Bendigo and Adelaide Bank (BEN) is one of Australia’s largest regional banks, serving retail, business, agribusiness, and community banking customers nationwide. The group operates through its core Bendigo Bank franchise and its fast-growing digital bank, Up, with a model built around deposits, residential and business lending, and relationship-driven banking, rather than scale alone.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

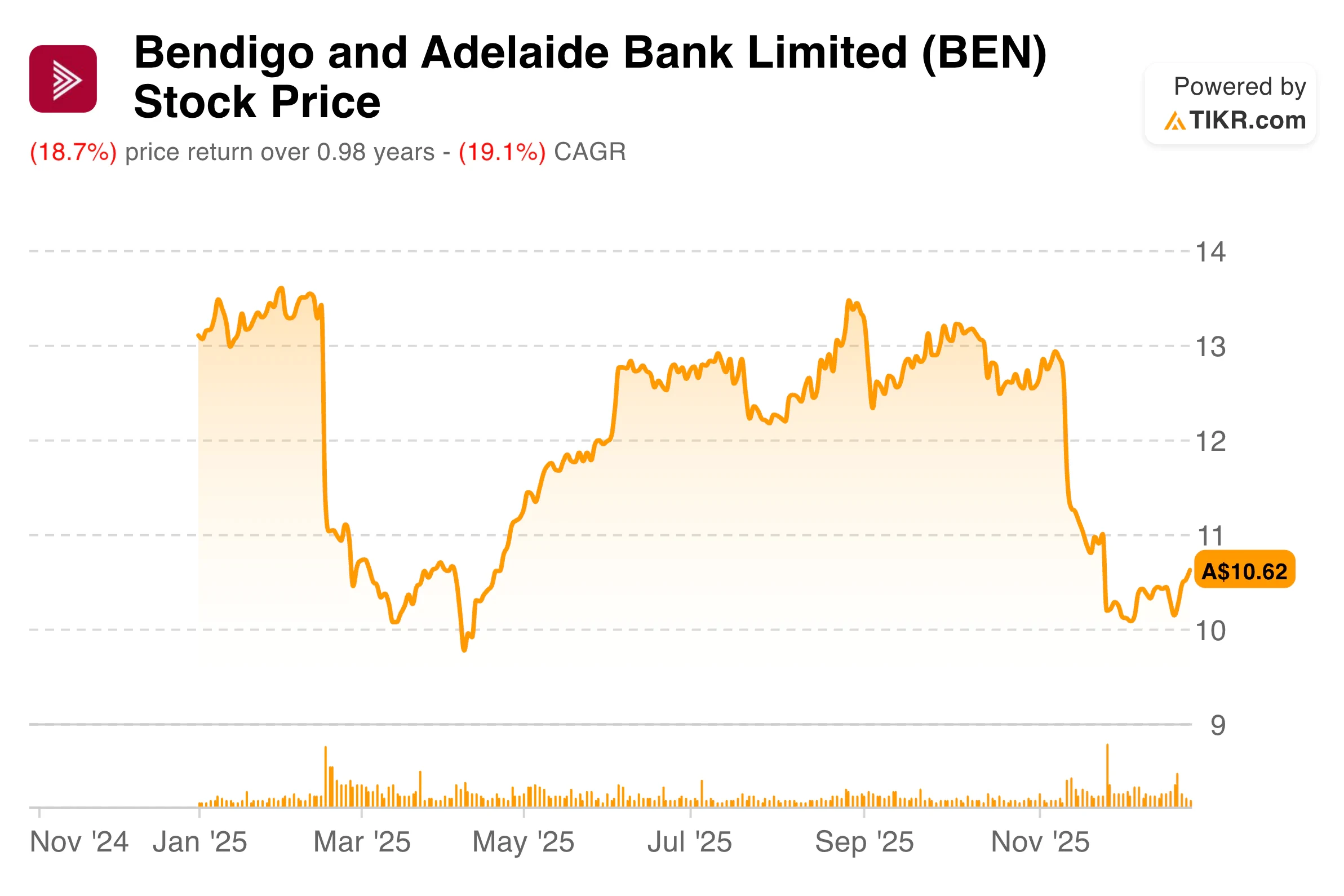

The stock had a difficult year, with shares down sharply as investors focused on softer cash earnings and a statutory loss driven by a large goodwill impairment. That headline result weighed on sentiment, even as underlying operating metrics such as customer growth, deposits, and asset quality remained solid. The market reaction reflected caution around margins, cost inflation, and competition across the Australian banking sector.

Heading into FY26, the setup looks more balanced. Management has completed key simplification work, refreshed its 2030 strategy, and is shifting focus toward lower-cost deposits, productivity gains, and disciplined growth. Valuation expectations now appear more grounded, which puts greater emphasis on execution rather than recovery hype.

