Flight Centre Travel Group (FLT) enters 2026 after a turbulent year that tested the resilience of global travel operators. The company faced geopolitical tensions, shifting consumer behavior, and a soft leisure-travel environment, all of which weighed on profitability. Even with these challenges, FLT delivered a record A$24.5 billion in total transaction value and demonstrated that its core business remains fundamentally strong.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free)>>>

The corporate division continued to perform well, securing new global accounts, expanding its technology-led offerings, and strengthening its market position in the United States and Canada. Meanwhile, the leisure business showed signs of structural improvement, driven by higher productivity, rapid expansion in the cruise and luxury segments, and the scaling of independent and online channels.

FLT’s cost discipline, investments in AI-driven tools, and plans for a new loyalty program reflect a company preparing for a more stable travel cycle. Management believes many of FY25’s headwinds were temporary and that improving demand indicators will help drive a healthier trajectory into FY26 and beyond.

Quickly value any stock with TIKR’s powerful new Valuation Model (It’s free!) >>>

Financial Story

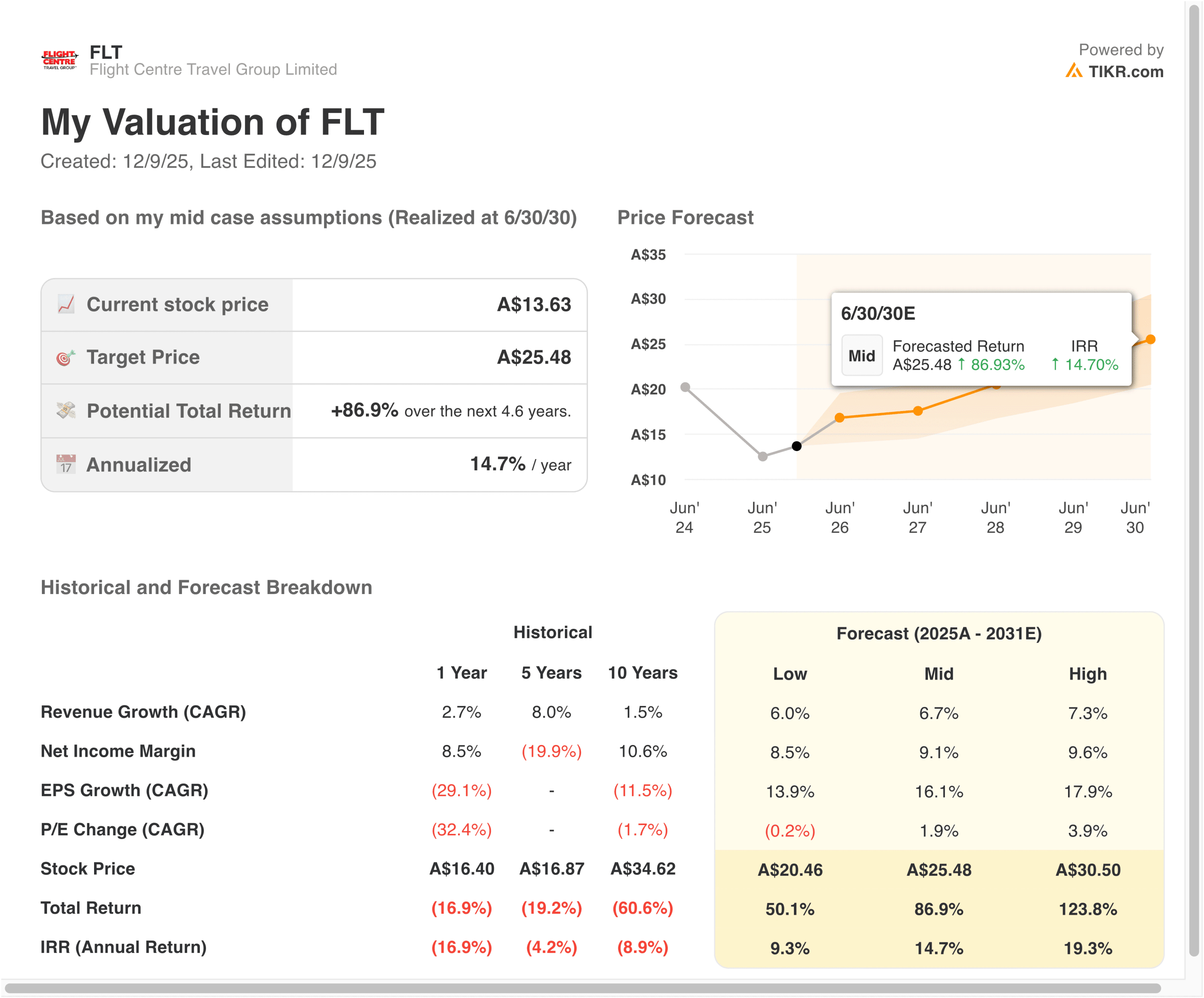

FLT delivered A$24.5 billion in TTV for FY25, a 3 percent increase in a volatile travel environment. Underlying profit before tax reached A$289.1 million, landing near the midpoint of guidance, though still below FY24 due to weakness in Asia and the Middle East conflict impacting peak-season bookings. The statutory PBT came in at A$213 million, reflecting softness late in the year and reduced supplier override income.

| Metric | FY25 Result |

|---|---|

| Total Transaction Value | A$24.5 billion |

| Underlying Profit Before Tax (UPBT) | A$289.1 million |

| Statutory PBT | A$213 million |

| Corporate TTV | A$12.3 billion |

| Leisure TTV | A$11.8 billion |

| Final Dividend | A$0.29 per share |

| Capital Returned in FY25 | A$450 million |

Corporate performance remained a relatively bright spot as well. TTV reached A$12.3 billion, with Corporate Traveller and FCM showing continued momentum, especially in the Americas, where Corporate Traveller reported more than 20 percent TTV growth in July 2025 alone. Excluding Asia’s losses, corporate profit improved, supported by productivity gains and growing adoption of digital platforms like Melon and FCM’s enhanced AI-driven tools.

