Canadian Pacific Kansas City Limited (CP), the first single-line railroad connecting Canada, the U.S., and Mexico, has quickly evolved from a merger integration story to a growth execution story. Formed by the 2023 combination of Canadian Pacific Railway and Kansas City Southern, the company now operates over 20,000 miles of track across North America’s most strategically important freight corridor, serving agriculture, energy, automotive, and intermodal markets.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

In 2025, that network is running on all cylinders. For the first half of the year, CPKC posted revenue of C$9.8 billion, up 6% year-over-year, with adjusted operating income rising 14% and EPS climbing 17% to C$1.38. The second quarter alone saw record results in grain shipments, Mexico intermodal volumes, and cross-border automotive. Operating ratio improved 180 basis points to 58.9%, reflecting stronger train productivity, pricing gains, and early cost synergies from the Kansas City Southern integration.

CEO Keith Creel called Q2 “our strongest quarter since the merger,” highlighting operational efficiency, synergy capture, and record safety performance. With C$1.2 billion in merger synergies expected by 2027 and capital spending targeted at ~C$3.2 billion for 2025, CPKC is well positioned to deliver on its promise of sustainable, cross-border growth that few competitors can match.

Quickly value any stock with TIKR’s powerful new Valuation Model (It’s free!) >>>

Financial Story

CPKC’s second quarter marked a turning point from integration to growth acceleration. Revenues rose 6% to C$5.02 billion, driven by robust intermodal and grain performance, while core pricing strength and disciplined cost control expanded operating income faster than volume growth. The railroad’s adjusted EPS of C$0.73 topped consensus expectations, marking its fifth straight earnings beat since the merger.

| Metric | Result | YoY Change | Commentary |

|---|---|---|---|

| Revenue | C$5.02 B | +6% | Record cross-border and intermodal growth |

| Adjusted Operating Income | C$2.06 B | +14% | Margin expansion on efficiency and pricing |

| Operating Ratio | 58.9% | –180 bps | Continued synergy capture |

| Adjusted EPS | C$0.73 | +17% | Strong pricing and cost leverage |

| Free Cash Flow | C$1.05 B | +12% | Higher earnings, stable capex |

| Grain Revenue | C$1.07 B | +11% | Canadian and U.S. crop recovery |

| Intermodal Revenue | C$1.02 B | +13% | Mexico–U.S. corridor drives record volumes |

| Automotive Revenue | C$392 M | +8% | EV plant shipments from Mexico rising |

| Synergies Captured YTD | C$220 M | — | On track for C$400M full-year target |

The integration of Kansas City Southern continues to outperform initial assumptions. Synergy realization reached C$220 million by midyear, tracking ahead of schedule toward C$400 million for 2025, and management reaffirmed its C$1.2 billion annual synergy target by 2027. The company’s capital program remains focused on high-return expansion projects, including the Mexico–U.S. automotive and intermodal corridor, where new terminals in San Luis Potosí and Laredo are driving record carload volumes.

See Canadian Pacific Kansas City’s full financial results & estimates (It’s free) >>>

Broader Market Context

Freight rail in North America is regaining investor attention after two years of soft volumes and high inflation. With supply chains normalizing and Mexico emerging as a manufacturing hub under nearshoring trends, CPKC’s unique tri-national footprint gives it an unmatched competitive edge. It’s the only railroad that can move freight directly from Canada to Mexico without an interchange, cutting transit times by up to 48 hours compared to competitors.

That structural advantage is translating into durable pricing power. Automotive, intermodal, and grain flows all benefit from macro tailwinds: Mexico’s manufacturing surge, North American energy exports, and agricultural recovery after 2024’s drought cycle. As trade corridors realign under the USMCA framework, CPKC’s network sits at the intersection of the continent’s most important growth lanes, making it a strategic asset in a reshaped global logistics landscape.

1. Synergy Capture and Margin Expansion

CPKC’s post-merger integration is ahead of schedule, and by Q2 2025, the company had achieved over C$220 million in annualized synergies, primarily from workforce optimization, shared maintenance facilities, and procurement savings. The operating ratio’s 180-basis-point improvement to 58.9% reflects both efficiency gains and disciplined network integration.

Management continues to target C$1.2 billion in annual synergies by 2027, split roughly 60% from cost reduction and 40% from new revenue opportunities. The full benefits of cross-border train rationalization and train-length optimization are still unfolding, suggesting further margin expansion potential in 2026–27 as capital projects mature.

2. Cross-Border Growth and Nearshoring Tailwinds

CPKC’s biggest differentiator is its north–south network, which links Canada’s resource centers, the U.S. Midwest, and Mexico’s fast-growing industrial belt. Cross-border traffic between Mexico and the U.S. surged 27% year-over-year, powered by record intermodal and auto shipments. The Laredo Gateway remains the network’s growth epicenter, with new partnerships secured with Schneider National and Knight-Swift to expand temperature-controlled and automotive freight.

Nearshoring remains the macro story behind CPKC’s growth. As U.S. and Canadian manufacturers diversify supply chains away from Asia, Mexico’s factory output is expected to grow 5–6% annually through 2030, directly benefiting CPKC’s corridor. The company’s seamless border transit and customs integration are proving to be major selling points for large OEMs and logistics customers alike.

Track company financials, stock value, and competitor information with TIKR (It’s free) >>>

3. Balance Sheet Strength and Shareholder Discipline

Financial flexibility remains a hallmark of CPKC’s strategy. The company ended Q2 with C$23 billion in total debt and a net leverage ratio of 2.7x EBITDA, comfortably within investment-grade parameters. Strong cash generation supports a C$3.2 billion capex plan for 2025, focused on track upgrades, locomotives, and terminal automation.

