Nancy Pelosi, the longtime Democratic leader and former Speaker of the House, has become as well-known on Wall Street as she is in Washington. Her uncanny ability to time the market has earned her a reputation far beyond politics, with some traders joking that following her disclosures is as valuable as any analyst report.

This interest has grown into what’s now called the “Pelosi stock tracker” phenomenon, where investors carefully monitor every trade she reports. In an era of heightened volatility, inflation concerns, and shifting interest rate policies, the logic is simple: if Pelosi is buying or selling, there may be a reason worth paying attention to.

Her most recent financial disclosures, filed on January 23, 2026, reveal a strong tilt toward technology, with a particular emphasis on artificial intelligence leaders driving the next wave of growth. The transactions show a combination of direct stock purchases and call option exercises spanning late December 2025 through mid-January 2026.

While tracking congressional trades is no substitute for fundamental analysis, these filings provide a window into where capital is flowing. Here is a closer look at the seven stocks that stand out from the most recent disclosures.

Find out what the top investors are buying with TIKR >>>

Stock #1: AllianceBernstein (AB)

AllianceBernstein stands out as Nancy Pelosi’s largest direct stock purchase in the January 2026 filings. She purchased 25,000 shares valued between $1 million and $5 million on January 16, 2026. The size of this position suggests meaningful conviction in the asset management space.

AllianceBernstein is a global investment management firm with approximately $865 billion in assets under management as of late 2025. The company operates across institutional, retail, and private wealth channels, with particular strength in fixed income strategies.

Recent results showed continued momentum in the active fixed income business. The firm reported record fixed-income inflows of $24.5 billion in 2024, roughly double the prior year’s. Credit strategies have been a key driver as institutional allocators shift capital back into bonds after years of underweighting.

The company trades at a meaningful discount to other publicly traded asset managers, with a distribution yield that appeals to income-focused investors. Management has emphasized expense discipline and operating leverage as AUM scales, which could support margin expansion if market conditions remain favorable.

AllianceBernstein plans to report fourth quarter 2025 results on February 5, 2026.

