Key Takeaways:

- CNH Industrial is navigating the agricultural downturn by cutting production and reducing dealer inventory, setting up for a 2026 recovery.

- CNH stock could reasonably reach $15/share by December 2029, based on our valuation assumptions.

- This implies a total return of 51% from today’s price of $10/share, with an annualized return of 10% over the next 4.2 years.

CNH Industrial (CNH) makes tractors, combines, and construction equipment for farmers and builders worldwide. The company is currently navigating a challenging agricultural cycle, but management is taking the right steps to emerge stronger on the other side.

CNH operates two main brands in agriculture, Case IH and New Holland, plus a Construction equipment division.

It also runs CNH Industrial Capital, which finances equipment purchases for customers. Manufacturing happens across North America, Europe, Latin America, and the Asia Pacific.

The product lineup includes everything from massive tractors and combines for large farms to mid-sized tractors for diverse operations. More recently, CNH has been building out FieldOps, its precision agriculture technology platform that helps farmers manage their operations more efficiently.

In the second quarter of 2025, CNH delivered revenue of $4.7 billion, down 14% from last year. This wasn’t a surprise, as management had intentionally cut production to help dealers work through excess inventory.

Under CEO Gerrit Marx and new CFO Jim Nickolas, CNH is focused on getting dealer inventories back to healthy levels by year-end.

The team cut production 12% below last year’s pace and helped dealers reduce ag inventory by over $200 million in just one quarter. They’re also rolling out new technology, including a partnership with Starlink, announced in May, that brings satellite internet connectivity to farm equipment.

CNH Industrial stock went public in 2011 and has since returned less than 10% to shareholders, even if we adjust for dividend reinvestments.

Here’s why we believe CNH Industrial stock is poised to deliver solid returns through 2029, driven by the recovery of farming markets and the company’s execution of quality and technology improvements.

See analysts’ full growth forecasts and estimates for CNH stock (It’s free) >>>

What the Model Says for CNH Stock

We examined CNH Industrial’s upside potential based on our current position in the agricultural cycle and factors within management’s control, such as inventory management, quality improvements, and technology development.

CNH is going through the worst part of the agricultural cycle in 2025 as dealer inventories are too high, farmers aren’t buying much equipment, and production is running well below normal.

However, the company is making smart moves on technology with the Starlink partnership and FieldOps platform. These aren’t just nice-to-haves—they genuinely help farmers be more productive, which supports pricing over time.

