Key Takeaways:

- Bath & Body Works is executing a comprehensive transformation strategy focused on digital elevation, efficacy messaging, and strategic distribution expansion under new CEO Daniel Heaf.

- BBWI could reasonably reach $34/share by January 2030, based on our valuation assumptions.

- This implies a total return of 38% from today’s price of $25/share, with an annualized return of 8% over the next 4.3 years.

Bath & Body Works (BBWI) is repositioning itself as a modern personal care and home fragrance leader through strategic initiatives addressing digital experience gaps, product messaging clarity, and customer acquisition challenges across younger demographic segments and alternative distribution channels.

Bath & Body Works serves consumers globally through its comprehensive retail platform, which spans over 1,900 North American stores, international partnerships, and digital channels, all supported by vertically integrated domestic manufacturing capabilities and a loyalty program with 39 million active members.

Core offerings include body care products like moisturizers and shower gels, home fragrances such as candles and room sprays, and soaps and sanitizers.

These are delivered through experiential retail stores, e-commerce platforms, and emerging wholesale partnerships targeting college campuses and strategic retail locations.

The specialty retailer delivered fiscal 2025 second-quarter revenue of $1.5 billion, a 1.5% year-over-year increase, with full-year guidance calling for 1.5-2.7% growth, indicating stabilization despite near-term margin pressures from tariffs and transformation investments.

Bath & Body Works demonstrates focused execution on strategic transformation under the leadership of CEO Daniel Heaf and CFO Eva Boratto.

BBWI launched three “no regret” initiatives within Heaf’s first week, which include digital platform elevation, product efficacy amplification, and expanded distribution.

It plans to enter 600 college bookstores, reaching seven million young consumers, while strengthening its balance sheet position with plans to deploy $400 million in share repurchases.

Today, BBWI stock trades almost 70% below its all-time high. Let’s see if the retail operator can recover over the next 12 months and beyond.

See analysts’ full growth forecasts and estimates for Bath & Body Works stock (It’s free) >>>

What the Model Says for BBWI Stock

We analyzed the upside potential for Bath & Body Works stock using valuation assumptions based on its transformation execution capabilities and market opportunities across digital enhancement, customer acquisition, and strategic distribution expansion.

Analysts recognize an opportunity ahead for BBWI stock given its iconic brand strength, operational infrastructure advantages, and systematic approach to addressing growth constraints while maintaining exceptional profitability metrics in the specialty retail market.

Bath & Body Works’ vertically integrated supply chain provides competitive advantages, while the strategic initiatives validate that focused execution can drive customer acquisition and revenue acceleration in the expanding personal care and home fragrance landscape.