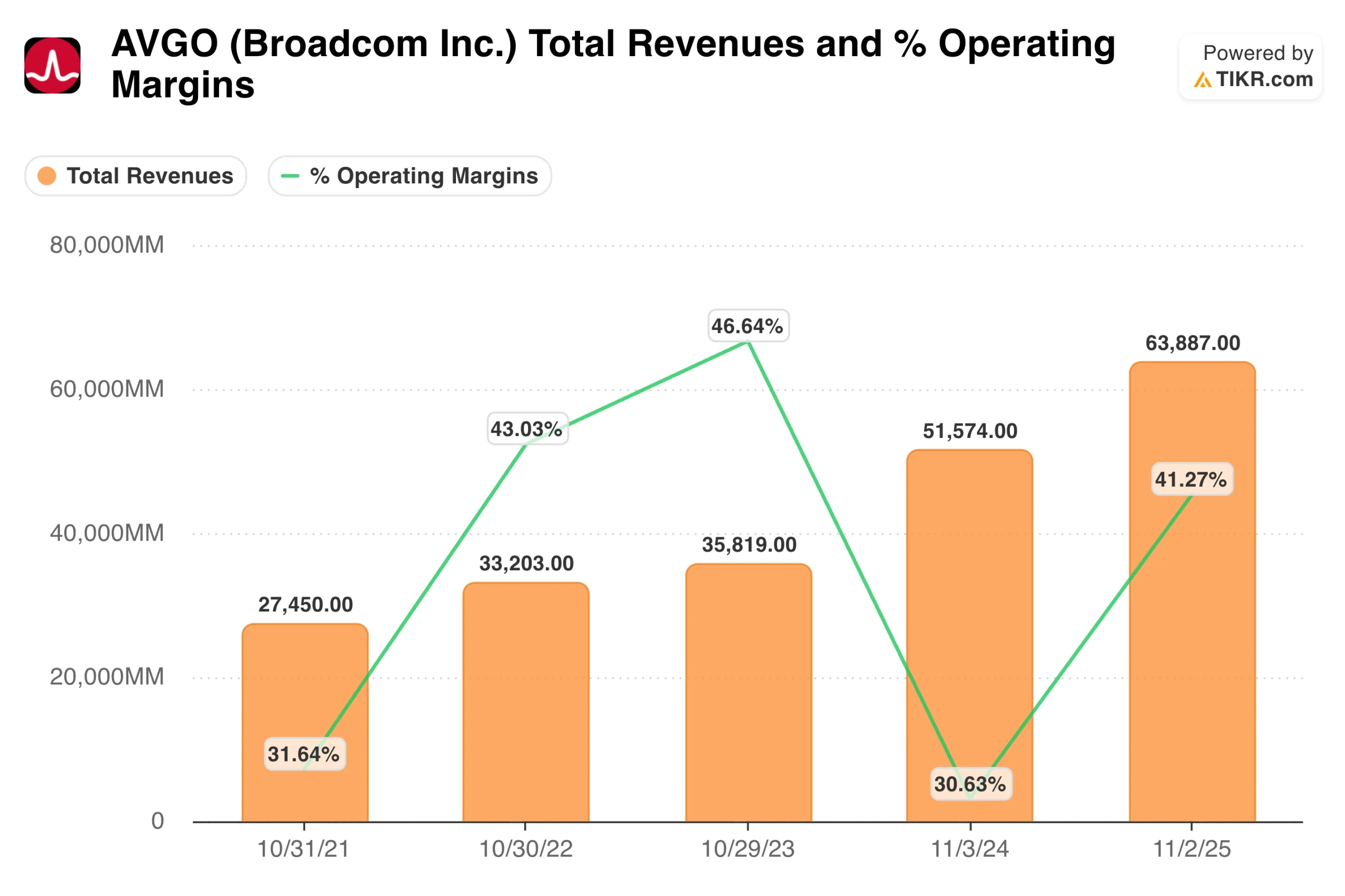

Stock #2: Broadcom (AVGO)

The next Nancy Pelosi stock on my list is Broadcom (AVGO), a chip maker also involved in the AI race. In June, Pelosi purchased 20 Broadcom call options with a split-adjusted strike price of $80 and a 12-month expiry.

Broadcom delivered another strong quarter in Q4 fiscal 2025, with revenue reaching $18.0 billion, up 28% year over year, driven primarily by AI demand and steady growth in infrastructure software.

AI semiconductor revenue jumped 74% year over year as hyperscale cloud customers ramped up spending on custom accelerators and networking solutions. Management noted that Broadcom is now working with four new hyperscalers on next-generation AI platforms, reinforcing its position as a core supplier inside global data centers.

Software revenue totaled $6.9 billion, supported by VMware, while profitability remained a standout. Broadcom generated $7.5 billion in free cash flow during the quarter and returned roughly $7 billion to shareholders through dividends and buybacks, underscoring the model’s cash-generating power.

Looking ahead, management guided to Q1 fiscal 2026 revenue of about $19.1 billion, up 28% year over year, with AI semiconductor revenue expected to double to $8.2 billion. As AI infrastructure spending accelerates, Broadcom remains squarely at the center of that buildout.

