Costco Wholesale Corporation (NASDAQ: COST) has been one of the market’s most consistent long-term winners. The stock now trades near $917/share, supported by resilient earnings and its membership-driven model. Strong renewal rates, loyal customers, and steady growth have kept momentum intact, but with the valuation sitting at a premium, analysts are divided on what comes next.

Recently, Costco has been in the headlines for two big reasons. First, its latest quarterly results showed a strong boost in membership income, highlighting just how powerful its renewal-driven model is. Second, management revealed plans to accelerate expansion with 35 new warehouse openings this fiscal year, up from 27 the year before. For investors, these developments reinforce Costco’s steady growth engine while also reminding the market that its premium valuation rests on execution and continued expansion.

This article explores where Wall Street analysts think Costco could trade by 2028. We have pulled together consensus forecasts and valuation models to get a sense of the stock’s possible trajectory. These figures reflect current analyst expectations and are not TIKR’s own predictions.

Unlock our Free Report: 5 AI compounders that analysts believe are undervalued and could deliver years of outperformance with accelerating AI adoption (Sign up for TIKR, it’s free) >>>

Analyst Price Targets Suggest Limited Upside

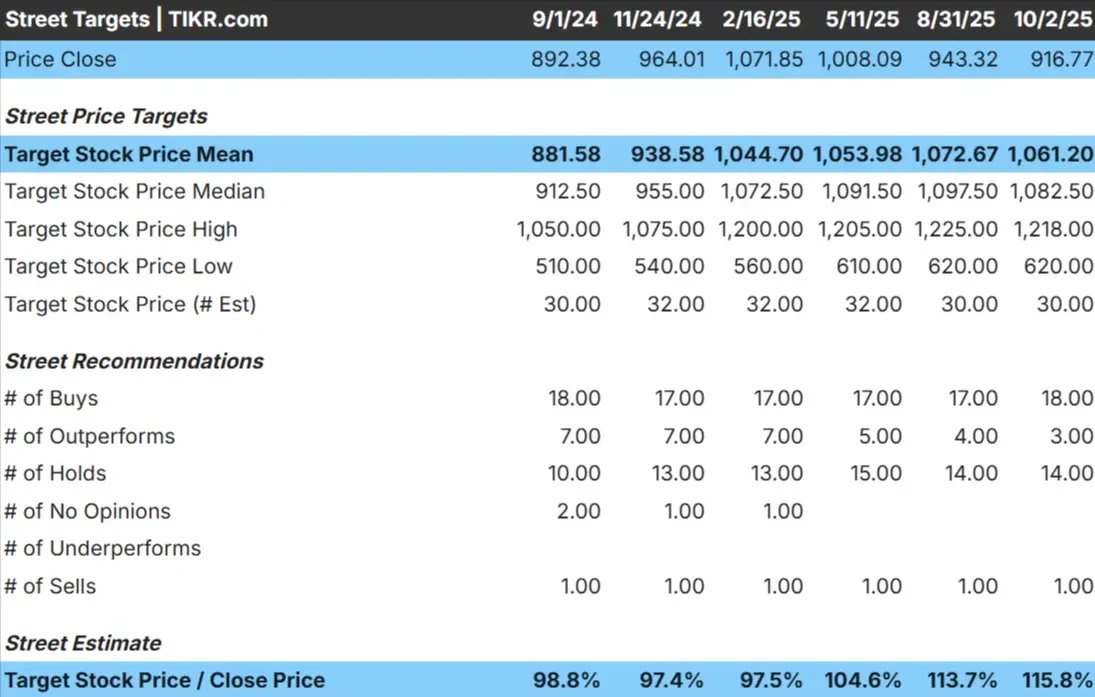

Costco trades at about $917/share today. The average analyst price target is $1,061/share, which points to around 16% upside. Forecasts show a wide spread and reflect divided sentiment:

- High estimate: ~$1,218/share

- Low estimate: ~$620/share

- Median target: ~$1,083/share

- Ratings: majority Buys, with Holds and a few Sells

It looks like analysts see some room for gains, but the wide range of targets suggests conviction is limited. The spread from $620 on the low end to over $1,200 on the high end highlights how uncertain Wall Street is about Costco’s future trajectory.

For investors, this means the potential 16% upside may not be enough to offset the risk of paying such a premium multiple. The stock could drift higher if Costco maintains its consistency, but the downside risk is equally real if sentiment shifts.

See analysts’ growth forecasts and price targets for Costco (It’s free!) >>>

Costco: Growth Outlook and Valuation

The company’s fundamentals look steady, though not exceptional:

- Revenue expected to grow ~7% annually through 2028

- Operating margins forecast near 4%

- Shares trade at ~45x forward earnings, well above retail peers

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 43x forward P/E suggests ~$1,130/share by 2028

- That implies ~23% upside, or about 7.5% annualized returns

These numbers suggest Costco can keep compounding at a healthy pace, but the growth story is more about stability than acceleration. The high multiple reflects investor trust in Costco’s predictability, but it leaves little margin for error if results fall short.

For investors, the takeaway is that Costco remains a dependable long-term holding, though outsized returns likely depend on stronger growth or sustained multiple expansion.

Value stocks like Costco in as little as 60 seconds with TIKR (It’s free) >>>

What’s Driving the Optimism?

Costco’s membership model provides a steady stream of recurring revenue and keeps renewal rates among the highest in retail. Its scale advantage allows it to maintain some of the lowest prices in the industry, which not only drives traffic but also strengthens loyalty over time.

International expansion is another growth lever, with new warehouses continuing to add incremental sales. Costco has also been expanding in digital channels while rewarding shareholders with dividends and occasional special payouts.

For investors, these strengths explain why Costco trades at a premium. The model is simple, resilient, and capable of compounding steadily even in tougher economic environments.

Bear Case: Valuation and Competition

Despite its strengths, Costco’s valuation remains demanding compared to traditional retailers. If revenue growth slows or margins come under pressure, the stock could face a reset toward more typical levels. That risk becomes more pronounced in an environment where consumer spending weakens.

Competition is also fierce. Walmart, Amazon, and discount chains continue to push hard on price and convenience. Any slowdown in membership renewals or shifts in shopping behavior could undermine Costco’s premium position.

For investors, the risk is paying too much for stability. Even modest disappointments could trigger outsized downside if expectations reset.

Outlook for 2028: What Could Costco Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 43x forward P/E suggests Costco could trade near $1,130/share by 2028. That would represent about 23% upside from today’s level, or roughly 7.5% annualized returns.

This outcome reflects expectations for steady mid-single-digit revenue growth and stable margins. While that is a healthy profile, it already assumes consistency. To deliver stronger upside, Costco would need faster international expansion, greater operating leverage, or further multiple expansion.

For investors, the message is that Costco looks like a reliable long-term hold, but not a stock likely to deliver extraordinary returns unless growth accelerates beyond current expectations.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Click here to sign up for TIKR and get your free copy of TIKR’s 5 AI Compounders report today.