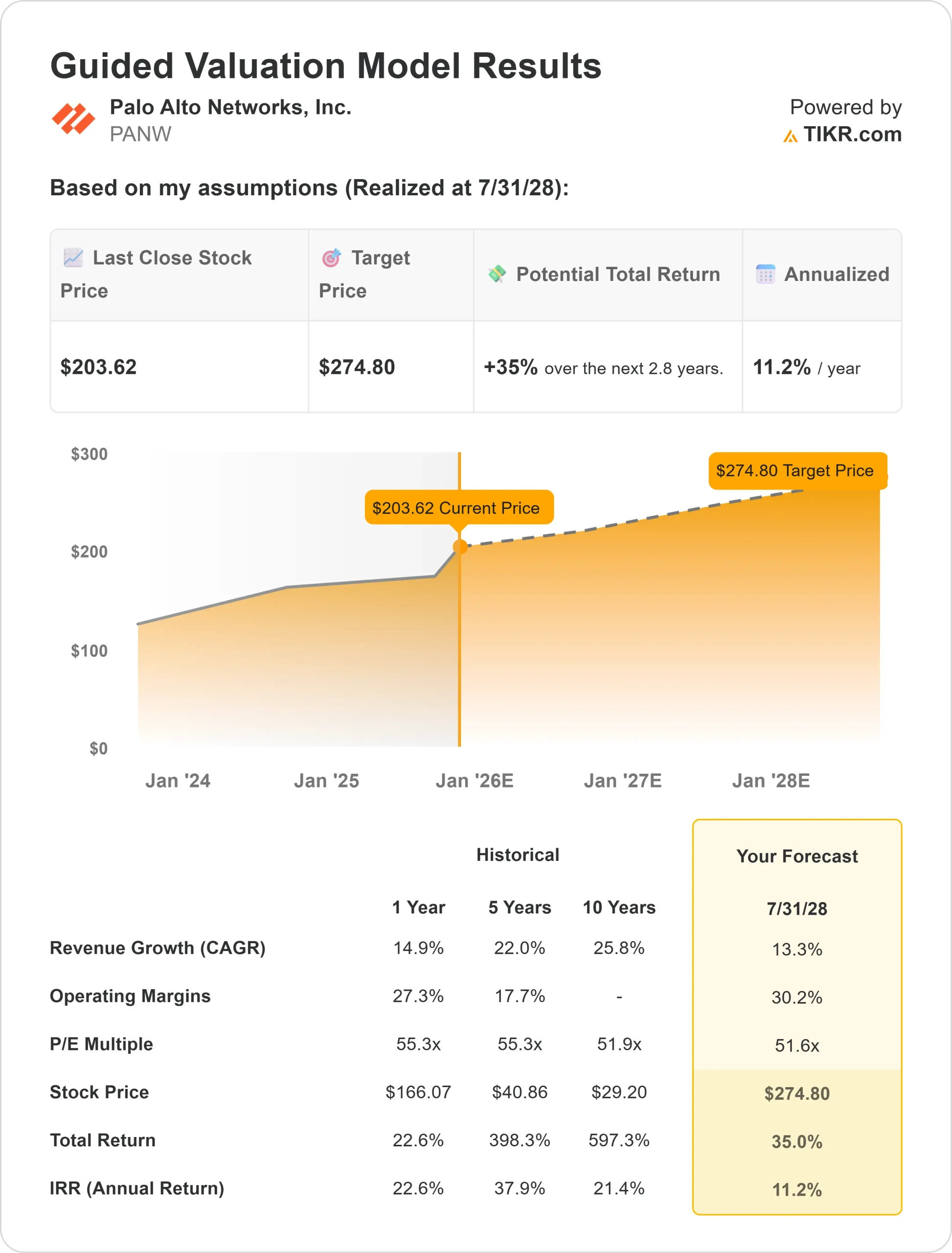

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 53.6x forward P/E suggests ~$274.80/share by July 2028

- That implies ~35% upside in total, or ~11% annualized returns

These numbers indicate Palo Alto has the ability to compound steadily, supported by margin expansion and recurring revenue growth.

The valuation remains elevated, but that reflects investor confidence in its execution and industry leadership. For investors, the real upside will come if the company beats expectations on AI-driven adoption and cross-platform growth.

Value stocks like Palo Alto in as little as 60 seconds with TIKR (It’s free) >>>

What’s Driving the Optimism?

Palo Alto has continued to grow as cybersecurity spending accelerates worldwide. Operating margins are also on an upward trajectory. Analysts project them to expand from 27.3% today to 30.2% by 2028, which shows efficiency gains as scale kicks in. For a business that already commands premium pricing, expanding margins add credibility to the bull case. Combined with a broad product portfolio and global enterprise relationships, these factors suggest Palo Alto can maintain its leadership position in cybersecurity.

For investors, this paints a picture of a company with staying power. As cyberattacks become more sophisticated and enterprises accelerate their shift to cloud and AI solutions, Palo Alto is positioned to capture that demand and compound revenue at double-digit rates.

Bear Case: Valuation and Competition

Despite the positives, Palo Alto’s valuation looks demanding compared to many peers. Shares currently trade at about 53.6x forward earnings, a multiple that assumes steady growth and strong execution. If growth slows, even modestly, the stock could see pressure as multiples compress.

Competition is another risk. CrowdStrike, Zscaler, and Microsoft are aggressively expanding into AI-driven cybersecurity, putting pressure on Palo Alto’s market share and pricing. In addition, large enterprise deals are sensitive to the broader economic cycle, meaning prolonged macro headwinds could delay contracts or shrink budgets.

For investors, the bear case is that Palo Alto’s stock already prices in near-perfect execution. Any stumble on growth, margins, or competitive positioning could lead to sharp underperformance. In other words, the upside is clear, but the margin for error is thin.

Outlook for 2028: What Could Palo Alto Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 53.6x forward P/E suggests Palo Alto could trade near $275/share by July 2028. That would represent about a 35% gain from today’s level, or roughly 11% annualized returns. The scenario assumes consistent low-teens revenue growth, margin expansion toward the low-30s, and stable valuation multiples.

While this represents healthy performance, the outlook already includes a fair degree of optimism. Stronger upside would require Palo Alto to beat expectations on AI adoption, expand its cross-selling opportunities, or capture faster-than-expected growth in cloud security. Without that, returns may be steady but not spectacular.

For investors, Palo Alto looks like a solid long-term compounder in cybersecurity. It may not deliver explosive growth from here, but its recurring revenue scale and expanding profitability make it a reliable candidate for portfolios focused on durable, long-term growth.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Click here to sign up for TIKR and get your free copy of TIKR’s 5 AI Compounders report today.