Find high-quality undervalued stocks with TIKR >>>

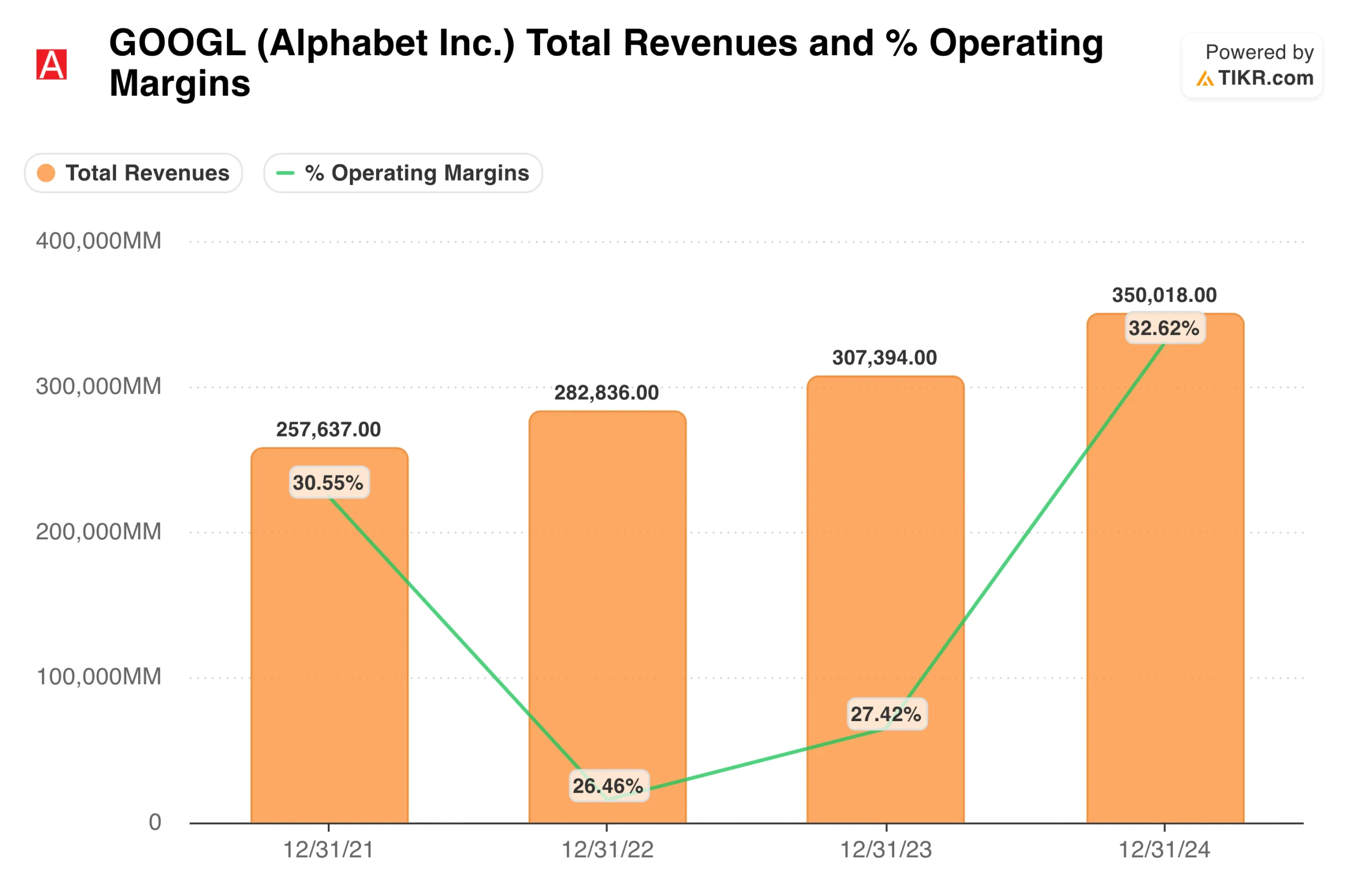

Stock #3: Alphabet (GOOGL)

Nancy Pelosi has taken a notable interest in Alphabet (GOOGL), with the stock appearing multiple times in her January disclosures. She exercised 50 call options valued between $500,000 and $1 million on January 16, 2026, following an earlier purchase of 20 call options valued between $250,000 and $500,000 in late December 2025. Her moves reflect growing investor conviction that Alphabet’s growth story remains intact.