Quickly value any stock with TIKR’s powerful new Valuation Model (It’s free!) >>>

Financial Story

Bendigo Bank reported cash earnings of $514.6 million for the full year, down 8.4 percent year over year. Statutory net profit swung to a loss of $97.1 million, driven largely by a goodwill impairment announced late in the year. Excluding that impairment, underlying profitability remained positive, supported by stable margins and controlled credit costs.

The second-half performance showed signs of stabilization, with cash earnings of $249.4 million, 6.0 percent lower than in the first half as income grew 0.2 percent, while expenses rose 2.1 percent. Net interest margin held flat at 1.88 percent, as active pricing management in consumer lending offset competitive pressure in business and agribusiness portfolios.

Balance sheet quality remained a clear strength. Customer deposits grew 6.6 percent for the year, total lending increased 6.3 percent, and gross impaired loans declined to just 0.15 percent of gross loans. The bank also recorded a net write-back of $14.7 million in credit provisions, reinforcing the resilience of its loan book.

Look up Bendigo Bank’s full financial results & estimates (It’s free)>>>

Broader Market Context

Australian banks are operating in a more stable macro environment than a year ago. Inflation has moderated, the labour market remains resilient, and expectations for further RBA rate cuts have improved sentiment around funding costs and credit demand. At the same time, competition for deposits remains intense, which continues to pressure margins across the sector.

For regional banks like Bendigo, scale is less important than funding mix and operating efficiency. The shift toward lower-cost deposits, digital onboarding, and simplified technology platforms matters more in this phase of the cycle. Banks that can grow without stretching margins or balance sheets are better positioned as economic conditions normalize.

1. Customer Growth and Franchise Strength

Customer growth was one of the most encouraging parts of the FY25 results. Total customers increased 11 percent to 2.9 million, the fastest growth rate among major and regional banks. Bendigo Bank’s Net Promoter Score of +28 remained far above the industry average, reinforcing the strength of its relationship-based model.

The digital bank Up continued to stand out, with customers growing 29 percent to 1.2 million, now representing over 40 percent of the group’s customer base. Up’s Net Promoter Score of +55.2 remains one of the strongest in Australian banking, and its momentum is translating into real balance sheet growth.

Up’s mortgage book tripled to $1.7 billion during the year, while deposits rose 34 percent to $2.8 billion. This matters because it shows customer engagement is deepening, not just expanding in number. Over time, this provides a foundation for lower-cost funding and more durable revenue streams.

2. Operational Simplification and Cost Control

FY25 was a year of investment, which pushed headline expenses higher. Total operating expenses rose 7.7 percent, with planned investment spend accounting for 2.3 percent of that increase. Wage inflation, technology costs, and software amortisation also contributed to higher costs.

At the same time, underlying cost discipline improved in the second half. Business-as-usual expenses, excluding investment spend, grew just 0.3 percent in the second half and remained well below inflation. Productivity benefits of $9.4 million were realized during the year, helping offset broader cost pressures.

Management has also simplified the operating model. The bank reduced the number of core banking systems from three to two, completed the migration of Rural Bank customers, and streamlined product offerings. These changes are not flashy, but they support long-term efficiency and execution consistency.

Value stocks like Bendigo Bank in less than 60 seconds with TIKR (It’s free) >>>

3. Strategy Into 2026 and Beyond

The refreshed 2030 strategy centers on five clear pillars: digital simplicity, operational efficiency, deeper customer relationships, trust and societal impact, and reinventing banking for a new generation through Up. A Strategic Execution Office has been established to ensure accountability and progress tracking.

Near-term priorities focus on growing lower-cost deposits, improving productivity, and funding lending growth internally. The household loan-to-deposit ratio declined to 72.8 percent, supporting balance-sheet flexibility. Deposit mix also enhanced, with lower-cost deposits rising 3.3 percent in the second half.

Management is targeting a return on equity above 10 percent by 2030. While that goal is still several years away, the steps taken in FY25 suggest a more disciplined and realistic path forward. The emphasis has shifted from expansion to execution.

The TIKR Takeaway

Bendigo Bank’s FY25 results show a business that looks healthier beneath the surface than headline statutory numbers suggest. Strong customer growth, stable margins, improving funding mix, and disciplined credit performance provide a steadier base heading into 2026. With valuation expectations reset, the investment case now rests on execution rather than recovery optimism.

Should You Buy, Sell, or Hold Bendigo and Adelaide Bank Stock in 2025?

For investors, the key questions revolve around margin durability, cost control, and the pace at which digital growth translates into returns. Progress in lower-cost deposit growth and productivity gains will likely matter more than short-term earnings noise. The stock now reflects a more cautious outlook, placing greater weight on management’s ability to deliver consistent improvements in the next phase of the cycle.

How Much Upside Does Bendigo and Adelaide Bank Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!