Hyatt Hotels Corporation (NYSE: H) has delivered strong results in recent years but faces a tougher backdrop as growth cools and leverage remains elevated. The stock trades near $143/share, down about 7% over the past year, as investors weigh premium valuation levels against slowing industry momentum.

Recently, Hyatt posted solid quarterly results, driven by double-digit growth in management fees and continued strength in its luxury and lifestyle brands. The company also announced new openings across Asia and the Middle East and revealed plans to acquire the Standard International hotel platform, signaling confidence in long-term expansion. These moves underscore Hyatt’s push toward an asset-light, high-margin model that aims to deliver steadier profitability.

This article explores where Wall Street analysts think Hyatt could trade by 2027. We’ve pulled together consensus price targets and valuation models to outline the stock’s potential trajectory. These figures reflect analyst expectations and not TIKR’s own predictions.

Unlock our Free Report: 5 AI compounders that analysts believe are undervalued and could deliver years of outperformance with accelerating AI adoption (Sign up for TIKR, it’s free) >>>

Analyst Price Targets Suggest Modest Upside

Hyatt trades at about $143/share today. The average analyst price target is $158/share, which points to roughly 11% upside over the next year. Forecasts show a moderate spread, reflecting mixed conviction across Wall Street:

- High estimate: ~$198/share

- Low estimate: ~$140/share

- Median target: ~$151/share

- Ratings: 10 Buys, 1 Outperform, 10 Holds, 1 Underperform, 1 Sell

For investors, this points to a modest upside scenario. Most analysts see Hyatt as a steady operator with solid fundamentals. The upside case would likely require stronger earnings momentum, further international expansion, or continued debt reduction to justify a higher valuation.

See analysts’ growth forecasts and price targets for Hyatt (It’s free!) >>>

Hyatt: Growth Outlook and Valuation

Hyatt’s fundamentals appear solid, supported by resilient travel demand and continued expansion in its luxury and lifestyle brands. The company’s fee-based model is helping boost margins while maintaining strong global visibility.