Alphabet reported a strong third quarter 2025, with revenue reaching $102.35 billion, up 15.9% year over year. The results reflected continued strength in Search, YouTube, and an accelerating contribution from Google Cloud.

Google Cloud was the standout performer. Revenue grew 33.5% year over year to $15.2 billion, while the segment’s backlog surged 82% year over year. Enterprise customers continue to increase spending on data analytics, AI workloads, and infrastructure services.

Search revenue climbed to $56.6 billion, up 14.5% year over year, while YouTube advertising reached $10.3 billion. Management highlighted the continued rollout of Gemini models across Search, Workspace, and developer tools.

Alphabet plans to report fourth quarter 2025 results on February 4, 2026. Consensus expects revenue near $111.4 billion, up approximately 15.5% year over year, and EPS of $2.64, up 23% from the prior year.

Stock #4: Amazon (AMZN)

Nancy Pelosi has shown repeated interest in Amazon (AMZN), with multiple transactions appearing in the January filings. She exercised 50 call options valued between $500,000 and $1 million on January 16, 2026, and purchased an additional 20 call options valued between $100,000 and $250,000 in late December 2025. Her continued positioning in Amazon reflects confidence in the company’s diversified growth engines.

With a market cap near $2.6 trillion, Amazon remains one of the most diversified technology platforms in the world. The business spans e-commerce, cloud infrastructure, digital advertising, and logistics, with each segment operating at different stages of maturity and margin potential.

AWS continues to lead profitability. In the third quarter of 2025, AWS revenue grew 20% year over year to $33.0 billion while operating income reached $11.4 billion. Management highlighted accelerating adoption of AI infrastructure, with Trainium2 now a multibillion-dollar business that grew 150% quarter over quarter.

Advertising has emerged as another high-margin profit driver. Revenue climbed 24% year over year to $17.7 billion in Q3, with Amazon expanding its ad footprint across retail, video, and third-party platforms.

Analysts expect Amazon to report fourth-quarter 2025 earnings on February 5, 2026, with consensus calling for EPS of approximately $1.97, up 5.9% from the prior year.

