The Toronto-Dominion Bank (TD) is one of North America’s largest and most diversified financial institutions, serving over 27 million customers across Canada, the United States, and key international markets. Known for its stability, digital innovation, and retail focus, TD operates through four core segments: Canadian Personal and Commercial Banking, U.S. Retail, Wealth Management & Insurance, and Wholesale Banking.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free)

In 2025, TD entered a new chapter under CEO Raymond Chun, who succeeded Bharat Masrani earlier in the year. The bank’s focus is twofold: strengthening governance and compliance in its U.S. operations, particularly following last year’s BSA/AML settlement, and driving operational efficiency through a sweeping cost-reduction plan.

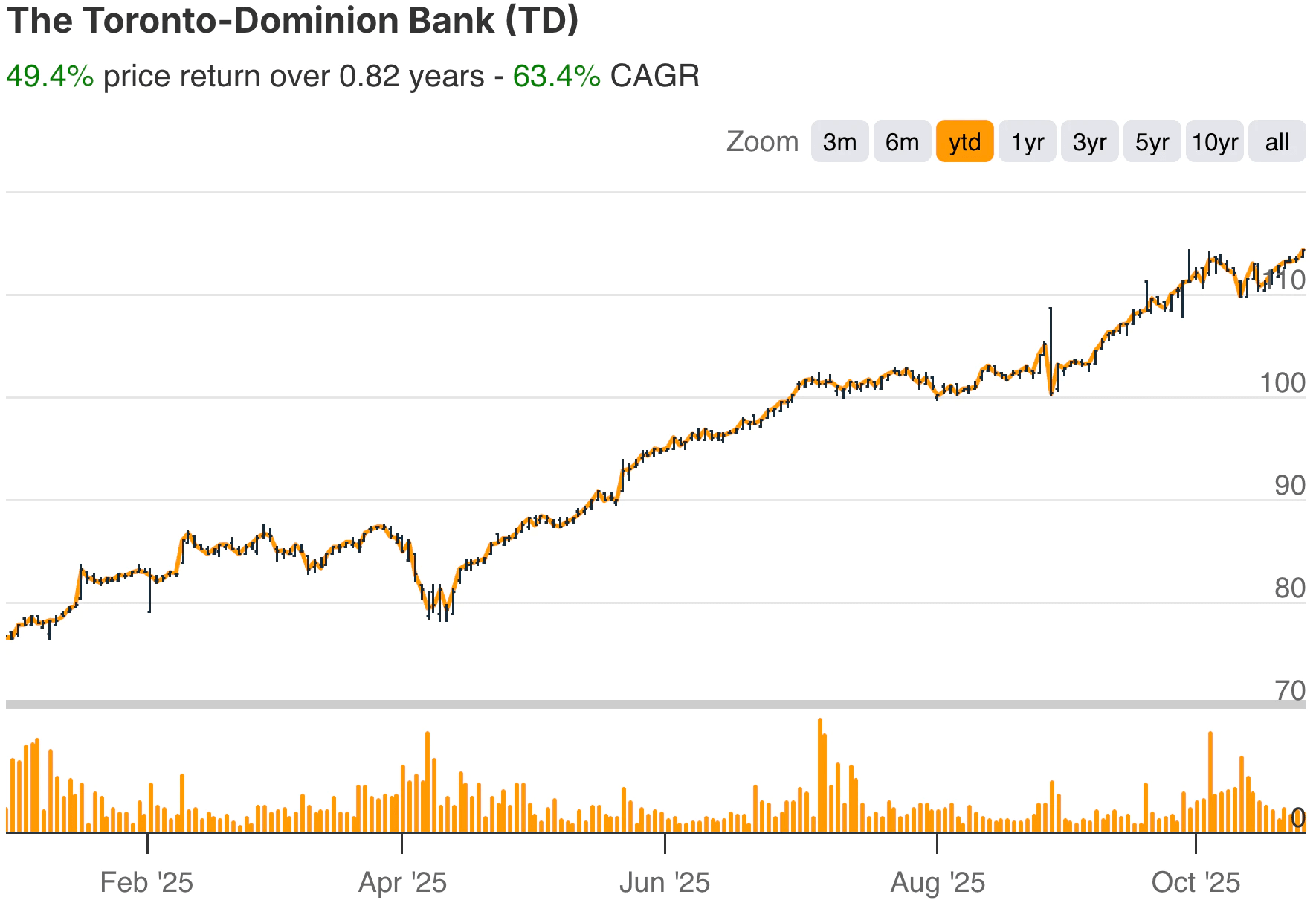

For the third quarter ended July 31, 2025, TD reported adjusted net income of C$3.9 billion, up 6% year-over-year, and adjusted EPS of C$2.20, reflecting the continued strength of its core Canadian franchise and wealth business. The CET1 ratio of 14.8% underscores TD’s strong capital position, even after repurchasing 46 million shares worth over C$4 billion during the quarter.

