Key Takeaways:

- Royal Caribbean delivered exceptional first-quarter results with adjusted earnings per share of $2.71, exceeding guidance by $0.23 and representing strong operational execution.

- RCL achieved record Wave season bookings, with a net yield growth of 5.6%, and maintained robust booking momentum through April 2025.

- Management raised its full-year adjusted earnings per share guidance for 2025, estimating approximately 28% year-over-year growth.

- Get accurate financial data on over 100,000 global stocks for free on TIKR >>>

Valued at a market capitalization of approximately $72 billion, Royal Caribbean Group (RCL) operates as the world’s second-largest cruise line company with a global fleet of 67 ships across five premium brands.

It serves millions of guests annually through its portfolio, including Royal Caribbean International, Celebrity Cruises, and Silversea, while expanding its land-based vacation experiences through Perfect Day destinations and the Royal Beach Club collection.

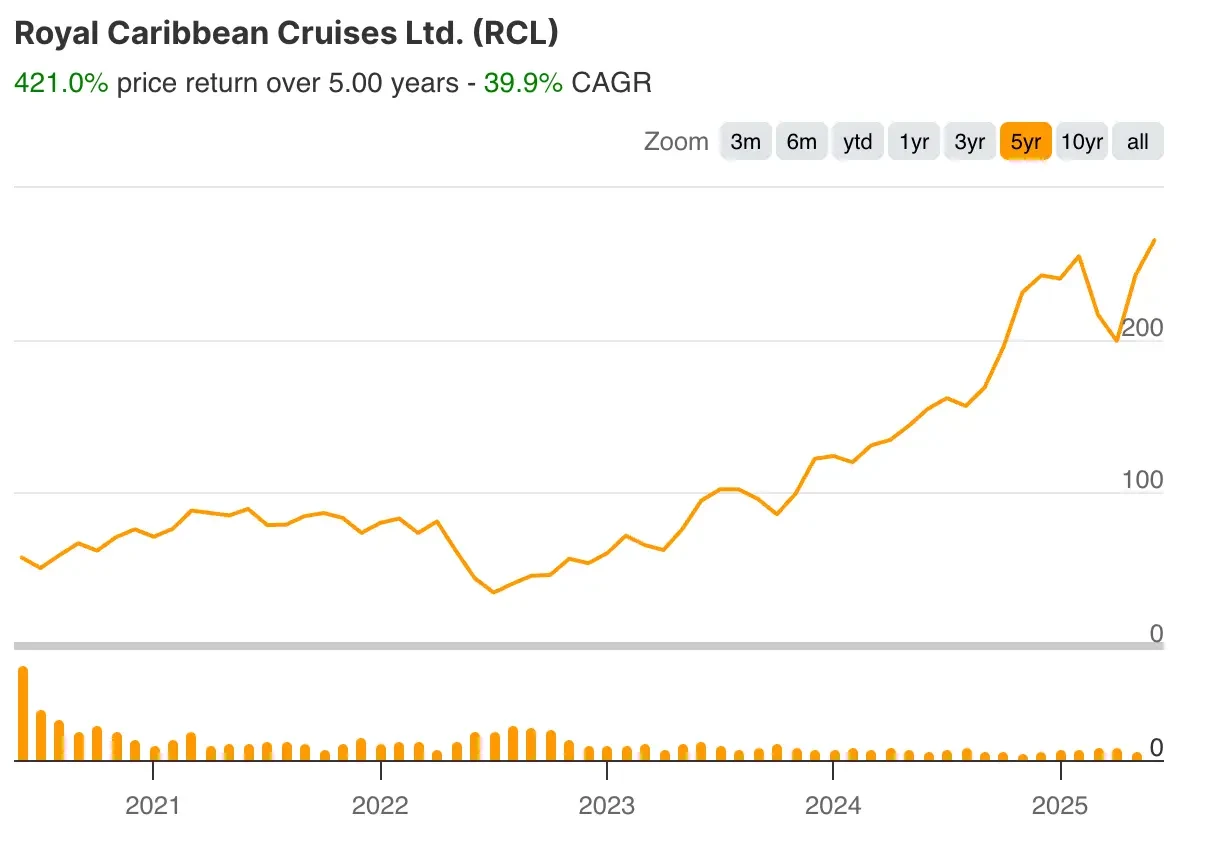

RCL stock has demonstrated remarkable resilience and growth momentum following an outstanding first-quarter earnings report that exceeded Wall Street expectations.

