Key Takeaways:

- The 2-Minute Valuation Model values KVUE stock at $25 per share in 2 years.

- That’s only a 4% upside from today’s price of $24.

- The stock trades at 20.9x forward earnings, which is nearly the highest valuation multiple the stock has traded at.

- The stock would be more attractive at a $20/share entry price and could deliver 12% annual returns at that entry price.

- Get accurate financial data on over 100,000 global stocks for free on TIKR >>>

Following its spinoff from Johnson & Johnson in 2023, Kenvue (KVUE) has established itself as the world’s largest pure-play consumer health company.

As the owner of iconic brands like Tylenol, Listerine, Band-Aid, and Neutrogena, Kenvue offers investors exposure to a portfolio of trusted consumer products with steady, if unspectacular, growth potential.

Despite the quality of the underlying business, the stock looks overvalued today and doesn’t look to offer attractive returns today.

Instead, let’s look at why paying $20/share might be a reasonable price to pay for the stock.

Find stocks that are even better than Kenvue today with TIKR. (It’s free!) >>>

What is the 2-Minute Valuation Model?

Three core factors drive a stock’s long-term value:

- Revenue Growth: How big the business becomes.

- Margins: How much the business earns in profit.

- Multiple: How much investors are willing to pay for a business’s earnings.

Our 2-Minute Valuation Model uses a simple formula to value stocks:

Expected Normalized EPS * Forward P/E ratio + Expected Dividends = Expected Share Price

Revenue growth and margins drive a company’s long-term normalized earnings per share (EPS), and investors can use a stock’s long-term average P/E multiple to get an idea of how the market values a company.

Why This Blue-Chip Dividend Stock Looks Fully Valued

Forecast

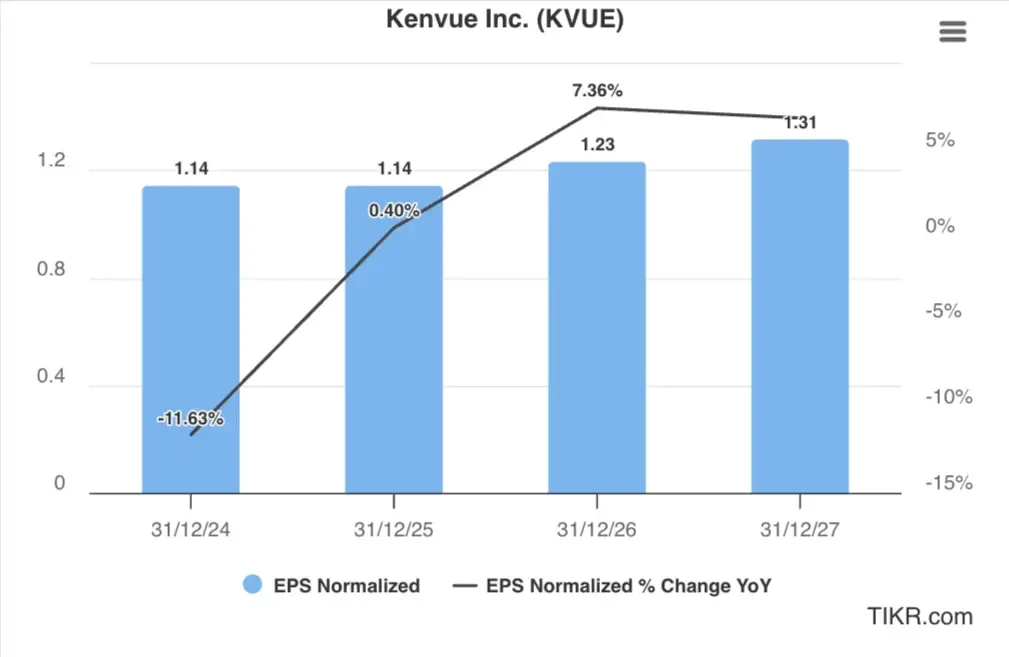

Kenvue is projected to deliver reliable but modest earnings growth over the next three years. This growth trajectory suggests the company is still finding its footing following the spinoff.

While earnings declined in 2024, they will return to mid-single-digit growth in the next three years. While not exciting, this pattern reflects the stable and mature nature of Kenvue’s consumer health products, which typically deliver consistent rather than explosive growth.

For this reason, we’ll assume that Kenvue reaches $1.30 in EPS for 2027.

Future earnings growth for the blue-chip healthcare giant is likely to be driven by:

- Portfolio of Essential Brands: Kenvue owns dozens of household name brands that consumers trust and purchase regularly, regardless of economic conditions.

- Defensive Business Model: Consumer health products are recession-resistant, providing earnings stability during economic downturns.

- Global Distribution Network: The company benefits from an extensive global reach, with products sold in over 165 countries, limiting regional risk.

- Category Leadership: Many Kenvue’s brands hold #1 or #2 positions in their respective categories, giving the company pricing power and shelf space advantages.