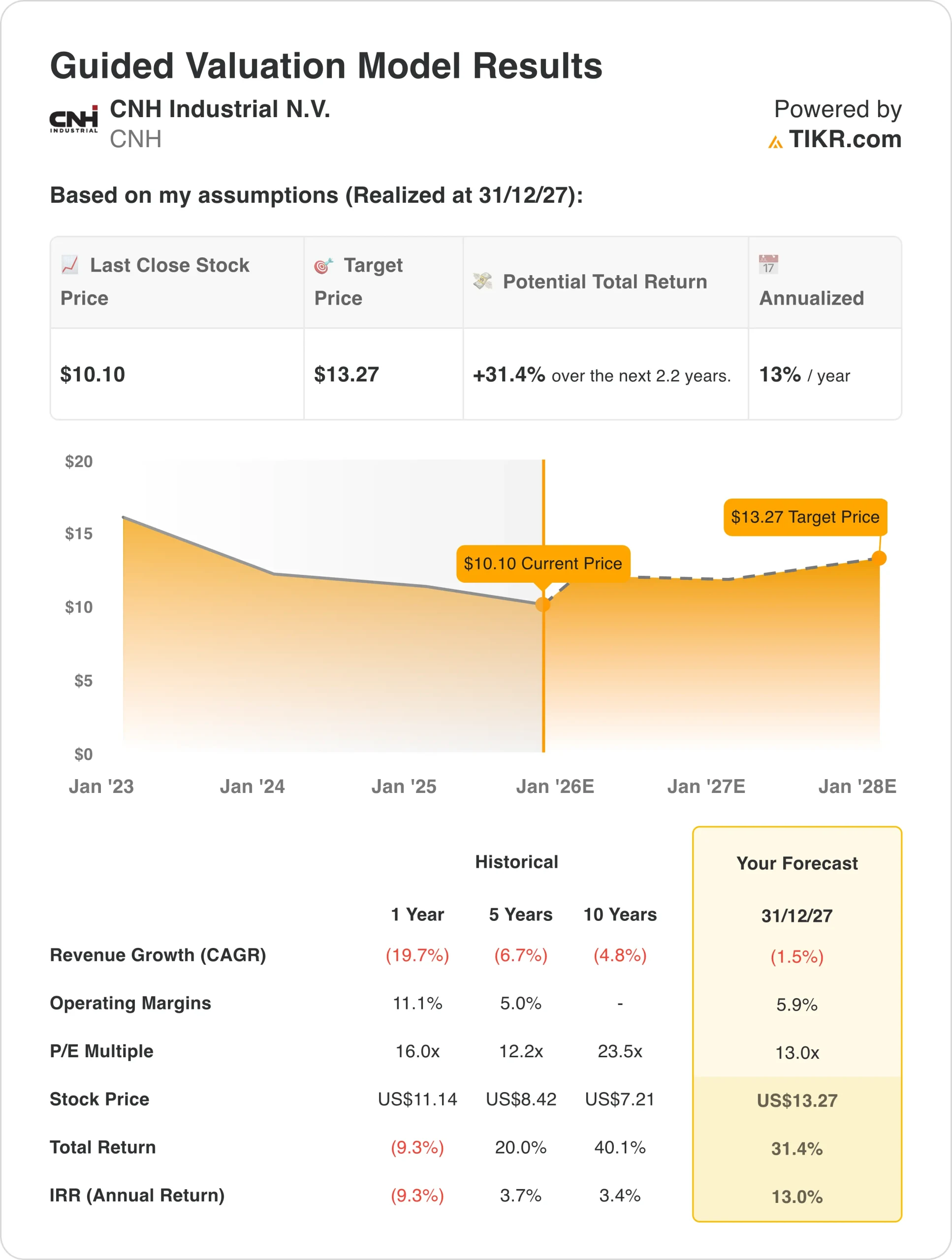

Using conservative assumptions of 1.3% annual revenue growth, 6.3% net margins, and a 13x P/E multiple, we estimate CNH stock could climb from $10 today to $13 per share.

That’s a 31% total return, or about 13% per year over the next 2.2 years.

Value CNH stock with TIKR’s Valuation Model today for FREE (Find undervalued stocks fast) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for CNH stock:

1. Revenue Growth: 1.3%

Revenue dropped 14% in Q2 as CNH deliberately underproduced to help dealers clear out inventory. Agriculture sales fell 17%, and Construction was down 13%.

But there are reasons to be optimistic looking ahead. First, production should match retail demand by late 2025. Once that happens, even a flat market means CNH can increase production and wholesale shipments in 2026.

Second, parts of Europe are showing signs of life, as evidenced by the retail activity pick-up in Germany and Poland during Q2. These markets aren’t booming, but they’re no longer deteriorating.

Third, CNH is advancing its precision agriculture technology. The Starlink partnership provides farmers with reliable internet connectivity anywhere, powering the FieldOps platform.

New features will be unveiled at the Agritechnica show in November 2025. Better technology means more value for farmers, which in turn leads to better pricing for CNH.

Fourth, the company’s strategic sourcing initiatives are reducing the cost base without sacrificing quality. This helps margins even if revenue growth is modest.

We’re using 1.3% annual revenue growth. It assumes 2025 is the bottom and things improve modestly from there.

2. Operating Margins: 6.3%

When you cut production by 12%, your factories become less efficient and ixed costs get spread over fewer units.

The company’s geographic mix is also killing margins. North America is CNH’s highest-margin region, but ag sales there plunged 36% in Q2. That one region accounted for over 90% of CNH’s total ag sales decline. When your top-performing business takes a hit, overall margins suffer.

Tariffs are another headwind, with about $120 million in impact expected in the second half of 2025. Steel and aluminum tariffs doubled from 25% to 50%, pushing up domestic steel prices by 30% since the start of the year. CNH sources 95% of its steel domestically, but even domestic prices rise when tariffs go up.

On the positive side, quality expenses are significantly down year-to-date versus last year. Warranty costs are also falling, while strategic sourcing is delivering purchasing efficiencies.

We’re using 6.3% net margins, which is up from the 4.1% five-year average, but acknowledges all the headwinds CNH is facing.

This assumes the operational improvements are real and deliver results, but that the impacts of tariffs and underproduction don’t disappear overnight.

3. Exit P/E Multiple: 13x

CNH stock trades at about 15x earnings today, lower than the 5-year average of 12.2x and way below the 10-year average of 23.5x.

The market is indicating a lack of confidence in a strong recovery, driven by skepticism about when farmers will resume equipment purchases and whether CNH can improve its margins.

We’re using 13x, which is pretty close to where the stock trades now. That’s a conservative approach, and we’re not counting on the market suddenly falling in love with CNH.

If CNH executes on inventory normalization, quality improvements, and technology rollout, a 13x multiple looks pretty achievable.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Different scenarios for CNH stock through 2030 show varied outcomes based on transformation execution and strategic initiatives: (these are estimates, not guaranteed returns):

- Low Case: The agricultural downturn drags on longer than expected, or CNH loses market share → 5% annual returns

- Mid Case: Inventory normalizes as planned, markets recover modestly in 2026 → 10% annual returns

- High Case: Strong farmer demand rebounds in 2026, margins expand meaningfully → 15% annual returns

CNH stock has defensive characteristics that provide downside protection. The geographic diversification helps, and the financial services business keeps generating profits.

The operational improvements, like quality and sourcing, deliver results regardless of market conditions.

The bull case for CNH stock could be very attractive if everything clicks. If farmers come back to the market in 2026 with pent-up demand, CNH will be well-positioned. Inventories will be clean, production can ramp quickly, and the technology story will be advancing.

See analysts’ growth forecasts and price targets for any stock (It’s free!) >>>

Wall Street Analysts Are Bullish on These 5 Undervalued Compounders With Market-Beating Potential

TIKR just released a new free report on 5 compounders that appear undervalued, have beaten the market in the past, and could continue to outperform on a 1-5 year timeline based on analysts’ estimates.

Inside, you’ll get a breakdown of 5 high-quality businesses with:

- Strong revenue growth and durable competitive advantages

- Attractive valuations based on forward earnings and expected earnings growth

- Long-term upside potential backed by analyst forecasts and TIKR’s valuation models

These are the kinds of stocks that can deliver massive long-term returns, especially if you catch them while they’re still trading at a discount.

Whether you’re a long-term investor or just looking for great businesses trading below fair value, this report will help you zero in on high-upside opportunities.

Click here to sign up for TIKR and get your free copy of TIKR’s 5 AI Compounders report today.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!