Burberry Group plc (BRBY) closed fiscal 2024/25 facing one of the most challenging years in its modern history. Revenue fell 15 percent at constant exchange rates to £2.46 billion, weighed down by weaker luxury demand in Asia and Europe. Comparable store sales dropped 12 percent, while adjusted operating profit plunged 88 percent to £26 million. After restructuring and currency headwinds, the company posted an overall operating loss of £3 million.

That slump tells only part of the story. Behind the scenes, management spent much of the year re-engineering Burberry’s cost structure, tightening its product mix, clearing old inventory, and refocusing on brand elevation. The company also expanded its store modernization program, opening 26 new locations while closing under-performing outlets, keeping its global footprint steady at 422 stores.

Despite the headline losses, Burberry finished the year with £708 million in net cash, nearly double the prior year, thanks to disciplined working-capital management and reduced capital expenditure. The brand’s sustainability performance also strengthened, with 84 percent of raw materials now responsibly sourced and Scope 3 emissions down 51 percent since 2019.

The market has taken notice. After sliding to multiyear lows early in 2025, Burberry’s shares have since rebounded by more than 25 percent year to date, suggesting investors may be positioning for a slow but credible turnaround as new designs hit stores and cost savings begin to flow through earnings.

Financial Story: A Reset Year With Glimmers of Recovery

Fiscal 2024/25 was a painful reset for Burberry. Revenue fell 15 percent at constant exchange rates as luxury shoppers pulled back in China and the Americas, while wholesale sales declined 35 percent following a strategic cutback in distribution partners. Comparable store sales were down 12 percent, hurt by fewer tourist shoppers in Europe and persistent macro uncertainty in Asia.

Margins compressed sharply, with adjusted operating profit sinking to £26 million from £418 million a year earlier. Yet despite those declines, Burberry managed to stabilize gross margins in the second half and delivered £24 million in structural cost savings through its efficiency program. Cash flow from operations remained healthy at £526 million, reflecting disciplined expense management.