Additionally, Kenvue offers shareholders a dividend yield of 3.4%. Analysts tracking the stock expect annual dividend payouts to increase from $0.81 per share in 2024 to $0.90 per share in 2027.

View KVUE’s full analyst estimates (It’s free) >>>

Is KVUE Stock Overvalued Right Now?

KVUE stock is trading above its 1-year average P/E multiple, which means the current valuation multiple reflects that investors are paying a premium for Kenvue’s portfolio of well-known brands.

Today, the stock trades at 21 times expected earnings. We’ll use a forward P/E multiple of 18x for our valuation, which seems more reasonable given the business’s mid-single-digit expected earnings growth.

Fair Value of KVUE Stock

Using our 2-Minute Valuation Model and applying a conservative approach:

- Conservative 2027 EPS estimate: $1.30

- Conservative forward P/E multiple: 18x

- Expected dividends in the next 2 years: $2

Expected Normalized EPS ($1.30) * Forward P/E ratio (18x) + Dividends ($2) = Expected Share Price ($25)

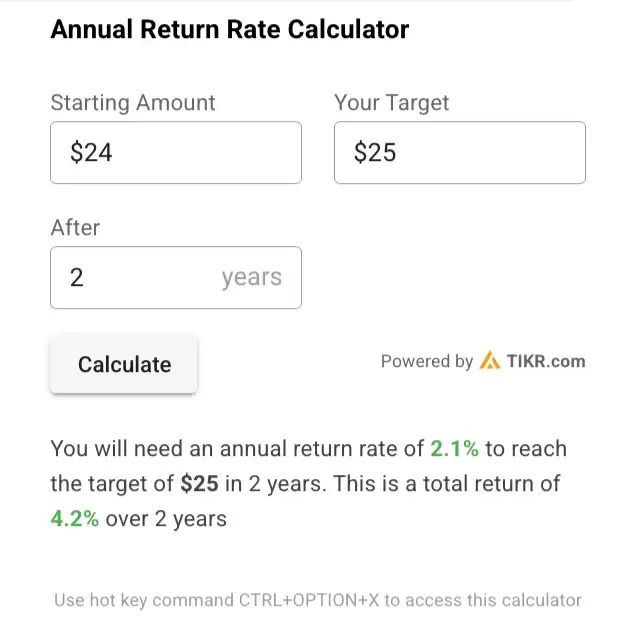

The 2-year expected KVUE stock price we would get from this valuation is $25 per share.

With the stock currently trading near $24, that implies just a 4% total return over two years, or about 2% per year.

That’s well below the market’s historical average of 10% annual returns, and this estimate already factors in dividends.

Here’s what we think might be a better price to pay for Kenvue to get attractive returns.

Value stocks like Kenvue quicker with TIKR (It’s free, no card required) >>>

What Would Be a Good Price to Pay for Kenvue Stock Today?

The right price to pay for Kenvue depends on the kind of return you’re looking for.

The broader market has historically returned around 8–10% per year, so let’s reverse-engineer a price that could offer similar or better returns.

