Estée Lauder (NYSE: EL) has faced one of its toughest stretches in years. Sales weakness in China and travel retail, coupled with rising costs, dragged shares down to about $88/share. Over the past year, the stock is still down roughly 7%, reflecting investor caution about its recovery pace.

Recently, the company reported fiscal Q4 results that showed early signs of stabilization, with skincare sales rebounding and Asia-Pacific demand improving. Management also unveiled a new multi-year restructuring program aimed at simplifying operations and cutting $1.1 billion in costs by 2026. Meanwhile, strong early demand for its luxury fragrances and La Mer skincare line highlights the brand’s continued pricing power even in a soft retail environment.

This article explores where Wall Street analysts think Estée Lauder could trade by 2028. We’ve pulled together consensus price targets and valuation models to outline the stock’s potential recovery path. These figures reflect analyst expectations and not TIKR’s own predictions.

Unlock our Free Report: 5 AI compounders that analysts believe are undervalued and could deliver years of outperformance with accelerating AI adoption (Sign up for TIKR, it’s free) >>>

Analyst Price Targets Suggest Limited Upside

Estée Lauder trades near $88/share today. The average analyst price target is around $93/share, implying roughly 6% upside over the next year. Forecasts remain mixed:

- High estimate: ~$120/share

- Low estimate: ~$61/share

- Median target: ~$90/share

- Ratings: 4 Buys, 3 Outperforms, 19 Holds, 1 Sell

With only about 6% implied upside, analysts appear to view Estée Lauder as mostly priced in for now. The broad range between high and low forecasts reflects uncertainty about the pace of recovery in key markets like China and travel retail.

For investors, this means expectations are muted in the near term. The stock could outperform only if management delivers faster margin expansion or stronger global demand than currently anticipated.

See analysts’ growth forecasts and price targets for Estée Lauder (It’s free!) >>>

Estée Lauder: Growth Outlook and Valuation

Estée Lauder’s fundamentals are improving, though the recovery remains gradual:

