Key Stats for Boeing Stock

- YTD Price Change for Boeing stock: 25%

- Current Share Price: $214

- 52-Week High: $242

- $BA Stock Price Target: $253

What Happened?

Yesterday, Boeing (BA) reported 55 aircraft deliveries in September, marking its strongest performance for the month since 2018. More importantly, momentum is building as production stabilizes and CEO Kelly Ortberg’s turnaround plan begins to yield tangible results.

Boeing handed over 40 of its 737 MAX jets, including 10 to Ryanair, which marked the company’s 2,000th MAX delivery, a symbolic milestone.

It also delivered 14 widebody aircraft, including seven 787 Dreamliners. For the first nine months of 2025, Boeing has delivered 440 aircraft compared to just 348 for all of 2024. This recovery in aircraft deliveries has driven Boeing stock higher by 25% in 2025.

Boeing also booked 96 gross orders in September, including 30 737 MAXs for Norwegian Airlines, 50 787 Dreamliners for Turkish Airlines, and 14 787x for Uzbekistan Airways. After adjustments and cancellations, net orders came to 95, keeping the backlog strong at 5,987 aircraft.

Norwegian’s purchase represents their first direct Boeing order since 2017, showing renewed confidence in the manufacturer.

Turkish Airlines’ decision to double down on both the 787 and potentially order 150 more MAXs demonstrates that major carriers see Boeing as a long-term winner despite recent troubles.

The FAA also provided a tailwind by easing restrictions on Boeing’s certification authority. Starting September 29, Boeing can once again perform some final safety checks on 737 MAX and 787 jets—something they’ve been prohibited from doing since the 2019 crashes for the MAX and 2022 quality issues for the 787.

While Boeing and the FAA will alternate weeks and oversight remains “direct and rigorous,” this change removes a significant bottleneck in the delivery process.

At a Morgan Stanley conference last month, Ortberg confirmed Boeing is on track to reach 42 MAXs per month by year-end, up from the current 38-per-month cap imposed by the FAA.

The company has been producing at 38 per month and maintaining stability at that rate while implementing the Safety & Quality Plan required by regulators.

See analysts’ growth forecasts and price targets for Boeing stock (It’s free!) >>>

What the Market Is Telling Us About Boeing Stock

The reaction to Boeing stock in 2025 indicates that investors are finally recognizing evidence of a genuine turnaround, rather than just rhetoric.

Ortberg relocated his office to the Seattle production floor so he can see which planes are moving and which aren’t every single morning.

He implemented a “One Boeing” incentive program to eliminate the siloed mentality where business units competed against each other.

The CEO is refusing to push production rate increases unless the metrics justify it, saying “a month will not matter in the big scheme of things and losing stability will matter.”

The supply chain is also in better shape than investors might think. Boeing has been keeping key suppliers producing at higher rates to build an inventory buffer.

Beyond 737, the 787 program has a clear path to double-digit production rates with strong order demand supporting teens-level production. Boeing is investing in Charleston to expand capacity with completion targeted for 2028, which will be necessary to sustain rates above 10 per month.

The defense business is also stabilizing under new permanent leader Steve Parker. Boeing has been working with customers to restructure problematic fixed-price contracts, making progress on programs like T-7 and VC-25B.

The goal is getting back to high single-digit margins as development programs complete and the portfolio normalizes.

Trade tailwinds from the Trump administration’s focus on bilateral aircraft deals have created additional order momentum.