Free cash flow rose 12% year-over-year to C$1.05 billion, reflecting higher earnings and consistent capital discipline. The quarterly dividend of C$0.19 per share remains well covered, and management reiterated its commitment to “balanced capital allocation,” prioritizing investment and debt paydown over buybacks until synergy goals are fully realized.

The TIKR Takeaway

CPKC has validated the merger thesis faster than skeptics expected. Efficiency gains, nearshoring-driven demand, and operational excellence have turned this into one of North America’s premier infrastructure stories. The network’s tri-national reach creates a long-term growth platform that’s both cyclical and structural, combining traditional rail economics with modern trade flows.

That said, the bar for execution remains high as investors will look for sustained double-digit EPS growth, consistent margin improvement, and clear delivery on synergy targets to justify current valuations. Still, the risk-reward tilts positive: CPKC’s unique cross-border franchise and operational discipline give it more levers for value creation than any Class I peer.

Should You Buy, Sell, or Hold Canadian Pacific Kansas City Stock in 2025?

CPKC’s cross-border network, improving margins, and synergy execution make it one of the most attractive long-term holdings in North American transport. While the stock’s 2025 rally has been steady rather than explosive, the structural story is undeniable: this is a company built to capitalize on the continent’s next era of trade growth. For investors seeking a mix of industrial resilience, infrastructure exposure, and durable compounding, CPKC remains on the right track.

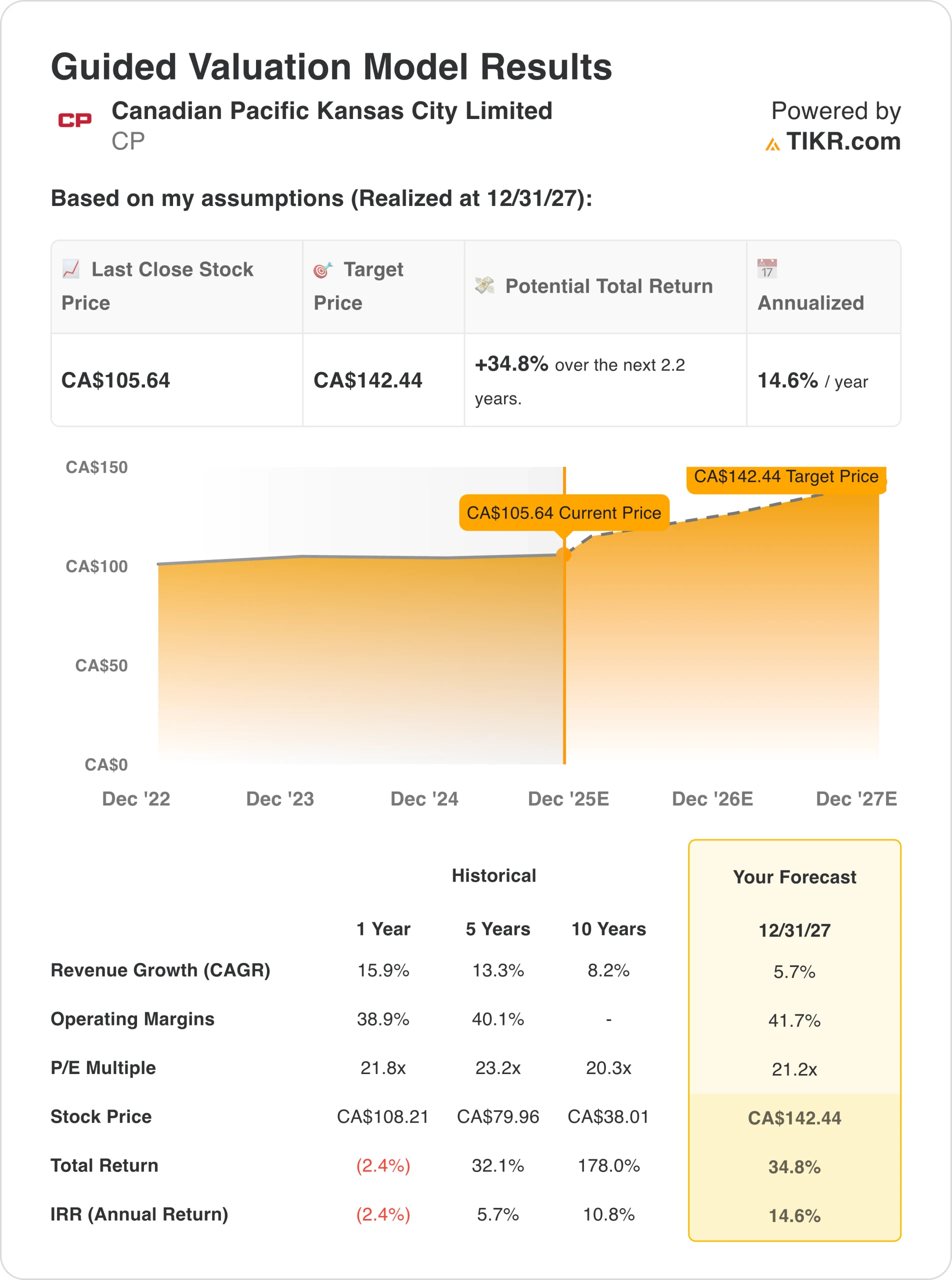

How Much Upside Does Canadian Pacific Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

Find out what your favorite stocks are really worth (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!