The leisure division generated A$11.8 billion in TTV, up 6.7 percent year over year. Lower-margin brands drove most of the growth, while Flight Centre’s core brand saw modest gains tied to higher basket size. Independent agents and online channels delivered nearly A$4 billion in TTV at leaner staffing levels, highlighting improved operational efficiency. Despite short-term regional pressures, the division positioned itself for future upside through expanded cruise offerings and a new loyalty initiative slated for FY26.

Look up Flight Centre Travel Group’s full financial results & estimates (It’s free)>>>

Broader Market Context

Travel stocks globally spent much of 2025 absorbing the effects of geopolitical unrest, uneven consumer sentiment, and sharp swings in travel demand. Airline partners faced a mix of higher operating costs and shifting regional bookings, which pushed travel agencies to adapt quickly. At the same time, corporate travel continued to normalize, with many companies regaining confidence in international travel budgets and prioritizing more flexible, tech-enabled service models.

The broader sector has shown that resilient operators with digital capabilities, diversified offerings, and leaner cost structures are best positioned for the next phase of the cycle. FLT’s 2026 setup reflects this pattern, as the company leans more heavily on its corporate strength and product investments while waiting for leisure demand to stabilize.

1. Corporate Momentum and Digital Scale

FLT has spent several years reshaping its corporate business into a more scalable, technology-driven platform. That strategy paid off again in FY25, with both Corporate Traveller and FCM continuing to win large accounts and expand their addressable markets. The Melon platform drove stronger adoption and reinforced FLT’s reputation for modern digital infrastructure that supports fast-growing SME and mid-market clients.

The company’s push into AI-enabled workflows is a competitive advantage. FCM’s upgraded travel assistant, Sam, now automates a range of traveler support functions, and the Productive Operations program has improved request handling and consultant efficiency. These capabilities are likely to become even more valuable as enterprises look for providers that can improve service levels while managing travel budgets more tightly.

Corporate Traveller’s performance in North America offers another positive signal. With more than 20 percent TTV growth in July and record monthly sales, the brand is gaining share in one of the world’s most profitable travel markets. If FLT can sustain this trajectory, the corporate segment could be a more prominent earnings engine heading into FY26.

2. Leisure Recovery Potential and New Growth Engines

While FLT’s leisure business faced a challenging year, several long-term strengths became more visible. Independent agents and digital channels played a larger role in generating TTV, enabling the group to expand revenue with far fewer employees than pre-pandemic staffing levels. These channels provide FLT with operating leverage as demand accelerates, allowing the business to serve customers across more markets without significant cost increases.

Investments in cruise and luxury travel also position the leisure division for stronger performance in FY26. The relaunch of Cruiseabout in Australia and the expansion of UK cruise offerings represent meaningful growth areas, even as these businesses currently operate at modest losses. Management expects them to become solid profit contributors as booking cycles normalize.

The upcoming loyalty program could be a turning point for the entire leisure ecosystem. By centralizing rewards across Flight Centre, Travel Associates, and Cruiseabout, FLT is creating a framework that boosts retention, expands customer data insights, and strengthens supplier partnerships. If consumer confidence continues to improve, this program may accelerate the shift in revenue mix toward higher-margin offerings.

Value stocks like Flight Centre Travel Group in less than 60 seconds with TIKR (It’s free) >>>

3. Cost Discipline, AI Integration, and 2026 Outlook

Management placed strong emphasis on cost control heading into FY26, targeting flat underlying expenses through productivity gains and targeted reductions in certain areas. Capital expenditure will be reduced by 15 to 20 percent, enabling the company to invest more selectively in initiatives across AI, loyalty, and high-performing travel categories.

AI integration remains one of FLT’s most critical long-term drivers. The company has already saved tens of thousands of hours through AI-powered request routing and intends to apply advanced tools to more customer-facing applications, including trip planning and personalized recommendations. These capabilities should help offset wage inflation and improve consultant effectiveness.

As for the near-term outlook, management expects continued volatility early in FY26 before booking behavior stabilizes and seasonal demand strengthens. Early indicators such as rising web traffic, stronger corporate TTV, and improving consumer sentiment suggest the travel cycle may be turning. If geopolitical pressures ease and operators regain pricing traction, FLT could see margin improvement as the year progresses.

The TIKR Takeaway

Flight Centre Travel Group is navigating a complex travel environment, but its long-term setup looks more constructive than its FY25 results suggest. Corporate momentum, expanding digital tools, and improving productivity form a solid foundation.

The leisure division needs better conditions to fully recover, but structural upgrades and a new loyalty program provide fresh growth levers. TIKR data shows the company has meaningful upside potential if 2026 brings a steadier travel cycle and management’s cost efforts continue to take hold.

Should You Buy, Sell, or Hold Flight Centre Travel Group Stock in 2025?

FLT presents a nuanced investment case heading into 2026. The stock still carries some uncertainty given regional volatility and shifting travel patterns, yet the company’s corporate strength and improving operational model offer compelling reasons to stay constructive.

For investors who believe the travel cycle will normalize and AI-driven efficiencies will unlock margin benefits, FLT looks like a name worth watching closely, especially at current valuation levels. A balanced stance makes sense until evidence of a sustained recovery becomes clearer.

How Much Upside Does Flight Centre Travel Group Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

Find out what your favorite stocks are really worth (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!