The strong performance reflects RCL’s successful execution of its growth strategy, innovative ship deployments, and effective revenue management capabilities.

Royal Caribbean’s ability to deliver exceptional guest experiences while maintaining pricing discipline has positioned it advantageously within the broader vacation market, driving sustained demand even amid macroeconomic uncertainties.

The RCL stock price in 2025 has reflected investor confidence in the company’s ability to navigate challenging market conditions while maintaining its superior financial performance.

Let’s explore why you should consider adding RCL stock to your equity portfolio right now.

1. RCL Stock Benefits from Exceptional Q1 Execution

RCL stock gained momentum following its stellar first-quarter performance that surpassed expectations across all key metrics.

Adjusted earnings per share reached $2.71, exceeding its midpoint guidance by $0.23 and demonstrating the company’s operational excellence. It also beat consensus estimates by 7% in the March quarter.

Net yield growth of 5.6% in constant currency exceeded initial guidance by 60 basis points, driven by strong close-in demand and effective pricing strategies across all itineraries.

Royal Caribbean delivered over two million unforgettable vacations during the quarter while achieving exceptional guest satisfaction scores.

Operating cash flow in Q1 reached $1.6 billion, representing a substantial increase from $1.3 billion in the prior year period. The adjusted EBITDA margin expanded to 35%, representing a 360-basis-point year-over-year improvement, which highlights the company’s enhanced profitability profile.

Wave season bookings established quarterly records, positioning Royal Caribbean with strong bookloads for the remainder of 2025 and extending into 2026.

The combination of new ship introductions, enhanced guest experiences, and strategic revenue management contributed to the exceptional quarterly performance that exceeded management’s expectations.

Check out RCL’s full analyst estimates and growth forecast (It’s free) >>>

2. The Cruise Stock Is Positioned for Sustained Growth

The RCL stock price reflects investor confidence in the company’s strategic growth initiatives and innovative fleet expansion.

Royal Caribbean continues introducing game-changing ships that command premium pricing, including the successful launch of Star of the Seas and Celebrity Xcel, which have exceeded expectations for both pricing and load factors.

These industry-leading new ships create competitive advantages that drive sustained yield premiums and enhanced guest satisfaction.

Royal Caribbean’s expanding portfolio of exclusive private destinations represents a significant growth driver. Over the next several years, the company plans to increase the number of exclusive destinations from 2 to 7.

The upcoming Royal Beach Club in Nassau, set to open in December, showcases a continued investment in high-margin destination experiences that enhance guest satisfaction while generating substantial returns.

Royal Caribbean’s unified loyalty program demonstrates exceptional effectiveness, with loyalty members accounting for nearly 40% of total bookings and spending 25% more per trip than non-members.

Cross-brand bookings continue to increase, while digital engagement through the mobile app has doubled year-to-date, demonstrating the strength of Royal Caribbean’s commercial flywheel and customer retention strategies.

Find the best stocks to buy today with TIKR. (It’s free) >>>

3. Royal Caribbean Has a Strong Balance Sheet

RCL stock benefits from a strong balance sheet and disciplined capital allocation approach. During the quarter, S&P Global Ratings upgraded Royal Caribbean’s credit rating to investment grade, reflecting a robust financial position, consistent performance, and prudent capital allocation strategy.

Royal Caribbean ended Q1 with $4.5 billion in total liquidity and minimal near-term debt maturities, providing it with financial flexibility.