- Revenue is projected to grow about 3.9% annually through 2028

- Operating margins are expected to recover to around 11.6%

- Shares trade near 39x forward earnings, above most peers

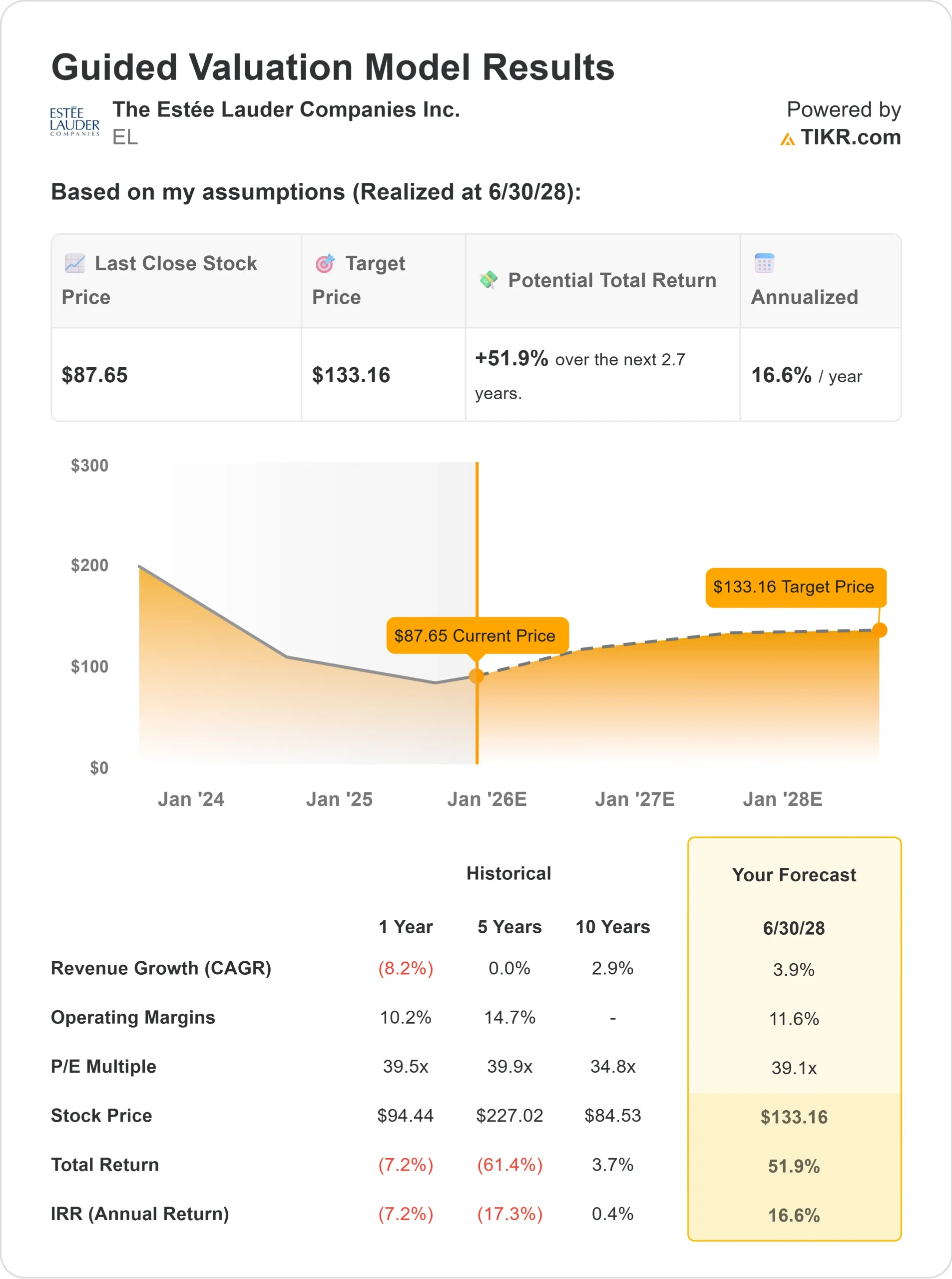

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 39x forward P/E suggests ~$133/share by 2028

- That represents about 52% total upside, or roughly 16.6% annualized returns

For investors, these numbers imply a steady rebound scenario. Estée Lauder’s valuation already reflects some optimism, so sustained earnings growth and consistent execution will be key. The company’s strong brand portfolio and disciplined cost management provide a credible path toward recovery, but patience remains essential.

Value stocks like Estée Lauder in as little as 60 seconds with TIKR (It’s free) >>>

What’s Driving the Optimism?

Estée Lauder remains one of the most respected names in global prestige beauty. Demand is gradually improving across Asia-Pacific, and travel retail is showing signs of recovery. The company’s focus on premium skincare and fragrance products supports pricing power, while operational efficiencies are beginning to lift margins.

Management’s restructuring plan and automation initiatives are helping streamline the business and reduce complexity. For investors, these changes indicate that the turnaround is on track. With healthier margins and a more focused cost base, Estée Lauder is rebuilding a foundation for sustainable long-term growth.

Bear Case: Slow Growth and Premium Valuation

Even with progress underway, challenges remain. Revenue growth is modest, and competition from L’Oréal, Shiseido, and emerging brands continues to intensify. The company’s heavy reliance on travel retail and China still poses risks if those markets recover more slowly than expected.

At roughly 39x forward earnings, the stock also trades at a premium compared to peers. For investors, this means limited margin for error. If cost savings or growth fall short, the valuation could restrict near-term returns despite improving fundamentals.

Outlook for 2028: What Could Estée Lauder Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 39x forward P/E suggests Estée Lauder could trade near $133/share by 2028. That represents about 52% total upside, or approximately 16.6% annualized returns from current levels.

This projection assumes moderate revenue growth, improving profitability, and ongoing cost discipline. It reflects a balanced view that is achievable if the company continues executing well, but not guaranteed.

For investors, Estée Lauder looks like a patient turnaround opportunity. The brand’s resilience, disciplined restructuring, and early signs of demand recovery could quietly compound into attractive long-term returns as the company regains its footing.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Click here to sign up for TIKR and get your free copy of TIKR’s 5 AI Compounders report today.