Key Takeaways for Norwegian Cruise Line Stock as of July 2026

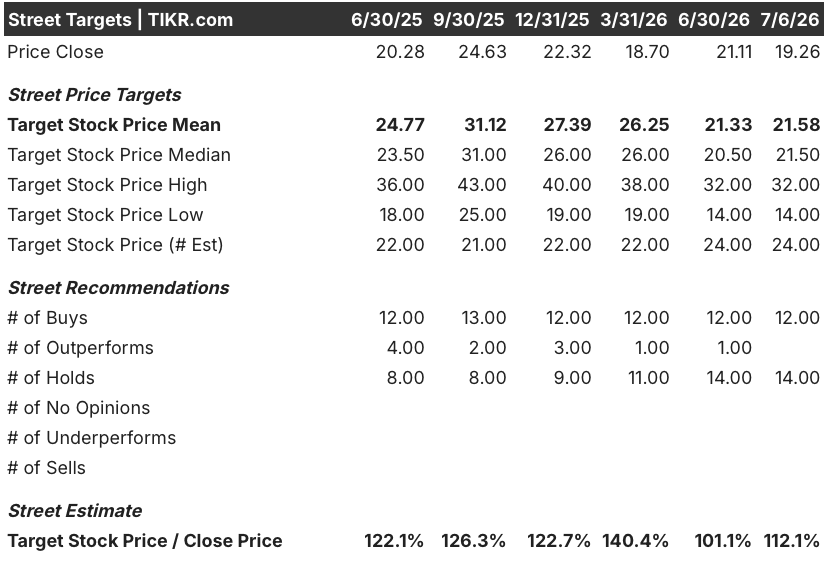

- Twelve buy ratings, fourteen holds, and zero sells put the mean target at $22, a 12% gap to Norwegian Cruise Line Holdings stock’s current $19.

- TIKR’s mid-case model prices Norwegian Cruise Line Holdings stock at $31 by December 2030, working out to 63% total return and 11% annualized.

- Trading near its 52-week low of $15, the stock still looks undervalued against an EBITDA base TIKR’s own estimates show swinging back to 16% growth by mid-2027.

- With fuel costs easing, Citi raised its NCLH target to $25 from $21.

Norwegian Cruise Line Stock Beats on Q1 EBITDA While Cutting Full-Year Guidance

Norwegian Cruise Line Holdings (NCLH) posted an 18% jump in Q1 2026 adjusted EBITDA to $533 million on May 4, even as revenue of $2.33 billion missed the Street’s $2.36 billion estimate. That gap between a cost-driven profit beat and a demand-driven revenue miss now defines the setup for Norwegian Cruise Line Holdings stock.

That cost discipline traces to $125 million in annualized SG&A savings CEO John Chidsey’s team identified within his first 90 days in the role. Combined with prior shipboard cuts, the company has now banked close to $400 million in cumulative savings since 2023.

Even so, the same call brought a sharp reset. NCLH cut full-year 2026 adjusted EPS guidance to $1.45 to $1.79 from a prior $2.38, and lowered adjusted EBITDA guidance to $2.48 billion to $2.64 billion.

On the Q1 earnings call, CEO John Chidsey framed the turnaround in blunt terms: “We have the assets, we have the brands, and now we have the focus.” That focus, he said, centers on culture and execution as much as costs, with early wins already visible in the EBITDA line.

Fuel remains the swing factor beneath the cost story. NCLH now models annual fuel expense near $800 million, though costs would run about 6% lower at forward-curve pricing.

That backdrop has since eased. Citi raised its price target on Norwegian Cruise Line Holdings stock to $25 from $21 on June 16, citing falling fuel costs and easing Middle East tensions across the cruise sector.

Most recently, Norwegian named Lee Applbaum, former global CMO at Patrón and Bacardi, as chief marketing officer effective July 6. His mandate: fix the demand-generation problems management blamed for 2026’s booking shortfall.

Wall Street Splits Between Buy and Hold on NCLH Stock

Twelve analysts rate Norwegian Cruise Line Holdings stock a buy and fourteen rate it a hold, with no sell ratings currently on record. The mean target sits at $22, about 12% above the stock’s current $19, while estimates range from a high of $32 to a low of $14.

Citi’s move to $25 from $21 in June was among the more constructive revisions, landing closer to the mean than the more cautious holds still anchored near current levels.

Wall Street Expects NCLH Stock’s EBITDA to Rebound 16% by Mid-2027

Norwegian Cruise Line Holdings stock’s anchor metric already turned first: adjusted EBITDA grew 17.6% year over year in the quarter ended March 31, reaching $533 million even as revenue missed estimates.

The Street models a steeper give-back from here, projecting EBITDA down 9% in the June quarter, 14% in September, and 8% in December as the guidance cut and European booking weakness work through the base.

That decline is expected to bottom in March 2027, with EBITDA down just 3% year over year, before growth returns at 16% in the June 2027 quarter to $730 million.

That $730 million print is the number to watch. A result anywhere close confirms the cost savings are compounding on schedule, while a miss would suggest the 2026 reset runs longer than a single year.

TIKR’s Model Points to $31 for Norwegian Cruise Line Holdings Stock by December 2030

TIKR’s mid-case model values Norwegian Cruise Line Holdings stock at $31 by December 2030, implying a 63% total return from the current price of $19, or 11% annualized over 4.5 years.

That return places the stock among the cheaper turnaround stories in travel, one where EBITDA recovery sits as a supporting data point inside a broader re-rating built on margin expansion, deleveraging, and moderating capital intensity.

$125 million in annualized SG&A savings and a newbuild schedule that thins out sharply after 2027 both feed the same margin recovery path TIKR’s model assumes.

Great Stirrup Cay’s water park, opening this summer, adds a further onboard-spend lever once marketing catches up.

Should You Invest in Norwegian Cruise Line Holdings?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Norwegian Cruise Line Holdings stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Norwegian Cruise Line Holdings alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze NCLH stock on TIKR for Free →