Analyze stocks quicker with TIKR >>>

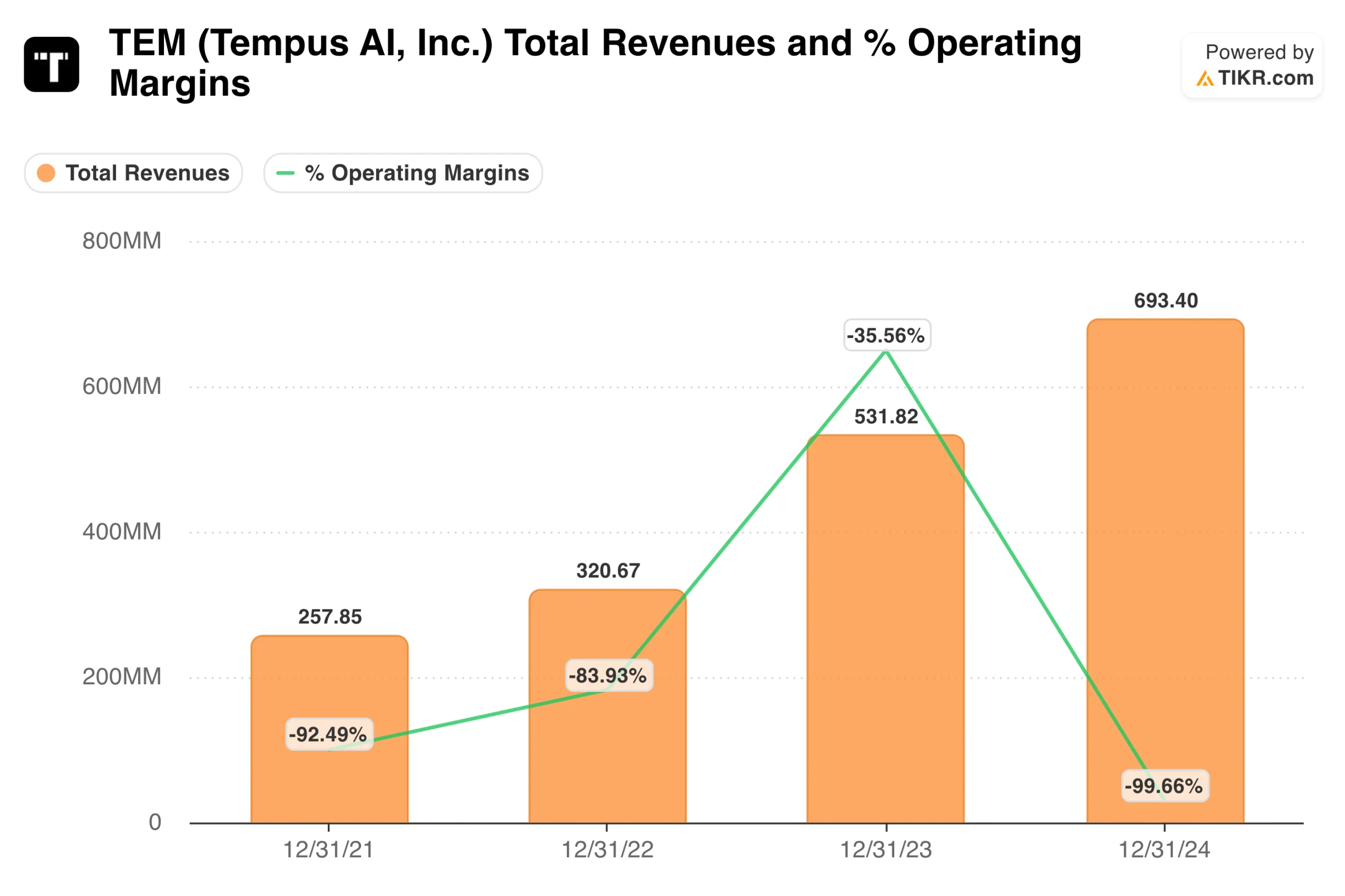

Stock #5: Tempus AI (TEM)

Tempus AI (TEM) remains one of the more speculative names in Nancy Pelosi’s portfolio, and she continues to add to the position. On January 16, 2026, she exercised 50 call options valued between $50,000 and $100,000. Her earlier trades in Tempus drew significant attention after the stock nearly tripled following disclosure of her initial position.

Tempus AI, now valued at more than $12 billion, operates at the center of precision medicine. The company applies AI to genomic and clinical datasets to help physicians make treatment decisions and to support drug discovery.

Preliminary results for the full year 2025 showed revenue of approximately $1.27 billion, representing 83% year-over-year growth and approximately 30% organic growth, excluding the Ambry acquisition. Diagnostics revenue reached approximately $955 million, up 111% year over year, driven by 26% growth in oncology volume and 29% growth in hereditary testing volume.

The Data and Applications segment delivered approximately $316 million in revenue, up 31% year over year. Within that segment, data licensing grew approximately 38%. Fourth quarter Data and Applications revenue reached a record of approximately $100 million, with Insights growing 68% excluding the prior-year AstraZeneca warrant impact.

CEO Eric Lefkofsky noted that the company enters 2026 in an exceptionally strong position, with both main business lines accelerating and delivering operating leverage.

Find stocks that analysts think have major upside >>>

Stock #6: Vistra (VST)

Nancy Pelosi has maintained her interest in the energy sector through Vistra (VST), a utility positioned at the intersection of power generation and AI infrastructure demand. She exercised 50 call options valued between $100,000 and $250,000 on January 16, 2026, signaling continued confidence in the company’s growth trajectory.

