Upstart Holdings, Inc. (NASDAQ: UPST) has been volatile as lending demand weakened and profitability slipped. The stock trades near $47/share, down about 11% over the past year, as investors weigh the risks of its AI-driven lending model against its long-term potential.

Recently, Upstart reported quarterly results that showed signs of stabilization, with loan transaction volumes improving and new bank partners joining its platform. The company also launched an upgraded version of its AI underwriting model to improve borrower risk accuracy. These moves suggest Upstart is positioning itself for recovery as credit markets normalize.

This article explores where Wall Street analysts think Upstart could trade by 2027. We have compiled consensus targets and valuation models to outline the stock’s potential path. These figures reflect current analyst expectations and are not TIKR’s own predictions.

Unlock our Free Report: 5 AI compounders that analysts believe are undervalued and could deliver years of outperformance with accelerating AI adoption (Sign up for TIKR, it’s free) >>>

Analyst Price Targets Suggest Meaningful Upside

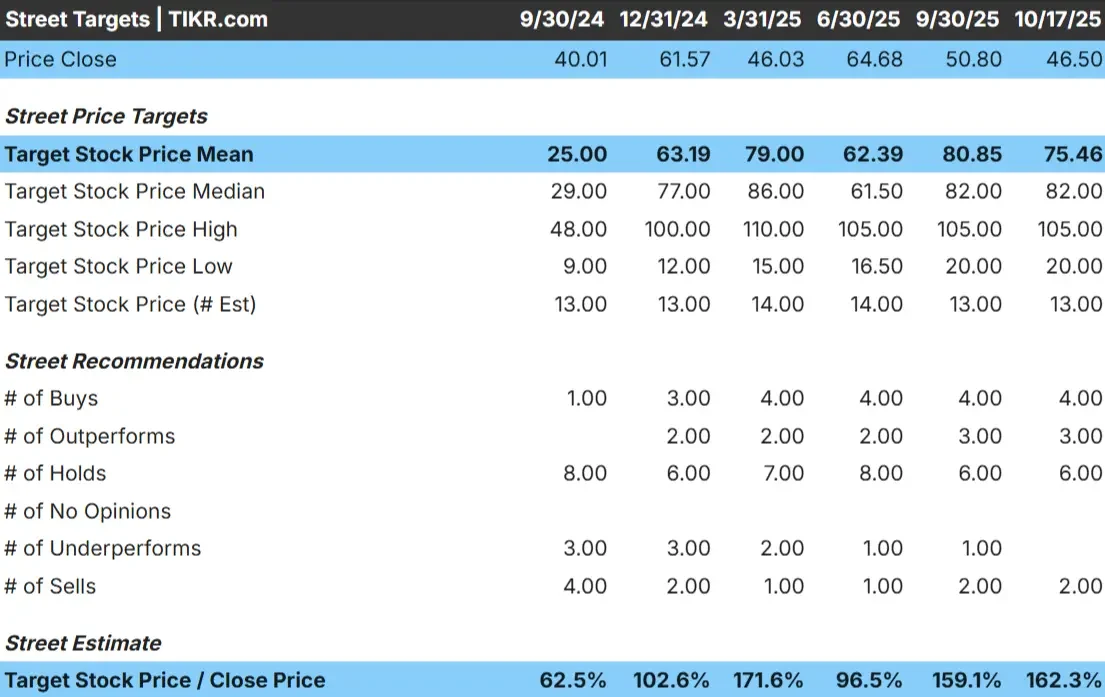

Upstart trades at about $47/share today. The average analyst price target is $75/share, which points to roughly 62% upside. Forecasts show a wide spread and reflect mixed conviction among analysts:

- High estimate: ~$105/share

- Low estimate: ~$20/share

- Median target: ~$82/share

- Ratings: 4 Buys, 3 Outperforms, 6 Holds, 2 Underperforms, 2 Sells

For investors, this suggests meaningful upside but also a wide range of possible outcomes. The gap between bullish and bearish targets reflects uncertainty around credit markets and how quickly Upstart can rebuild consistent loan volume and funding demand. Execution over the next few quarters will likely decide whether the stock’s recovery is sustained or short-lived.

See analysts’ growth forecasts and price targets for Upstart (It’s free!) >>>

Upstart: Growth Outlook and Valuation

The company’s fundamentals point to high growth potential but elevated risk:

- Revenue is expected to grow about 36% annually through 2027

- Operating margins could improve to roughly 9% as funding stabilize

- Shares trade at around 23× forward earnings, slightly above peers

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 23× forward P/E suggests ~ $120/share by 2027

- That implies about 158% total upside, or roughly 54% annualized returns

These figures show Upstart as a high-risk, high-reward opportunity within fintech. The valuation assumes meaningful execution on growth and margin recovery, leaving little room for error.

For investors, Upstart offers significant upside potential if its AI lending platform scales and profitability returns, but share price volatility could persist until funding and loan performance stabilize.

Value stocks like Upstart in as little as 60 seconds with TIKR (It’s free) >>>

What’s Driving the Optimism?

Upstart’s AI lending model remains one of the most advanced in the fintech space. Its technology allows partner banks to assess credit risk beyond traditional FICO scores, which can improve loan approvals without taking on excessive risk.

The company continues to add new lending partners and expand into areas like auto and small business loans, helping diversify its revenue base. As funding conditions improve, these efforts could fuel a strong rebound in transaction volumes and fee income.

For investors, this reinforces the idea that Upstart’s core technology advantage could translate into lasting growth once credit markets stabilize. Its platform is positioned at the intersection of AI and finance, two areas with significant long-term potential.

Bear Case: Profitability and Funding Dependence

Despite its promise, Upstart’s path to consistent profitability remains uncertain. The business is heavily reliant on external funding partners, which means loan volumes can fall sharply when capital markets tighten. This sensitivity makes the stock more volatile than most fintech peers.

Margins also remain under pressure, with rising costs tied to technology development and data infrastructure. Until loan funding becomes steadier and margins expand meaningfully, earnings visibility will stay limited.

For investors, the risk is that Upstart’s innovation alone may not be enough to sustain valuation gains if its funding network remains fragile. The story depends on stability, not just technology.

Outlook for 2027: What Could Upstart Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model suggests Upstart could trade near $120/share by 2027. That represents about 158% upside from current levels, or roughly 54% annualized returns, assuming growth targets are met.

While this would mark a strong recovery, it already assumes significant improvement in loan volumes, funding availability, and profitability. To deliver further upside, Upstart would need to scale faster, deepen lender partnerships, and prove that its AI credit models outperform traditional methods over time.

For investors, Upstart stands out as a high-upside but high-volatility stock. The company’s future hinges on execution and market conditions, making it best suited for investors comfortable with elevated risk in pursuit of potentially exceptional long-term returns.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Click here to sign up for TIKR and get your free copy of TIKR’s 5 AI Compounders report today.