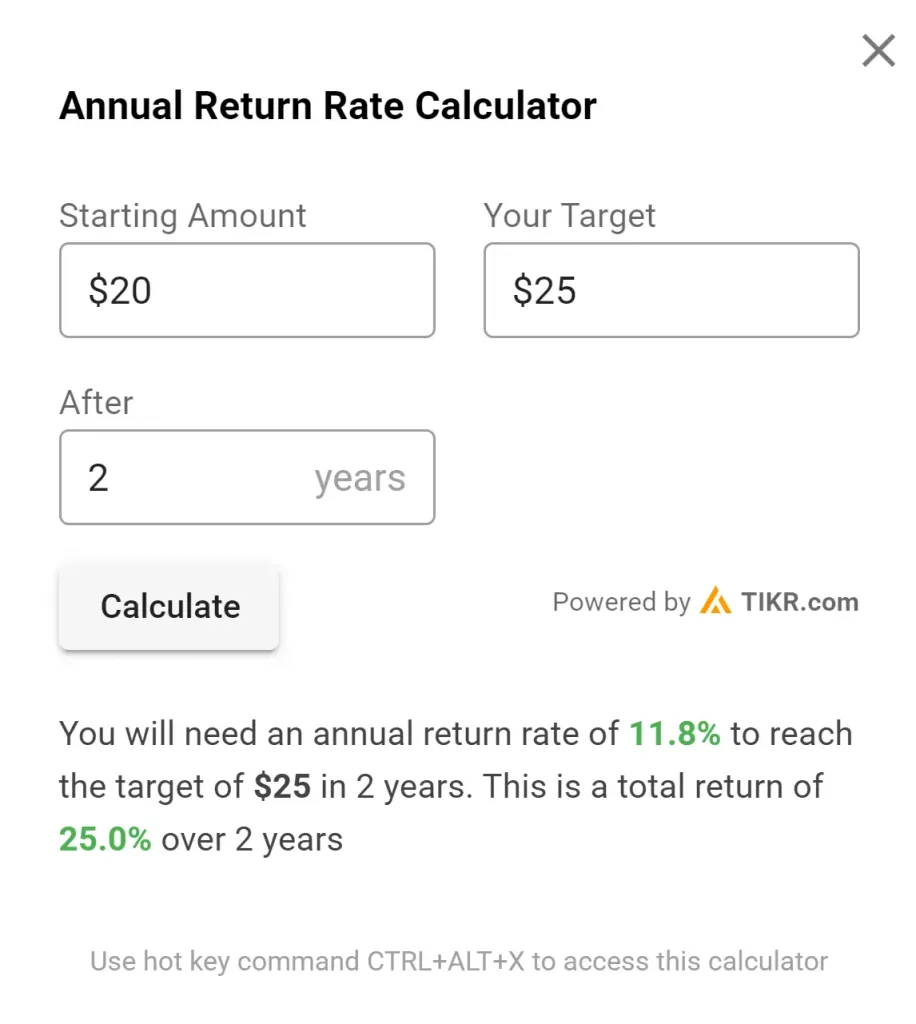

If Kenvue were to trade at $20 per share, it could generate roughly 12% annual returns over the next two years, including dividends. That would make it a much more appealing opportunity.

The stock dipped below $21 back in February, so a return to those levels wouldn’t be out of the question. Buying Kenvue at a $20 share price or less would offer much more attractive returns.

What is the Target Price for KVUE Stock?

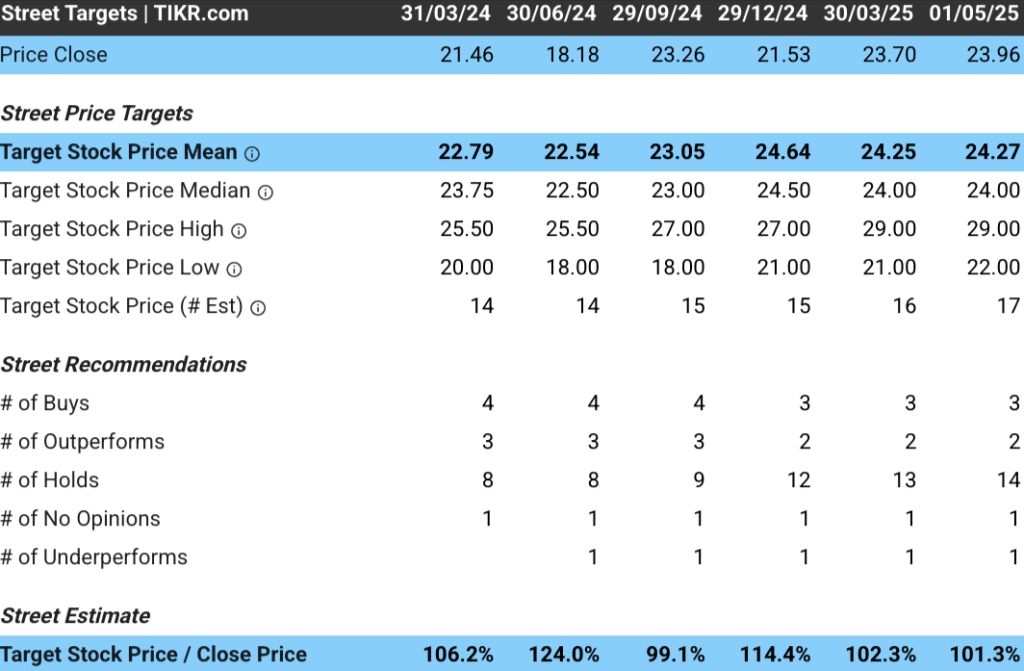

Analysts have an average price target of around $24 per share for KVUE stock, indicating they see about 1% upside for the stock from its current share price:

Risks to Consider

Investors should be aware of several risks that come with this stock as a pharmaceutical company:

- Private Label Competition: Increasing competition from store brands and private label alternatives could pressure margins and market share.

- Limited Organic Growth Potential: The mature nature of many of Kenvue’s categories means the company must rely more on price increases than volume growth.

- Regulatory Scrutiny: Consumer health products face ongoing regulatory oversight, with potential for increased scrutiny of ingredients, claims, and marketing practices.

- Innovation Challenges: Kenvue may face challenges in product innovation as a standalone company with limited R&D resources compared to its former parent.

- Elevated Valuation: The current premium valuation leaves little room for error and could lead to underperformance if growth targets are missed.

These risks help explain the stock’s compressed valuation multiple, as the market discounts future growth potential against these headwinds.

TIKR Takeaway

Kenvue represents a high-quality consumer health company with trusted brands, but at current prices, it offers an unattractive investment proposition.

The stock’s premium valuation (20.9x forward earnings) appears overvalued relative to its historical average and modest growth outlook, creating a poor risk-reward profile for new investors.

With projected annual returns of just 2.1% compared to the S&P 500’s historical average of 10%, KVUE stock offers inadequate compensation for the capital invested.

What are some better stocks to buy today than Kenvue? Use TIKR to find stocks that are undervalued compared to analyst price targets with strong outlooks.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!