- Revenue growth forecast: ~6.3% annually through 2027

- Operating margin: improving to about 8.6%

- Forward P/E: ~42x, above peer averages

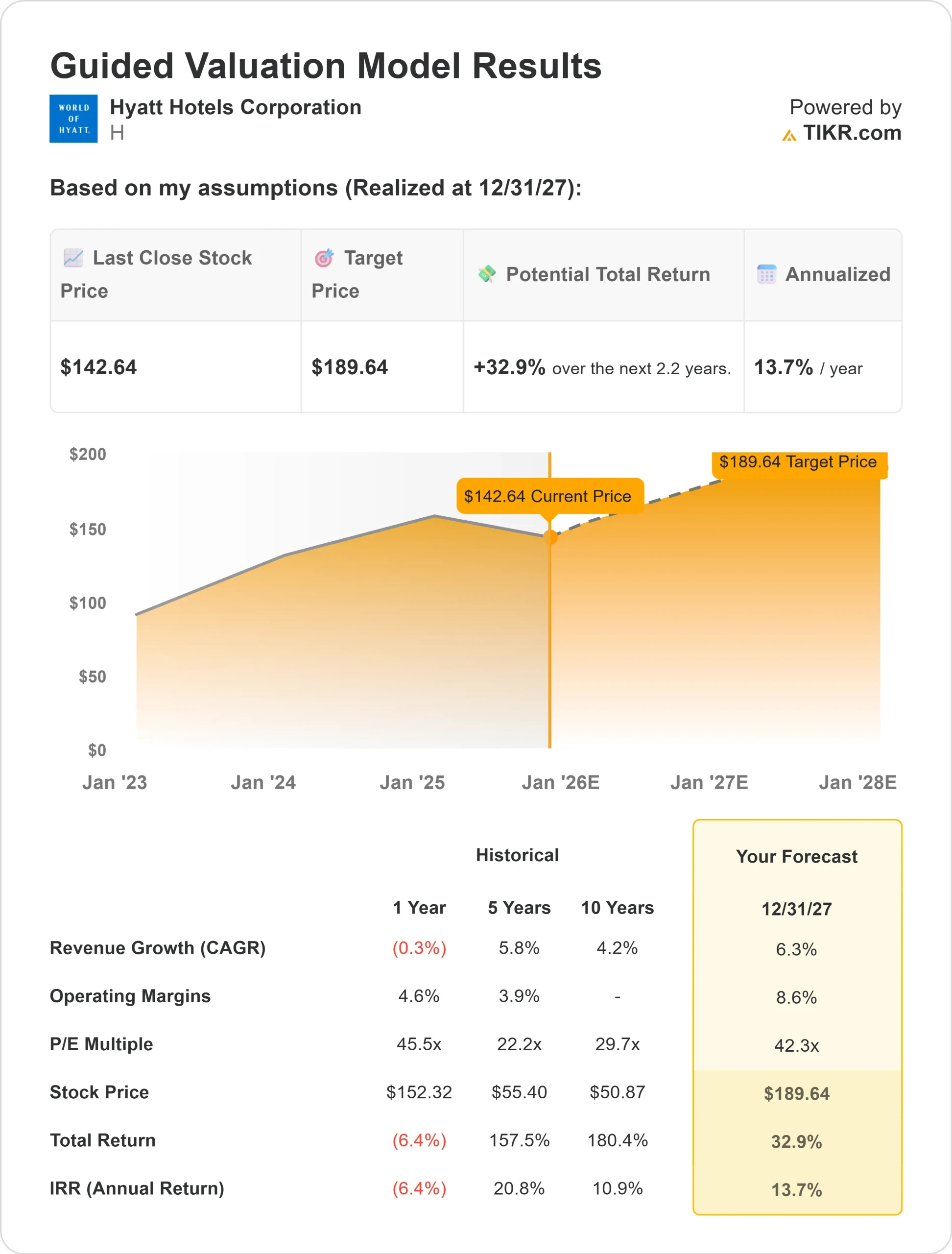

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 42x forward P/E suggests: ~$190/share by 2027

- That implies about 33% upside, or roughly 14% annualized returns

For investors, these numbers suggest Hyatt can deliver steady compounding returns if its growth strategy stays on track. However, the stock’s premium valuation already reflects optimism, leaving limited room for missteps if travel trends or margins weaken.

Value stocks like Hyatt in as little as 60 seconds with TIKR (It’s free) >>>

What’s Driving the Optimism?

Hyatt continues to benefit from strong global travel demand and its leadership in the luxury and lifestyle space. The company’s management and franchise fee growth is helping drive higher profitability, while new developments in Asia and the Middle East are adding to long-term earnings visibility.

Management’s disciplined cost structure and asset-light strategy provide flexibility and strong cash flow generation. For investors, these strengths suggest Hyatt can sustain profitability and deliver consistent value creation even as the broader travel cycle normalizes.

Bear Case: Valuation and Debt Load

Despite solid fundamentals, Hyatt’s valuation remains demanding given its modest growth outlook. The company trades at a premium multiple and carries net debt around 6.5x EBITDA, limiting flexibility if demand softens.

Its dividend yield of only 0.4% means most of the potential return relies on price appreciation. For investors, the risk is that Hyatt’s current valuation already prices in strong execution. Any slowdown in travel or persistent inflation could pressure margins and weigh on sentiment.

Outlook for 2027: What Could Hyatt Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 42x forward P/E suggests Hyatt could trade near $190/share by 2027. That represents about 33% total upside, or roughly 14% annualized returns from current levels.

While this outlook points to healthy returns, it already assumes steady global travel and consistent execution. For investors, Hyatt looks like a high-quality operator offering moderate growth and predictable earnings. Upside potential exists, but it depends on sustained fee growth, disciplined debt management, and continued success in expanding its luxury footprint.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Click here to sign up for TIKR and get your free copy of TIKR’s 5 AI Compounders report today.