Quickly value any stock with TIKR’s powerful new Valuation Model (It’s free!) >>>

Financial Story

TD’s third-quarter results marked an important turning point for the bank. After absorbing more than a year of regulatory settlements and integration expenses, profitability and capital generation are returning to trend. Reported earnings surged to C$3.3 billion versus a loss of C$181 million a year ago, while adjusted EPS climbed to C$2.20, up 7% year-over-year.

| Metric | Result | YoY Change | Commentary |

|---|---|---|---|

| Reported Net Income | C$3.34B | +>100% | Compared to a loss last year driven by U.S. settlement costs |

| Adjusted Net Income | C$3.87B | +6% | Record Canadian P&C and Wealth results |

| Adjusted EPS | C$2.20 | +7% | Strong operating leverage |

| CET1 Capital Ratio | 14.8% | Flat | Among the highest in the Big Six |

| PCL Ratio | 41 bps | -370 bps QoQ | Credit conditions remain stable |

| Loan Growth (Canada) | +4% YoY | — | Steady retail and commercial demand |

| Loan Growth (U.S.) | +2% YoY | — | Core lending momentum |

| Free Cash Flow | C$4.0B+ Buybacks | — | Significant capital returns |

| Restructuring Charges | C$333M | — | Targeting annual savings of C$550–650M pre-tax |

Growth was broad-based: record Canadian banking results, double-digit gains in Wealth Management and Insurance, and strong trading income in Wholesale Banking. The U.S. Retail division, while still absorbing AML remediation costs and restructuring charges, is beginning to show balance sheet improvement, with net interest margins up 15 basis points quarter-over-quarter to 3.19%, and core loan growth of 2% year-over-year.

The Canadian Personal and Commercial segment delivered record net income of C$1.95 billion, powered by higher loan and deposit volumes and continued strength in TD Auto Finance. Digital adoption continues to accelerate, with record year-to-date sales across chequing, savings, and credit card products, underscoring the scalability of TD’s omnichannel strategy.

Look up Toronto-Dominion’s full financial results & estimates (It’s free) >>>

Broader Market Context

After a challenging two years for the banking sector, TD’s results suggest the bank is positioning itself for a new growth cycle. Canadian banks faced margin compression, regulatory costs, and subdued loan growth in 2024, but with interest rates stabilizing and capital ratios improving, TD stands out for its combination of earnings resilience and capital flexibility.

In the U.S., where TD operates as “America’s Most Convenient Bank”, management is focused on repositioning its balance sheet and completing governance remediation. Executives have guided toward a near-term expense headwind through 2026, but expect meaningful improvement thereafter.

Longer term, TD’s North American diversification, spanning retail, wealth, insurance, and capital markets, remains a structural advantage, especially as the bank leverages AI-driven automation and digital channels to unlock operating leverage.

1. Record Canadian Banking and Wealth Momentum

TD’s domestic franchise continues to outperform peers. Canadian Personal and Commercial Banking achieved record revenue of C$5.24 billion and record earnings of C$1.95 billion, supported by stable net interest margins (2.83%) and strong loan growth. Commercial and small business lending remained healthy, while digital client engagement surged across product lines.

Wealth and Insurance were standout performers, with net income up 63% year-over-year to C$703 million, marking the sixth consecutive quarter of double-digit revenue growth. TD Asset Management added C$2.5 billion in new mandates, while TD Insurance achieved record premium volumes and maintained its #1 ranking for brand awareness in home and auto coverage.

2. U.S. Restructuring and Compliance Remediation

TD’s U.S. operations are entering a recovery phase. Adjusted net income of C$956 million reflected continued loan and deposit growth but higher governance costs related to AML remediation. Management reaffirmed that the U.S. balance sheet restructuring is now largely complete, with a 10% reduction in total assets and the bond repositioning program fully executed.

The U.S. Retail segment’s profitability is expected to improve as restructuring costs taper off and core lending growth reaccelerates in late 2026. TD Bank N.A. also earned another “Outstanding” Community Reinvestment Act rating, marking over a decade of top-tier performance in U.S. regulatory compliance and community engagement.

Value stocks like Toronto-Dominion Bank in under 60 seconds with TIKR (It’s free) >>>

3. Cost Discipline and Strategic Efficiency Plan

Under Raymond Chun’s leadership, TD has unveiled a C$2.0–2.5 billion annual cost-savings plan, including C$500 million in savings from AI and process automation. Combined with workforce optimization and technology investments, the initiative aims to lift adjusted return on equity to 16% and adjusted EPS growth to 7–10% annually by fiscal 2029.

In parallel, TD continues to return capital to shareholders. With a CET1 ratio near 15% and roughly C$15 billion of excess capital expected to be returned by 2026, the bank remains one of the most overcapitalized among the Big Six. A renewed share buyback program (valued at C$6–7 billion) and steady dividend growth reinforce TD’s long-term investor appeal.

The TIKR Takeaway

TD’s story is one of transition and renewal. After years of expansion and amid U.S. regulatory setbacks, the bank is executing a disciplined turnaround that balances near-term cost management with long-term digital growth. Canadian core earnings are firing on all cylinders, the balance sheet remains pristine, and capital deployment is generous.

While the U.S. restructuring will continue to weigh on expenses through 2026, the payoff, simplified operations, higher margins, and better risk management set up a cleaner, more efficient TD Bank entering the second half of the decade.

Should You Buy, Sell, or Hold Toronto-Dominion Bank Stock in 2025?

With a strong capital position, improving efficiency, and a clear return-to-growth strategy, TD remains one of the most compelling large-cap bank plays in North America. The bank’s combination of dividend strength, scale, and digital innovation gives investors exposure to both stability and upside. If management executes on cost savings and U.S. remediation winds down as planned, TD could enter 2026 as one of the sector’s best risk-adjusted growth stories.

How Much Upside Does Toronto-Dominion Bank Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!