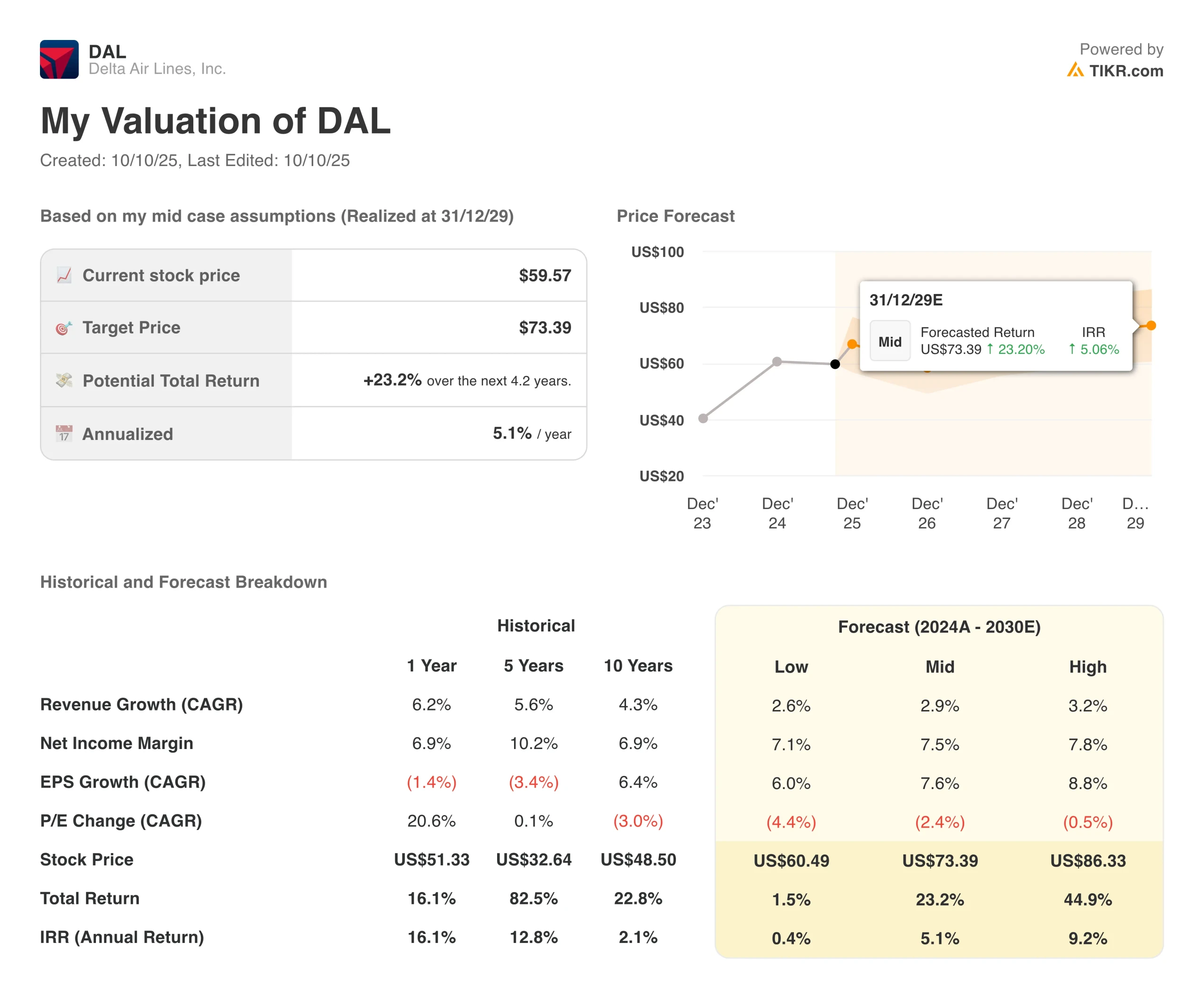

Key Stats for $DAL Stock

- Price Change for $DAL stock: 4.3%

- Current Share Price: $60

- 52-Week High: $70

- $DAL Stock Price Target: $71

What Happened?

Delta Air Lines (DAL) stock jumped 4% on Thursday after the company reported third-quarter earnings that crushed Wall Street expectations and issued strong guidance for the rest of the year.

The Atlanta-based carrier posted adjusted earnings of $1.71 per share on revenue of $16.67 billion, both comfortably ahead of analyst estimates.

