Cloudflare, Inc. (NYSE: NET) has been one of the market’s strongest momentum stories. The stock now trades near $216/share, up about 178% over the past year after bottoming around $78. Rapid growth in security, edge computing, and rising demand tied to AI adoption have powered the surge. But with valuation looking expensive and execution risks still high, analysts remain split on what comes next.

Recently, Cloudflare has also pushed into new areas that highlight its ambitions. In September 2025, the company introduced NET Dollar, a U.S. dollar–backed stablecoin designed to enable micropayments across AI-driven web interactions. It also updated its robots.txt “pay-per-crawl” framework, giving website owners the ability to block unauthorized AI scraping or charge bots for access. These moves show Cloudflare is not just defending its role in security and networking, but actively shaping how the internet will evolve in the age of AI.

This article explores where Wall Street analysts think Cloudflare could trade by 2027. We have reviewed consensus targets, growth forecasts, and valuation models to gauge the stock’s possible path. These figures reflect current analyst expectations and are not TIKR’s own predictions.

Unlock our Free Report: 5 AI compounders that analysts believe are undervalued and could deliver years of outperformance with accelerating AI adoption (Sign up for TIKR, it’s free) >>>

Analyst Price Targets Suggest the Stock Is Fairly Valued

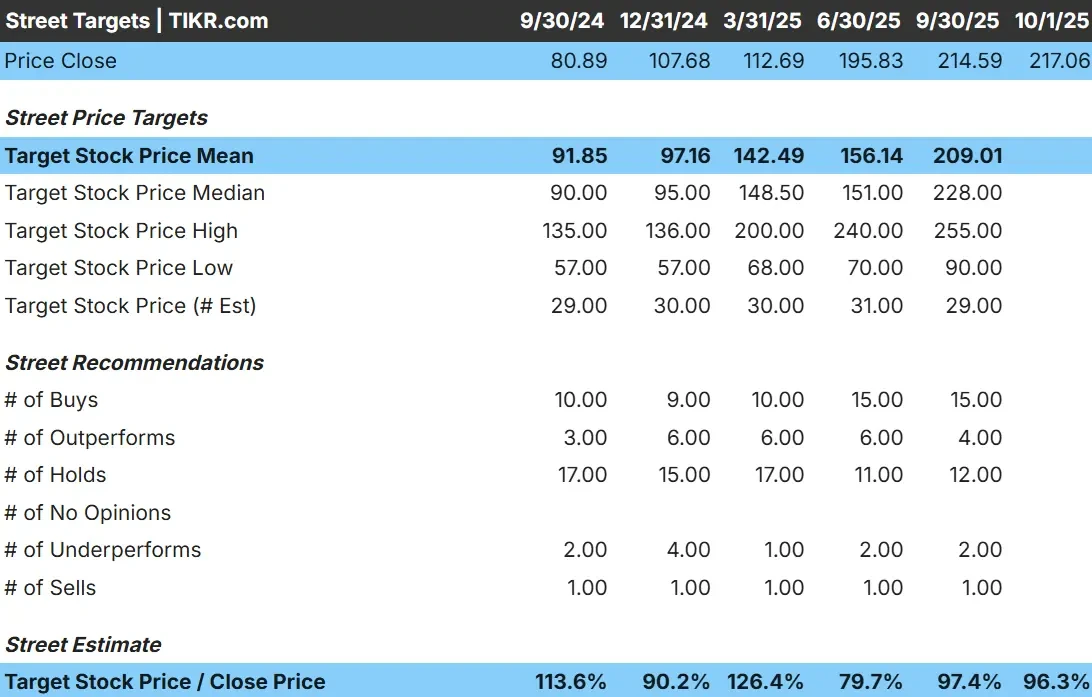

Cloudflare trades at about $217/share today. The average analyst price target is $209/share, which suggests the stock is roughly fairly valued at current levels. Forecasts show a wide spread and reflect divided sentiment:

- High estimate: ~$255/share

- Low estimate: ~$90/share

- Median target: ~$228/share

- Ratings: 15 Buys, 6 Outperforms, 12 Holds, 2 Underperforms, 1 Sell

It looks like analysts see the stock as fully priced for now. While a few still expect further gains, most agree that much of Cloudflare’s strong performance is already reflected in the current share price.

For investors, this means the upside from here is limited unless the company delivers results well above expectations or accelerates profitability faster than expected.

See analysts’ growth forecasts and price targets for Cloudflare (It’s free!) >>>

Cloudflare: Growth Outlook and Valuation

The company’s fundamentals remain strong, but the valuation is demanding:

- Revenue is projected to grow ~27% annually through 2027

- Operating margins may expand from -9.8% today to ~15%

- Shares trade at ~217x forward earnings, well above peers

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 171x forward P/E suggests ~$309/share by 2027

- That implies about 42% upside, or ~17% annualized returns

These numbers suggest Cloudflare can keep compounding quickly if growth and margin expansion materialize. But at this valuation, the stock is already priced for strong execution.

For investors, Cloudflare still offers attractive long-term potential, but its high multiple leaves little margin for error. Any slip in growth or profitability could weigh heavily on the stock.

Value stocks like Cloudflare in as little as 60 seconds with TIKR (It’s free) >>>

What’s Driving the Optimism?

Cloudflare continues to broaden its platform beyond core security services. Its Zero Trust and developer tools are gaining adoption, and the company’s global network makes it well-positioned to capture demand from AI-driven workloads.

Strong gross margins also provide flexibility to eventually expand profitability as scale increases. Supporters believe these strengths give Cloudflare the runway to keep compounding growth for years to come.

For investors, the bull case is about Cloudflare evolving into a full-stack platform with multiple growth levers, not just a niche security company.

Bear Case: Valuation and Execution Risk

Cloudflare’s biggest risk is its valuation. The stock is priced for near-perfect execution, leaving little room for disappointment. If growth slows or profitability improves more gradually than expected, the downside could be meaningful.

Competition also remains a constant pressure, with Zscaler, Akamai, and the hyperscalers all investing heavily in edge and security solutions. Any loss of market share would raise questions about Cloudflare’s ability to maintain momentum.

For investors, the bear case is that Cloudflare has little room for error. At this price, even small disappointments could trigger meaningful pullbacks.

Outlook for 2027: What Could Cloudflare Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 171x forward P/E suggests ~$309/share by 2027. That would represent about a 42% gain from today’s level, or roughly 17% annualized returns.

This outcome assumes sustained high-20s revenue growth and margin expansion to the mid-teens. While that path looks achievable, it already builds in a fair amount of optimism.

For investors, Cloudflare could remain a strong long-term compounder, but outsized returns depend on management delivering growth and margin improvement above what analysts already expect. Without that, gains may be steady but not spectacular.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Click here to sign up for TIKR and get your free copy of TIKR’s 5 AI Compounders report today.