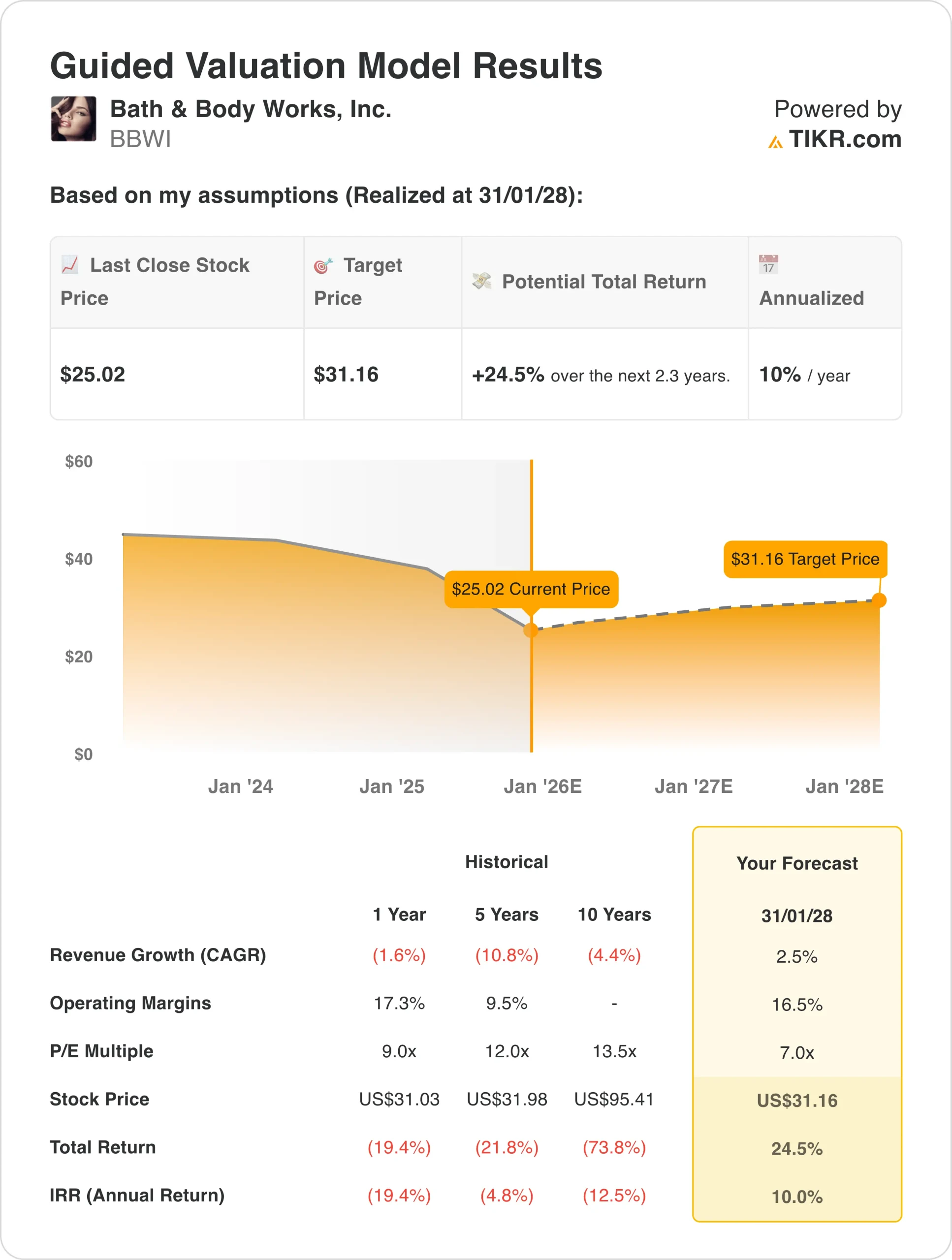

Based on estimates of 2.3% annual revenue growth, 10% net income margins, and a normalized P/E valuation multiple of 7x, the model projects BBWI stock could rise from $25/share to $34.50/share.

That would be a 24.5% total return, or a 10% annualized return over the next 2.3 years.

Value BBWI stock with TIKR’s Valuation Model today for FREE (Find undervalued stocks fast) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for BBWI stock:

1. Revenue Growth: 2.3%

Bath & Body Works delivered modest fiscal 2025 first-half performance, with revenue growth stabilizing after several quarters of declines driven by cautious consumer spending and new customer acquisition challenges.

Growth drivers include digital platform improvements launching September-October 2025, expanded distribution through college bookstores and strategic wholesale partnerships, amplified product efficacy messaging resonating with younger consumers, and international expansion through franchise partners with system-wide retail sales up 9% in recent quarters.

We used a 2.3% forecast, reflecting Bath & Body Works’ realistic path to consistent mid-single digit growth as transformation initiatives scale while balancing near-term consumer headwinds and competitive dynamics in the personal care and home fragrance markets.

2. Operating Margins: 10%

In fiscal 2025, Bath & Body Works’ net income margins face pressure from $85 million in tariff impacts, strategic investments in digital capabilities and technology infrastructure, and higher healthcare costs, while it navigates transformation investments under new leadership.

BBWI targets sustainable margin improvement through reduced promotional intensity and higher average unit retail prices, operational efficiency gains from fuel-for-growth cost reduction initiatives, and leverage from Beauty Park’s vertically integrated manufacturing as revenue growth accelerates.

We used 10% net margins, reflecting normalization from recent 10.1% trailing levels as the company balances transformation investments with disciplined cost management and gradual pricing power recovery in core categories.

3. Exit P/E Multiple: 7x

Bath & Body Works stock trades at approximately 7x earnings, representing a significant discount to its 10-year historical average of 13.5x, reflecting market skepticism about growth trajectory and transformation execution risks.

We maintain conservative valuation levels at 7x, considering uncertainties in leadership execution, challenges in acquiring new customers that require proof points, and the competitive intensity in specialty retail, which offsets Bath & Body Works’ brand strength and profitability advantages.

Long-term competitive advantages from supply chain integration, store network scale, and brand equity should support valuation expansion, as they demonstrate consistent growth and successful customer acquisition among younger demographics.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Different scenarios for BBWI stock through 2030 show varied outcomes based on transformation execution and consumer response to strategic initiatives: (these are estimates, not guaranteed returns):

- Low Case: Digital improvements underperform, new customer acquisition stalls → 3% annual returns

- Mid Case: Successful digital enhancement and moderate customer growth → 8% annual returns

- High Case: Strong new customer momentum and reduced promotional dependency → 11% annual returns

Even in the conservative case, BBWI stock offers reasonable returns supported by strong free cash flow generation and defensive positioning through domestic supply chain advantages and affordable luxury price points during economic uncertainty.

The upside scenario for BBWI stock could deliver attractive performance if it can successfully attract younger consumers while scaling alternative distribution and achieving reduced promotional intensity through stronger brand positioning and product innovation.

See analysts’ growth forecasts and price targets for any stock (It’s free!) >>>

Wall Street Analysts Are Bullish on These 5 Undervalued Compounders With Market-Beating Potential

TIKR just released a new free report on 5 compounders that appear undervalued, have beaten the market in the past, and could continue to outperform on a 1-5 year timeline based on analysts’ estimates.

Inside, you’ll get a breakdown of 5 high-quality businesses with:

- Strong revenue growth and durable competitive advantages

- Attractive valuations based on forward earnings and expected earnings growth

- Long-term upside potential backed by analyst forecasts and TIKR’s valuation models

These are the kinds of stocks that can deliver massive long-term returns, especially if you catch them while they’re still trading at a discount.

Whether you’re a long-term investor or just looking for great businesses trading below fair value, this report will help you zero in on high-upside opportunities.

Click here to sign up for TIKR and get your free copy of TIKR’s 5 AI Compounders report today.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!