More importantly, Delta forecast fourth-quarter earnings of $1.60 to $1.90 per share, above the $1.65 that Wall Street expected. The airline said revenue would grow as much as 4% in the final three months of the year, nearly double the 1.7% analysts projected.

CEO Ed Bastian said Delta is well-positioned to deliver top-line growth and margin expansion in 2026, consistent with the company’s long-term financial framework. The strong outlook signals improving demand and less oversupply of flights that had pushed domestic fares down earlier this year.

The results show premium travel continues dominating Delta’s business. Revenue from high-end segments, including first class and roomier economy seats, jumped 9% in the third quarter to nearly $5.8 billion. Main cabin revenue fell 4% to about $6 billion during the same period.

Bastian said there were no signs of consumer pullback for premium products. President Glen Hauenstein reiterated that revenue from Delta’s upmarket options, such as first class, is on track to eclipse main cabin sales next year, potentially as soon as a quarter or two into 2026.

Corporate travel also showed strength, up 8% year over year with sequential improvement across all sectors. Domestic corporate sales grew double digits, including mid-teens growth in coastal hubs. That momentum matters as 30-40% of premium revenue comes from corporate travelers.

Delta’s SkyMiles loyalty program continues to generate significant revenue. Remuneration from American Express increased 12% to $2 billion in the quarter, keeping the airline on track to deliver over $8 billion this year. Co-brand card spending grew at a double-digit pace, driven by a record mix of customers choosing premium cards.

The airline generated free cash flow of $830 million in the quarter, bringing year-to-date free cash to $2.8 billion. Delta updated its full-year free cash flow outlook to $3.5 billion to $4 billion, reflecting an increase in cash generation compared to the previous year.

See analysts’ growth forecasts and price targets for DAL stock (It’s free!) >>>

What the Market Is Telling Us About DAL Stock

The 4% jump in DAL stock reflects investor confidence that the airline industry bifurcation is accelerating in Delta’s favor. The company expects to capture roughly 60% of overall industry profits this quarter, with United Airlines likely taking most of the rest.

The gap between premium carriers like Delta and budget airlines continues to widen. Lower-end carriers rely on high growth and low fares, but struggle to attract capital when they fail to cover their cost of capital.

Delta’s competitive advantages have never been more evident. The airline delivered an 11.2% operating margin and 13% return on invested capital, five points above its cost of capital. Those returns put Delta in the top half of the S&P 500, not just among airlines.

The premium travel story shows no signs of slowing, given that Delta has increased premium seating through both new aircraft deliveries and retrofits of existing planes.

Premium products used to be loss leaders a decade ago. Now they’re the highest margin offerings, and the margins descend with the level of premiumness.

International profitability remained strong across all entities despite a disappointing 7% revenue decline in the Atlantic. Hauenstein said the airline will be more aggressive in building a solid book earlier next year and will adjust summer capacity to flatten out peak periods.

Notably, the federal government shutdown hasn’t impacted operations yet, but Bastian said that could change if it continues another 10 days. Inflation on maintenance and parts stays elevated as the supply chain struggles to normalize.

But for investors betting on DAL stock, the thesis looks increasingly solid. Delta is capturing share from weaker competitors while premium demand holds strong. Free cash flow generation enables debt paydown and shareholder returns while maintaining a fortress balance sheet.

The airline raised full-year earnings guidance to approximately $6 per share, the upper end of its July range. The industry bifurcation Bastian described on CNBC isn’t temporary. It’s structural. And Delta sits firmly on the winning side.

Wall Street Analysts Are Bullish on These 5 Undervalued Compounders With Market-Beating Potential

TIKR just released a new free report on 5 compounders that appear undervalued, have beaten the market in the past, and could continue to outperform on a 1-5 year timeline based on analysts’ estimates.

Inside, you’ll get a breakdown of 5 high-quality businesses with:

- Strong revenue growth and durable competitive advantages

- Attractive valuations based on forward earnings and expected earnings growth

- Long-term upside potential backed by analyst forecasts and TIKR’s valuation models

These are the kinds of stocks that can deliver massive long-term returns, especially if you catch them while they’re still trading at a discount.

Whether you’re a long-term investor or just looking for great businesses trading below fair value, this report will help you zero in on high-upside opportunities.

Click here to sign up for TIKR and get our full report on 5 undervalued compounders completely free.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!