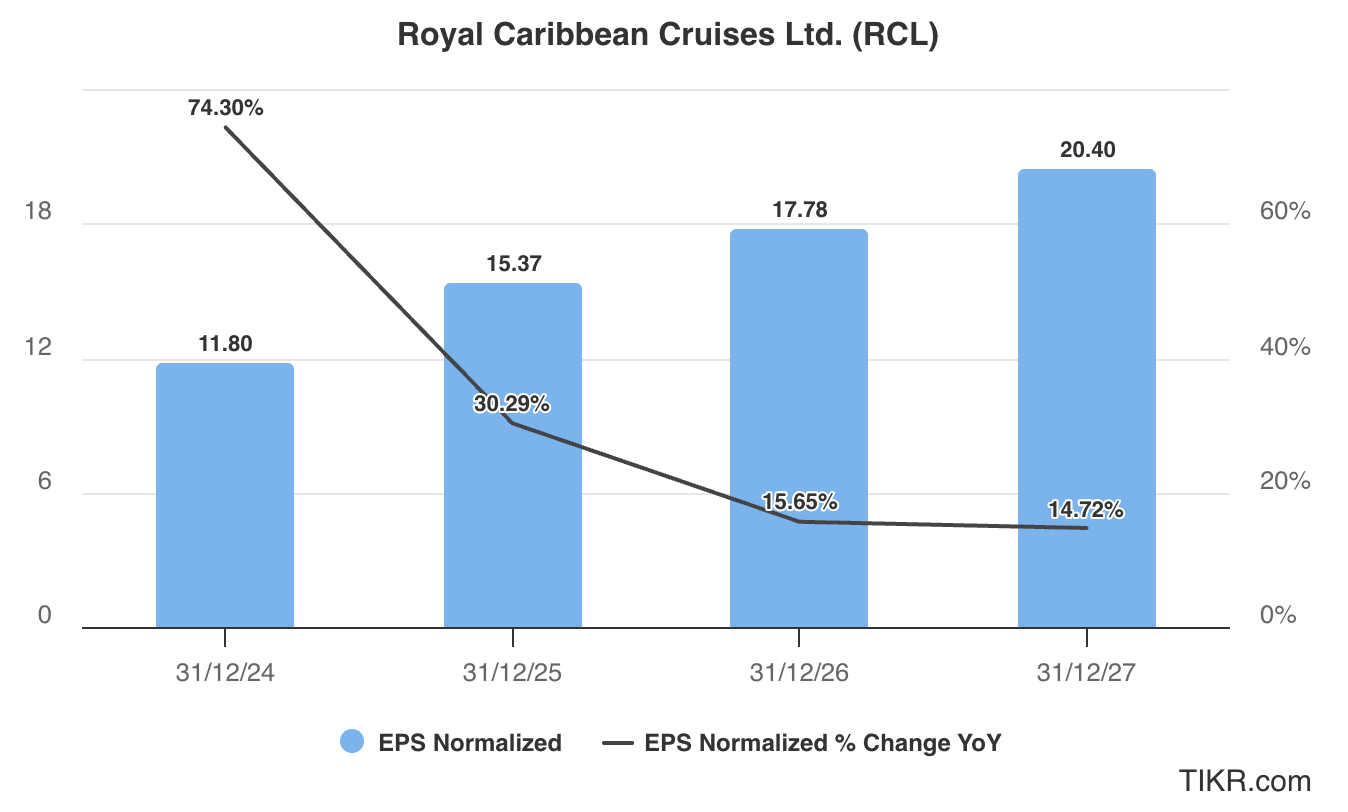

Management raised full-year adjusted earnings per share guidance to $14.55-$15.55, indicating a 28% year-over-year growth driven by favorable foreign exchange rates and improved fuel costs.

It also expects 15% growth in adjusted EBITDA and a 210-basis-point expansion in gross EBITDA margin, positioning Royal Caribbean for accelerated cash flow generation.

Royal Caribbean’s 5.5% capacity growth in 2025 reflects a disciplined expansion strategy that involves introducing high-quality ships, which command premium pricing.

Its formula of moderate capacity growth, moderate yield growth, and strong cost control continues driving superior financial performance while maintaining the flexibility to invest in strategic growth initiatives.

Valuation Setup for RCL Stock

Analysts tracking RCL stock expect its sales to rise from $16.5 billion in 2024 to $21.4 billion in 2027. Comparatively, adjusted earnings are forecast to increase from $11.80 per share to $20.40 per share in this period.

RCL stock currently trades at a forward price-to-earnings multiple of 17x, which is above its 12-month average multiple of 15x.

If the cruise stock is priced at a multiple of 16x and reaches its projected $20.4 in normalized EPS, it will trade around $326/share in June 2027, indicating an upside potential of 24% from current levels.

