The Boston Beer Company, Inc. (NYSE: SAM) has faced a tough stretch as craft beer demand cools and hard seltzer sales fade. Shares trade near $216/share, down about 22% over the past year. Despite these challenges, analysts see room for steady gains as the company leans on strong brands, disciplined cost control, and improved operational efficiency.

Recently, Boston Beer announced new product innovations, including the launch of Surfside Iced Tea, a ready-to-drink cocktail aimed at capturing growth in flavored malt beverages. The company also began scaling its Truly Vodka Soda line and expanding Twisted Tea’s distribution footprint, signaling a continued push to diversify beyond seltzers. These moves suggest Boston Beer is actively adapting its portfolio to shifting consumer tastes.

This article explores where Wall Street analysts think Boston Beer could trade by 2027. We’ve gathered the latest consensus forecasts and valuation models to outline the stock’s potential path based on current expectations, not TIKR’s own predictions.

Unlock our Free Report: 5 AI compounders that analysts believe are undervalued and could deliver years of outperformance with accelerating AI adoption (Sign up for TIKR, it’s free) >>>

Analyst Price Targets Suggest Modest Upside

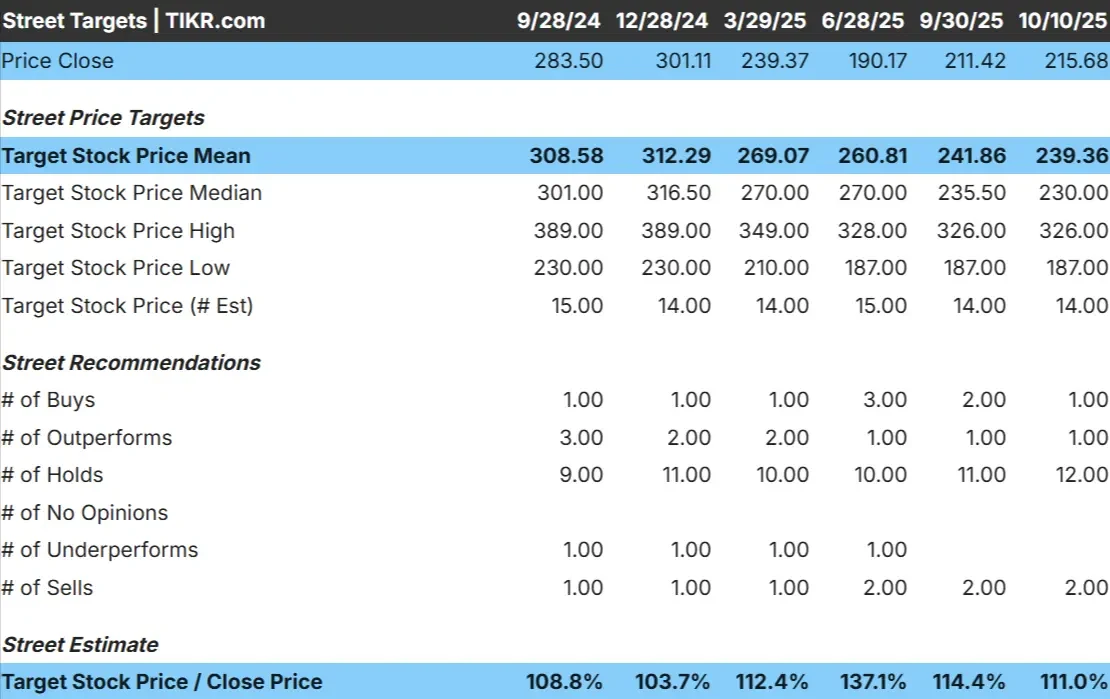

Boston Beer trades around $216/share today. The average analyst price target is about $239/share, implying roughly 11% upside over the next year. Forecasts show a wide range of expectations:

- High estimate: ~$326/share

- Low estimate: ~$187/share

- Median target: ~$230/share

- Ratings: 1 Buy, 1 Outperform, 12 Holds

Analysts see a modest recovery ahead, but overall sentiment remains cautious. For investors, the stock could outperform if consumer trends in premium beverages strengthen or if the company executes well on cost management. Otherwise, returns may stay limited near current levels.

See analysts’ growth forecasts and price targets for Boston Beer (It’s free!) >>>

Boston Beer: Growth Outlook and Valuation

Boston Beer’s fundamentals appear steady, but not particularly strong:

- Revenue is projected to grow about 0.2% annually through 2027

- Operating margins are expected to hold near 7.8%

- Shares trade at roughly 23x forward earnings

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 23x forward P/E suggests around $270/share by 2027

- That implies about 25% total upside, or roughly 11% annualized returns

These assumptions point to gradual improvement in earnings and profitability, not a breakout story. For investors, it suggests the stock could deliver moderate returns as margins stabilize, but stronger volume growth or new product momentum would be needed to unlock meaningful upside.

Value stocks like Boston Beer in as little as 60 seconds with TIKR (It’s free) >>>

What’s Driving the Optimism?

Boston Beer’s brand portfolio remains strong across categories like Samuel Adams, Twisted Tea, and Truly. Twisted Tea continues to post growth and stands out as a key profit driver, helping offset softness in hard seltzers. The company is also expanding into ready-to-drink cocktails through its new Surfside Iced Tea and Truly Vodka Soda lines, aiming to capture shifts in consumer taste toward flavored and low-ABV beverages.

Management has emphasized productivity improvements, pricing discipline, and supply chain efficiency to protect margins even in a slow-demand environment. For investors, these actions suggest Boston Beer has the levers to maintain healthy profitability while gradually rebuilding volume growth.

Bear Case: Weak Volumes and Competitive Pressure

Even with these positives, Boston Beer faces a sluggish demand backdrop. The hard seltzer category remains under pressure, and craft beer volumes continue to decline industry-wide. Competitors with larger portfolios and stronger distribution networks, like Constellation Brands and Molson Coors, could continue gaining share.

At around 23x forward earnings, the valuation already prices in some recovery. If revenue growth stays flat or margins fail to improve further, upside could remain limited. For investors, the key risk is that Boston Beer’s innovation efforts may not offset ongoing category weakness, leaving the stock stuck in a narrow trading range.

Outlook for 2027: What Could Boston Beer Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model suggests Boston Beer could trade near $270/share by 2027. That represents about 25% total upside, or roughly 11% annualized returns from current levels.

This scenario assumes modest revenue growth, stable margins, and consistent cash generation. It reflects a steady recovery path, not an aggressive turnaround. For investors, the takeaway is that Boston Beer looks like a quality operator in a slow market, capable of gradual compounding but unlikely to deliver explosive gains unless category trends improve meaningfully.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Click here to sign up for TIKR and get your free copy of TIKR’s 5 AI Compounders report today.