General Electric Company (NYSE: GE) has transformed into a focused aerospace leader after years of restructuring. The stock has surged more than 60% in the past year, driven by strong demand for jet engines, improving margins, and confidence in GE’s streamlined business model.

Recently, GE reported better-than-expected earnings as its aerospace segment delivered double-digit growth in commercial engine services and equipment. Management also raised full-year guidance, citing robust demand from Boeing and Airbus, while reaffirming plans to return additional cash to shareholders through buybacks and dividends. These results reinforced investor confidence that GE’s turnaround is entering a new growth phase.

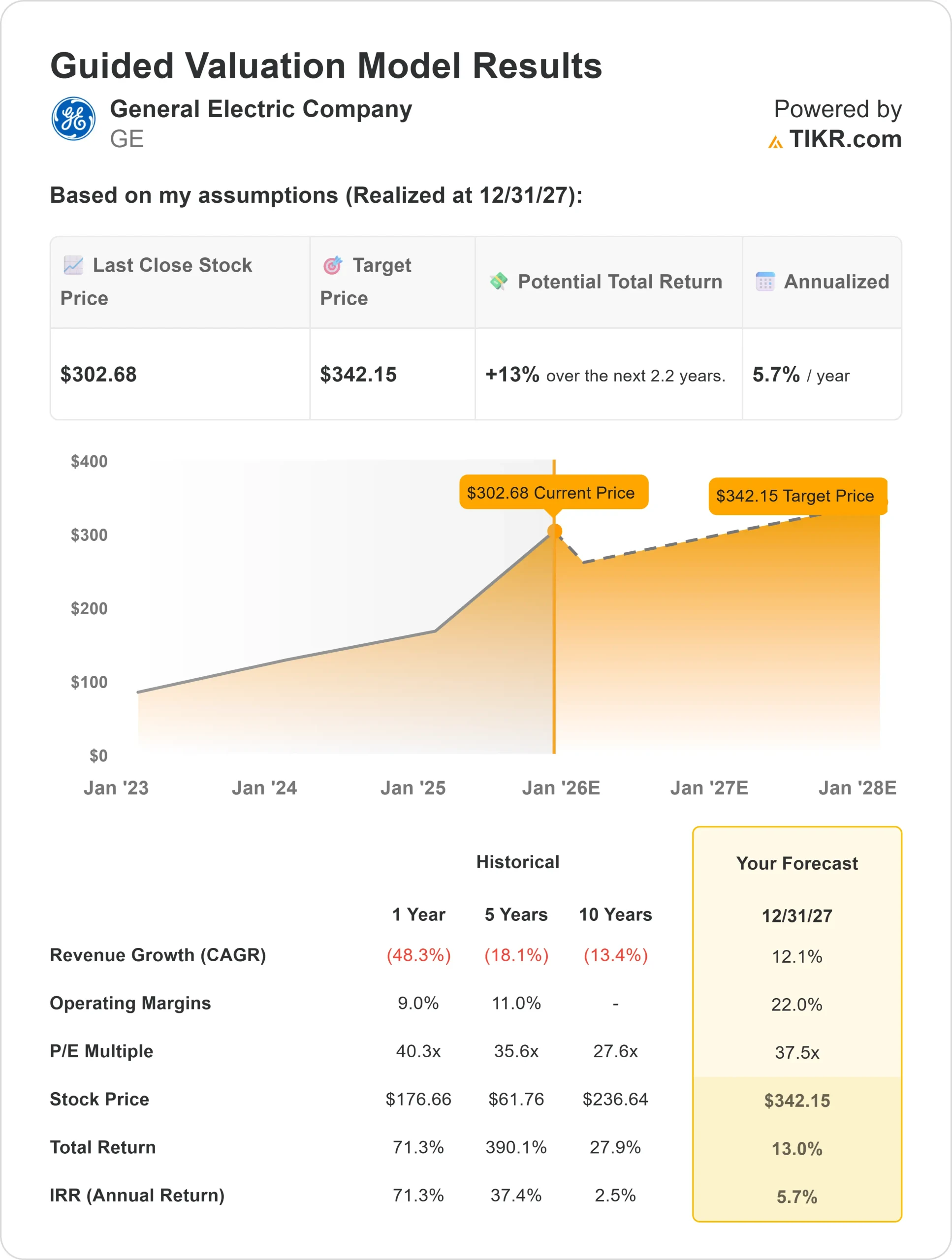

At around $306/share, investors now view GE as a high-quality compounder, though upside appears moderate after a sharp rally. This article explores where Wall Street analysts think GE could trade by 2027, combining consensus targets and TIKR’s Guided Valuation Model to outline the stock’s potential path. These figures reflect current analyst expectations and are not TIKR’s own predictions.

Unlock our Free Report: 5 AI compounders that analysts believe are undervalued and could deliver years of outperformance with accelerating AI adoption (Sign up for TIKR, it’s free) >>>

Analyst Price Targets Suggest Modest Upside

GE trades at about $306/share today. The average analyst price target sits around $322/share, suggesting roughly 6% upside over the next year. Forecasts show a relatively tight spread, signaling confidence in GE’s earnings outlook:

- High estimate: ~$374/share

- Low estimate: ~$266/share

- Median target: ~$330/share

- Ratings: 11 Buys, 2 Outperforms, 1 Hold, 1 Underperforms

The modest upside tells investors that most of the turnaround optimism is already priced in. Analysts see GE as a high-quality industrial compounder rather than a rapid-growth story. Future gains will likely depend on management’s ability to sustain margin expansion and maintain free cash flow strength as demand normalizes.

See analysts’ growth forecasts and price targets for General Electric (It’s free!) >>>

GE: Growth Outlook and Valuation

GE’s fundamentals remain strong, supported by consistent demand for commercial and defense engines, margin expansion, and solid cash generation.

- Revenue Growth (2023–2027E): ~12% annually

- Operating Margin (2027E): ~22%

- Shares trade at: ~37× forward earnings

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 37× forward P/E suggests around $342/share by 2027,

- That implies roughly 13% total upside or about 5.7% annualized returns.

