The Campbell’s Company (NYSE: CPB) has faced a challenging stretch. Shares trade near $30/share, down about 37% over the past year as slowing soup sales and weaker volumes have weighed on results. Consumers are pulling back on packaged foods, forcing Campbell’s to rely more on pricing and cost discipline to protect margins.

Recently, the company completed its Sovos Brands acquisition, bringing premium labels like Rao’s Homemade into its portfolio to strengthen its sauces and frozen meals segment. Campbell’s also reaffirmed its cost-saving goals and said synergies from the deal should begin to flow through in fiscal 2026. However, management noted that near-term demand remains soft as consumers remain cautious and competition in grocery aisles intensifies.

This article looks at where Wall Street analysts think Campbell’s could trade by 2028. Using consensus price targets and TIKR’s Guided Valuation Model, we break down what the next few years could look like for investors and whether this classic food stock still has room to rebound.

Unlock our Free Report: 5 AI compounders that analysts believe are undervalued and could deliver years of outperformance with accelerating AI adoption (Sign up for TIKR, it’s free) >>>

Analyst Price Targets Suggest Modest Upside

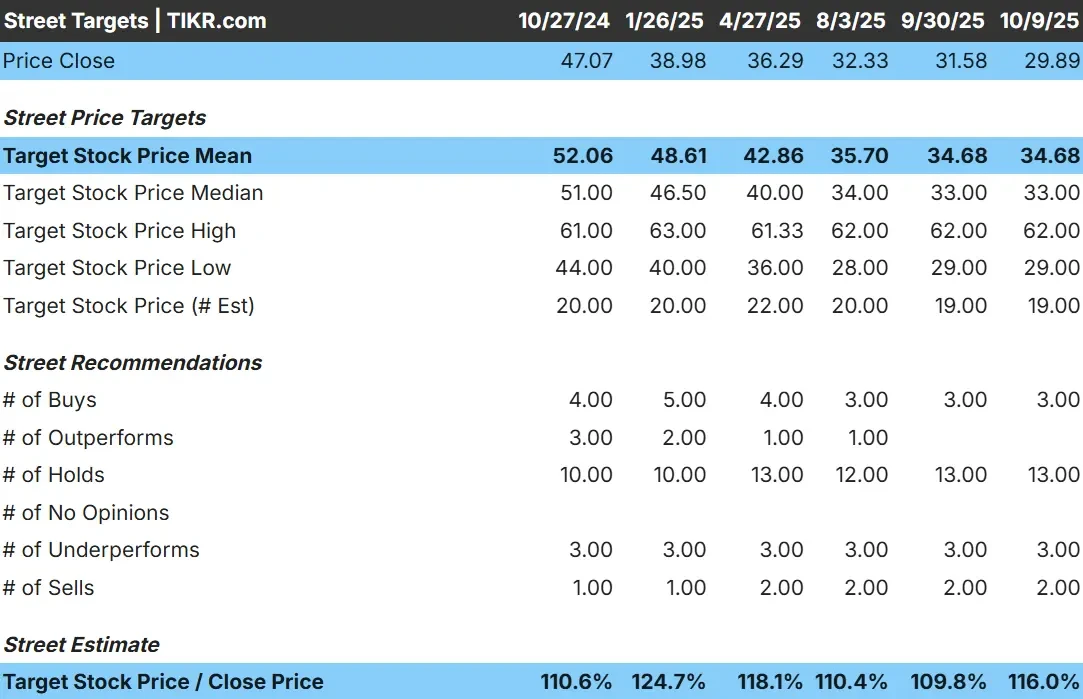

Campbell’s trades at about $30/share today. The average analyst price target is $35/share, which points to about 17% upside over the next year. Forecasts are closely grouped and reflect cautious sentiment:

- High estimate: $62/share

- Low estimate: $29/share

- Median target: $33/share

- Ratings: 3 Buys, 3 Outperforms, 13 Holds, 3 Underperforms, 2 Sells

For investors, this suggests most analysts expect the stock to stay in a tight range. Upside looks modest unless Campbell’s can drive stronger volumes or improve margins more than expected.

See analysts’ growth forecasts and price targets for Campbell (It’s free!) >>>

Campbell’s: Growth Outlook and Valuation

The company’s fundamentals appear steady, but not particularly strong:

- Revenue CAGR (to 2028): ~0%

- Operating Margin: ~13.4%

- Shares trade at: ~12× forward earnings, close to their long-term average

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a forward P/E of 13× suggests ~$38/share by 2028

- That implies about 27% upside, or roughly 9% annualized returns

These figures suggest Campbell’s is a stable, income-focused stock rather than a growth play. Its valuation already reflects consistent margins and dependable cash generation, leaving limited room for a major re-rating.

For investors, the appeal lies in the 5.4% dividend yield and the company’s defensive nature. Campbell’s may not deliver rapid growth, but it offers reliability and steady income for long-term holders seeking lower volatility.

Value stocks like Campbell in as little as 60 seconds with TIKR (It’s free) >>>

What’s Driving the Optimism?

Campbell’s remains one of the most recognized names in packaged foods. Its focus on efficiency, pricing, and product innovation continues to support stable margins despite weak consumer volumes.

The recent Sovos Brands acquisition adds premium products like Rao’s, which could help Campbell’s tap into higher-growth food categories beyond soup. Management also expects meaningful cost synergies to start in fiscal 2026, supporting steady profit expansion even without major revenue growth.

For investors, these initiatives show that Campbell’s still has tools to protect earnings and maintain cash flow. If execution on integration and cost discipline stays strong, the stock could gradually recover from recent lows.

Bear Case: Sluggish Growth and Leverage

Even with these positives, Campbell’s faces a long road to reigniting growth. Sales remain flat, and pricing strength is masking persistent volume declines. With consumer demand normalizing after inflation, it is unclear whether Campbell’s can return to consistent top-line growth.

The company’s Net Debt-to-EBITDA ratio near 3.0× also limits flexibility for major acquisitions or aggressive buybacks. Meanwhile, competition from private-label brands is intensifying, forcing Campbell’s to defend market share while managing costs.

For investors, the key risk is that Campbell’s steady margins may not translate into earnings growth. Without stronger consumer trends or innovation-driven demand, the stock could remain stuck near current levels.

Outlook for 2028: What Could Campbell’s Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model suggests Campbell’s could trade near $38/share by 2028. That represents about a 27% total return, or roughly 9% annualized gains from today’s price.

This forecast assumes flat revenue and stable margins, so it already bakes in moderate optimism. Stronger upside would require a clear turnaround in volumes, successful integration of Sovos Brands, and faster debt reduction.

For investors, Campbell’s looks like a dependable income stock rather than a growth opportunity. The 5.4% dividend yield provides a steady return base, but capital appreciation will likely be gradual. Long-term holders may view it as a safe, slow compounder rather than a high-upside play.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Click here to sign up for TIKR and get your free copy of TIKR’s 5 AI Compounders report today.