Value stocks quicker with TIKR (It’s free, no card required) >>>

Average Analyst Price Target for RCL Stock

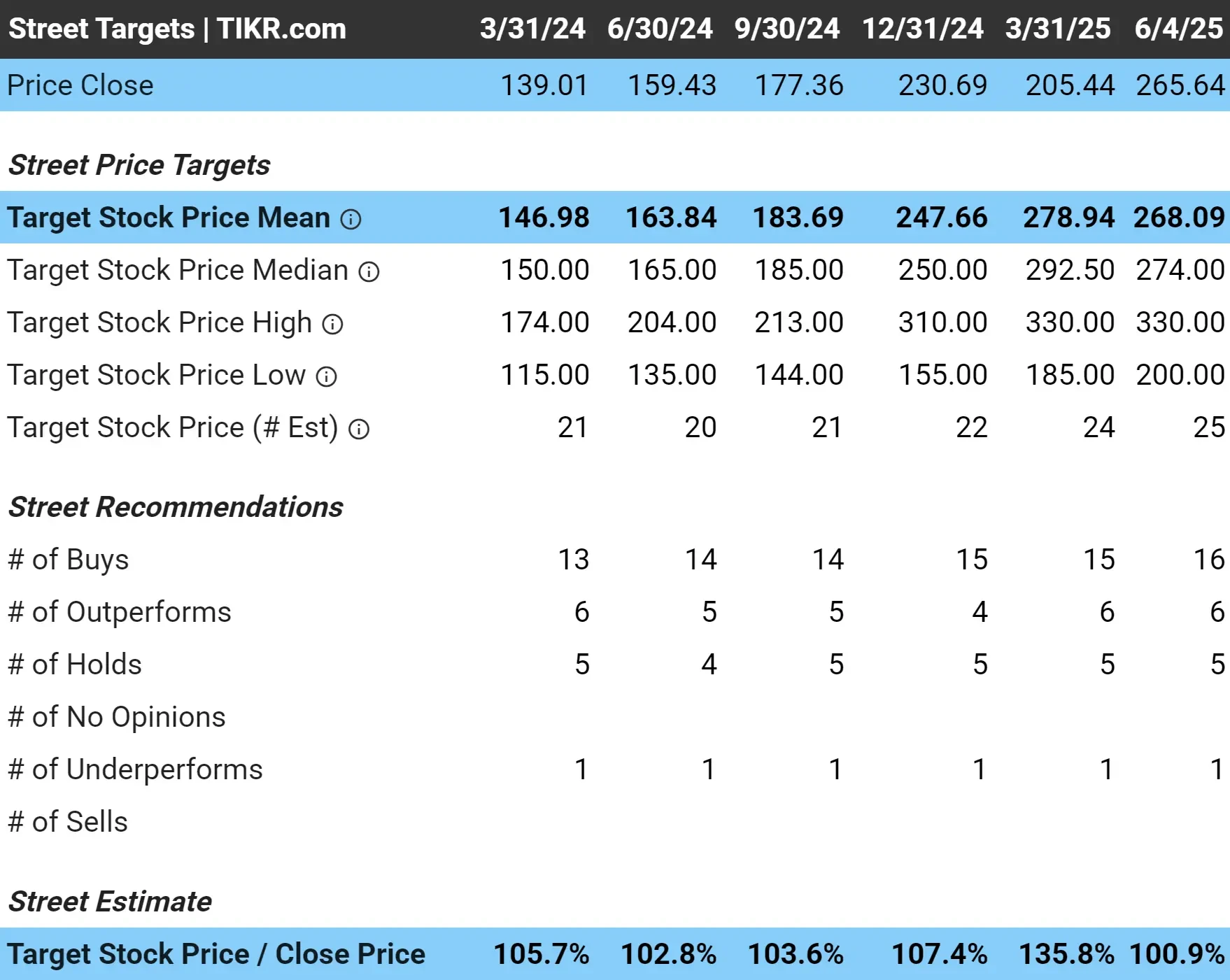

While Wall Street remains bullish on RCL stock, with a consensus price target of $268/share, analysts expect the stock to rise around 1% from current levels.

This really isn’t a lot of upside. However, it’s likely that Royal Caribbean is one of the best operators in the cruise industry.

Notably, RCL stock currently has a high target price of $330 and a low target price of $200.

Of the 28 analysts tracking Royal Caribbean stock, 22 recommend “Buys”, five recommend “Hold,” and one recommends “Sell.”

TIKR Takeaway for Royal Caribbean Stock

RCL stock could be a premium cruise company as Royal Caribbean executes a proven growth strategy from a position of financial strength.

The company’s leadership in cruise innovation, exclusive destination development, and customer experience differentiation creates sustainable competitive advantages that drive market share gains and pricing power.

Royal Caribbean’s investment-grade balance sheet, strong cash flow generation, and disciplined capital allocation provide downside protection. At the same time, its innovative capabilities and expanding market opportunity create substantial upside potential for long-term investors.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!