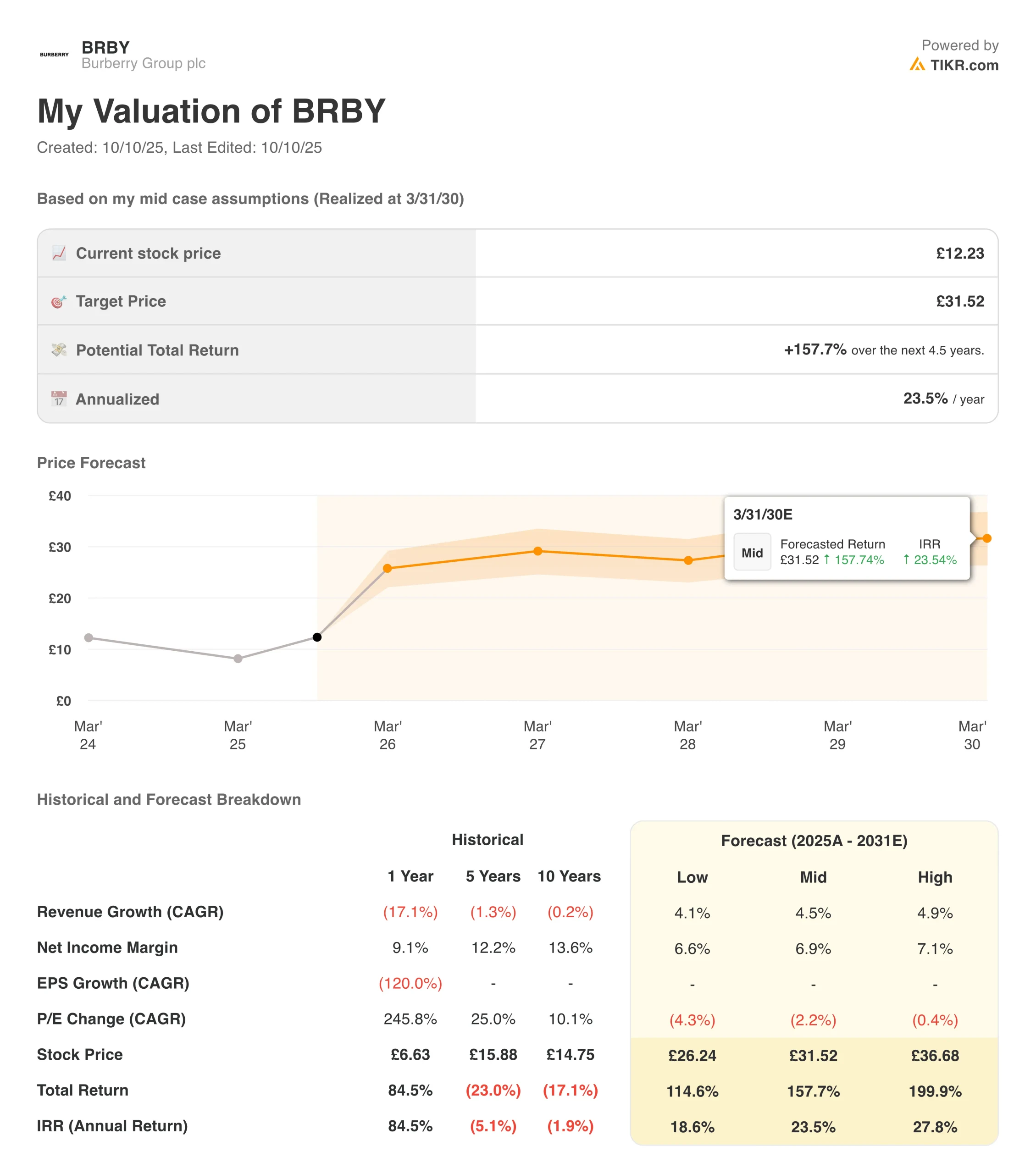

See Burberry’s full financial results & estimates (It’s free) >>>

The numbers underscore a brand in transition, one that took decisive, if costly, steps to simplify its product lineup and regain pricing power. Management acknowledged 2025 as a “year of rebuilding,” but with inventories down 7 percent and store productivity stabilizing, the groundwork for a recovery is being laid.

1. Reigniting Brand Momentum

The company’s turnaround strategy, called “Burberry Forward,” focuses on restoring the British luxury identity that originally defined the label. Creative director Daniel Lee’s first full collections emphasized heritage-driven design with modern tailoring, a pivot back to timeless pieces rather than chasing seasonal trends.

Burberry also doubled down on marketing investment in key fashion capitals such as London, Paris, and Shanghai, where early sell-through rates for its Autumn 2025 collection have reportedly improved. The company plans to refresh 80 percent of its store interiors by 2026 to better align with the new brand aesthetic, and is experimenting with smaller “local luxury” boutiques designed for urban shoppers.

2. Cost Discipline

If the brand narrative is emotional, the operational story is analytical. Burberry achieved £25 million in annual cost savings during FY 2025 and aims for another £75 million through 2027. Net operating expenses fell 3 percent at constant exchange rates, and tight inventory management helped avoid further write-downs.

The company’s decision to exit weaker wholesale relationships may weigh on near-term revenue, but it has already improved cash conversion. With free cash flow steady at £65 million and capex reduced by £57 million year-on-year, management has more flexibility to invest selectively in growth markets without stretching the balance sheet.

Value stocks in less than 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

3. Global Demand: Pockets of Strength, Caution Ahead

Geographically, Asia Pacific remains Burberry’s largest and most volatile region, with sales down 16 percent amid a sluggish China recovery. By contrast, Japan grew 1 percent, aided by inbound tourism, while EMEA fell 8 percent and the Americas declined 9 percent. Encouragingly, leather goods and outerwear outperformed ready-to-wear, hinting at returning core demand.

Looking ahead, management expects a gradual improvement in comparable sales as brand equity rebuilds and tourist traffic normalizes. The wholesale reset will continue through FY 2026, but the focus on retail productivity, pricing integrity, and selective store expansion could restore margins once demand stabilizes.

The TIKR Takeaway

Burberry’s fiscal 2025 results may mark the inflection point in a multi-year turnaround. The numbers are still weak, no one disputes that, but beneath the surface lies progress on cash discipline, inventory management, and brand refocusing. With £708 million in cash and a leaner cost base, the company has the flexibility to ride out the near-term storm.

Execution risk remains high. Global luxury spending is soft, and Burberry’s aspirational positioning puts it between high-end powerhouses like Hermès and mass-premium peers like Ralph Lauren. Still, if Daniel Lee’s creative revival gains traction and operating margins recover even modestly, Burberry could emerge as one of the more interesting comeback stories in European retail by 2026.

Should You Buy, Sell, or Hold Burberry?

Burberry’s financials are weak, but the trajectory is improving. Management has taken painful steps to reset operations, and investors appear willing to give the brand another chance. The stock’s rebound in 2025 reflects that optimism, but sustained recovery will depend on translating creative buzz into consistent sales growth.

For now, Burberry looks like a hold, a potential turnaround play worth watching closely, but still in the early stages of proving that this year’s reset will become next year’s rebound.

Quickly value any stock with TIKR’s powerful new Valuation Model (It’s free!) >>>

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie in the AI application layer, where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Click here to sign up for TIKR and get your free copy of TIKR’s 5 AI Compounders report today.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!