Mondelez International, Inc. (NASDAQ: MDLZ) has been under pressure, with shares down about 12% over the past year. The stock now trades near $62/share, as weak volumes and rising input costs have weighed on performance. Still, the company’s powerful portfolio of brands like Oreo, Cadbury, and Toblerone keeps analysts optimistic about a gradual rebound.

Recently, Mondelez reported quarterly results that highlighted its resilience in a tough consumer environment. Pricing gains helped offset softer volumes, while the company continued expanding in emerging markets and launched new innovations under its Oreo and Clif Bar brands. Management also reaffirmed its focus on margin recovery and cash flow discipline, signaling confidence in the business heading into 2026.

This article explores where Wall Street analysts expect Mondelez to trade by 2027. We’ve combined consensus forecasts and TIKR’s valuation models to outline the stock’s potential path based on current market expectations. These figures reflect analyst estimates, not TIKR’s own predictions.

Unlock our Free Report: 5 AI compounders that analysts believe are undervalued and could deliver years of outperformance with accelerating AI adoption (Sign up for TIKR, it’s free) >>>

Analyst Price Targets Suggest Modest Upside

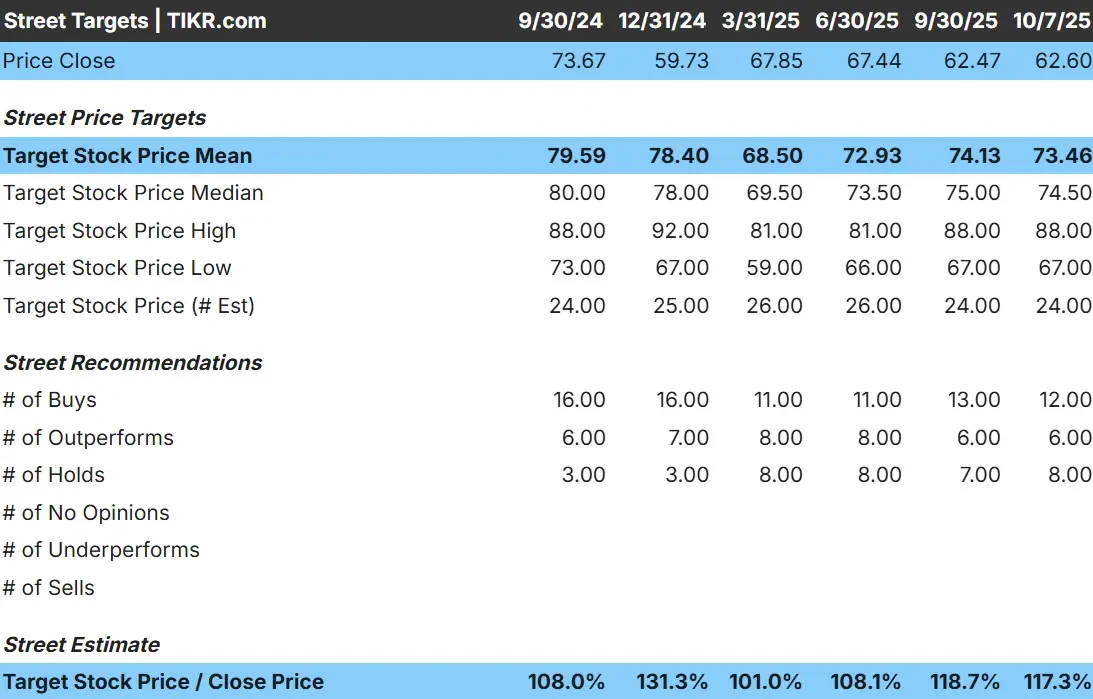

Mondelez trades at about $62/share today. The average analyst price target is $73/share, suggesting roughly 17% upside over the next year. Forecasts remain relatively close, reflecting cautious optimism across Wall Street:

- High estimate: ~$88/share

- Low estimate: ~$67/share

- Median target: ~$75/share

- Ratings: 12 Buys, 6 Outperforms, 8 Holds

For investors, this points to modest upside potential. Analysts see Mondelez as a reliable compounder rather than a high-growth story, with returns driven more by consistent cash flow and brand resilience than rapid expansion. The stock could outperform if volume trends recover or if cost pressures ease faster than expected.

See analysts’ growth forecasts and price targets for Mondelez (It’s free!) >>>

Mondelez: Growth Outlook and Valuation

The company’s fundamentals appear steady and well-balanced:

- Revenue Growth (CAGR 2025–2027): ~4.6%

- Operating Margin: ~14.9%

- Forward P/E: ~20×

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 19× forward P/E suggests ~$79/share by 2027

- That implies about +27% upside, or roughly 11% annualized returns

These projections show Mondelez can continue compounding at a moderate pace through pricing power and disciplined execution. The 3.3% dividend yield adds a layer of income stability, making it appealing for long-term investors who value dependable returns over short-term excitement.

For investors, Mondelez looks like a steady, cash-rich business capable of gradual value creation. While growth may stay moderate, its global scale and strong brands help cushion earnings through economic cycles.

Value stocks like Mondelez in as little as 60 seconds with TIKR (It’s free) >>>

What’s Driving the Optimism?

Mondelez continues to show resilience through strong pricing power and global brand leadership. Its core products like Oreo, Cadbury, and Ritz maintain dominant shelf space, allowing the company to offset weaker volumes with steady price increases.

Recent innovation, including expansions in emerging markets and product extensions under Clif Bar and BelVita, is helping sustain growth momentum. Management’s focus on productivity and cost control has also supported margins near 15%, even with elevated input costs.

For investors, these strengths suggest Mondelez can deliver steady earnings and cash flow growth despite a challenging consumer environment. The company’s scale, pricing discipline, and brand strength remain key advantages that should continue driving long-term value.

Bear Case: Sluggish Growth and Cost Pressure

Even with these positives, Mondelez’s growth profile remains modest. Volumes have been slow to recover, and inflation continues to weigh on profitability. Consumers in key markets are shifting toward cheaper local or private-label options, limiting the company’s pricing flexibility.

Competition across global snacking is also intensifying, with peers like Nestlé and Hershey expanding aggressively. Without stronger volume growth, Mondelez may see margins flatten and earnings growth slow.

For investors, the risk is that Mondelez maintains stability but lacks a clear catalyst for acceleration. While downside appears limited due to its brand quality and dividends, the upside may stay capped if demand doesn’t pick up meaningfully.

Outlook for 2027: What Could Mondelez Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 19× forward P/E suggests ~$79/share by 2027. That would represent about 27% upside from today, or roughly 11% annualized returns.

For investors, this outlook signals slow but consistent compounding potential. Mondelez is positioned to keep generating strong cash flow, maintain its dividend, and gradually expand margins through disciplined execution.

While the valuation already reflects much of this stability, stronger volume recovery or faster cost normalization could drive additional upside. Overall, Mondelez looks like a dependable long-term holding for those seeking predictable returns from a high-quality global snacking leader.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Click here to sign up for TIKR and get your free copy of TIKR’s 5 AI Compounders report today.