For investors, this means GE is positioned for steady, predictable growth rather than outsized gains. The valuation reflects confidence in the aerospace cycle’s strength, but to deliver stronger returns, GE would need to exceed earnings forecasts or unlock new profit levers through cost efficiencies and technology-driven growth.

Value stocks like General Electric in as little as 60 seconds with TIKR (It’s free) >>>

What’s Driving the Optimism?

GE Aerospace is benefiting from one of the strongest aviation recoveries in decades. Airlines are ramping up engine orders as global air travel surpasses pre-pandemic levels, and GE’s service contracts are generating stable, high-margin revenue. The company’s defense segment is also expanding, supported by long-term military engine programs that add visibility to future earnings.

Management’s focus on efficiency and disciplined cost control is driving margin gains, while strong free cash flow is giving GE room to reinvest and return capital to shareholders. For investors, these strengths highlight a business that is not just recovering but building durable profitability as the aerospace cycle matures.

Bear Case: High Expectations and Valuation Risk

Even with these positives, GE’s valuation leaves little room for disappointment. The stock trades around 37× forward earnings, which is high for an industrial company. Any slowdown in air traffic recovery, supply chain pressure, or cost overruns could quickly limit upside.

Competition from Pratt & Whitney and Rolls-Royce remains fierce, especially in next-generation engine programs where pricing power is key. For investors, the risk is that even minor execution missteps or macro slowdowns could compress GE’s premium multiple.

Outlook for 2027: What Could GE Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 37× forward P/E suggests GE could trade near $342/share by 2027, implying about 13% total upside or roughly 5.7% annualized returns.

This forecast assumes strong earnings follow-through and sustained momentum across both commercial and defense markets. While that would mark solid progress, much of this optimism is already reflected in today’s valuation.

For investors, GE looks like a reliable long-term compounder rather than a breakout opportunity. Future gains will likely depend on continued margin expansion, execution consistency, and GE’s ability to capture a larger share of the global aerospace market.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Click here to sign up for TIKR and get your free copy of TIKR’s 5 AI Compounders report today.