Vistra is a Fortune 500 integrated retail electricity and power generation company based in Irving, Texas. The company operates a diversified fleet of natural gas, nuclear, coal, solar, and battery storage facilities while serving approximately 5 million retail customers.

The company narrowed its 2025 adjusted EBITDA guidance to $5.7 billion to $5.9 billion and introduced 2026 guidance of $6.8 billion to $7.6 billion. Management also set a 2027 adjusted EBITDA midpoint opportunity range of $7.4 billion to $7.8 billion.

Recent strategic activity includes a 20-year power purchase agreement at Comanche Peak, enabling a customer to energize up to 1,200 megawatts of new load. The company also acquired approximately 2.6 gigawatts of natural gas-fired assets from Lotus Infrastructure Partners.

Since 2021, Vistra has returned over $6.7 billion to shareholders through buybacks and dividends, with an additional $2.9 billion planned. The company has reduced its share count by approximately 30% since November 2021.

Vistra will report fourth-quarter and full-year 2025 results on February 26, 2026.

Stock #7: NVIDIA (NVDA)

Continuing to focus on AI positions, Nancy Pelosi is building exposure to the buildout of the AI infrastructure market through NVIDIA (NVDA). She exercised 50 call options valued between $250,000 and $500,000 on January 16, 2026, and purchased 20 call options valued between $100,000 and $250,000 in late December 2025. Her positioning in NVIDIA signals confidence in the durability of AI-driven semiconductor demand.

NVIDIA reported record results for fiscal Q4 2025 (ended January 26, 2025), with revenue of $39.3 billion, up 78% year over year and 12% sequentially. Data Center revenue reached a record $35.6 billion, driven by continued demand from hyperscalers and enterprises for AI compute.

Full fiscal year 2025 revenue totaled $130.5 billion, up 114% from the prior year. GAAP earnings per diluted share reached $2.94, up 147% year over year.

Management guided for Q1 fiscal 2026 revenue of approximately $43 billion, with GAAP gross margins expected to be near 70.6%. CEO Jensen Huang noted that demand for Blackwell remains strong as reasoning AI creates another scaling law for compute intensity.

NVIDIA is expected to report fiscal Q4 2026 results on February 25, 2026.

Track company financials, stock value, and competitor information with TIKR (It’s free) >>>