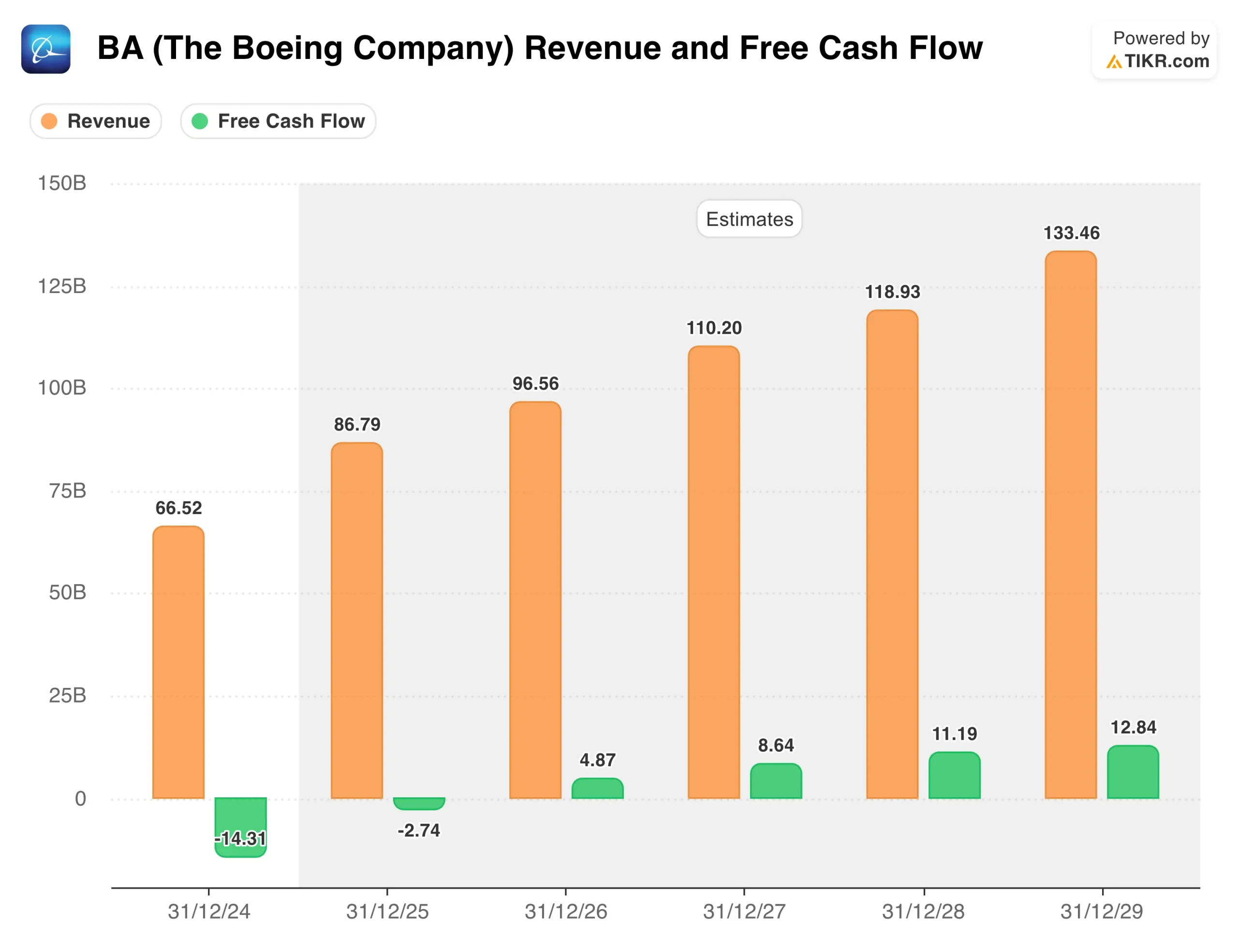

Looking ahead, Ortberg expects positive free cash flow in Q4 of 2025 after burning about $3 billion for the full year.

The company’s plan remains targeting $10 billion in annual free cash flow once production rates stabilize—50 per month on 737, 10 on 787, the 777X and MAX variants certified and ramping, and defense returning to mid-single-digit margins.

Ortberg said he sees “nothing structurally” preventing that outcome, though timing depends on execution.

The balance sheet priority is clear: pay down debt. Boeing took on too much during the crisis and needs to be solidly investment-grade before considering a next-generation aircraft program. As cash generation returns, debt reduction will be the focus.

The certification challenges on 777X remain concerning, with Ortberg calling it a “mountain of work” that’s falling behind schedule. Any delays create a significant financial impact given the reach-forward loss position.

But the aircraft and engine are performing well in flight testing without new technical issues—it’s the FAA certification process that’s the bottleneck.

For investors, today’s news reflects Boeing finally converting its massive backlog into deliveries and demonstrating the operational discipline needed to sustain higher production rates.

If the momentum continues and the FAA approves the rate increase to 42 per month, the financial recovery could accelerate faster than expected.

Wall Street Analysts Are Bullish on These 5 Undervalued Compounders With Market-Beating Potential

TIKR just released a new free report on 5 compounders that appear undervalued, have beaten the market in the past, and could continue to outperform on a 1-5 year timeline based on analysts’ estimates.

Inside, you’ll get a breakdown of 5 high-quality businesses with:

- Strong revenue growth and durable competitive advantages

- Attractive valuations based on forward earnings and expected earnings growth

- Long-term upside potential backed by analyst forecasts and TIKR’s valuation models

These are the kinds of stocks that can deliver massive long-term returns, especially if you catch them while they’re still trading at a discount.

Whether you’re a long-term investor or just looking for great businesses trading below fair value, this report will help you zero in on high-upside opportunities.

Click here to sign up for TIKR and get our full report on 5 undervalued compounders completely free.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!