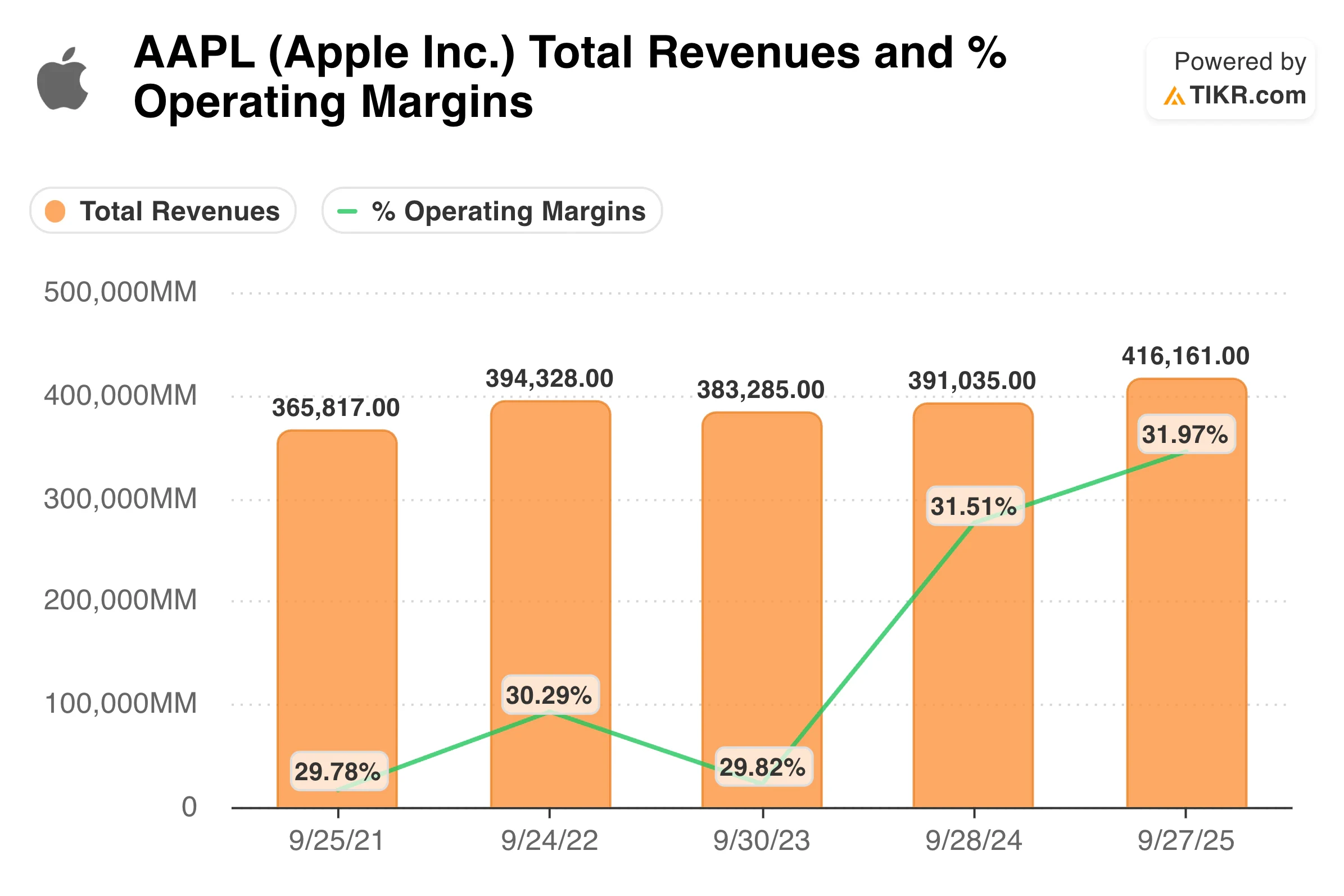

Stock #8: Apple (AAPL)

Apple (AAPL) rounds out the notable positions in Pelosi’s January 2026 filings. She purchased 20 call options valued between $250,000 and $500,000 on December 30, 2025. The filings also showed share sales and contributions totaling between $10 million and $50 million around the same period, suggesting portfolio rebalancing rather than a directional bet against the stock.

Apple reported record fiscal Q4 2025 results (ended September 27, 2025), with revenue of $102.5 billion, up 8% year over year, and diluted EPS of $1.85, up 13% year over year on an adjusted basis. Full-year 2025 revenue reached $416 billion.

Services remained the standout, with revenue climbing by more than 15% to an all-time record of $28.75 billion. Margins in the segment expanded to 75.3%, and for the first time, Services overtook iPhone as the largest contributor to gross profit.

iPhone revenue reached $49.03 billion, up 6% year over year. Mac revenue grew 13% to $8.7 billion. CEO Tim Cook guided fiscal Q1 2026 growth of 10% to 12% year over year, citing strong demand for the iPhone 17 lineup.

Analysts expect Apple to report fiscal Q1 2026 results on January 30, 2026, with consensus calling for revenue of approximately $137.5 billion and EPS of $2.65.

How to Accurately Value a Stock in Under 30 Seconds

With TIKR’s new Valuation Model tool, you can accurately estimate a stock’s potential share price in 30 seconds or less.

All it takes are three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR will enter analysts’ consensus estimates for you.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued today.

See a stock’s true value in under 30 seconds (Free with TIKR) >>>

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!