Alcoa Corporation (NYSE: AA) has faced a challenging stretch as aluminum prices softened and global demand slowed. The stock trades near $37/share, down roughly 13% over the past year. Still, Alcoa’s strong balance sheet and ongoing cost discipline give it room to navigate this period of pricing pressure.

Recently, the company announced a $2.2 billion all-stock merger with Alumina Limited, a move designed to simplify its corporate structure and improve control over global bauxite and alumina assets. Alcoa also restarted key smelting capacity in Norway and Spain, signaling confidence in long-term aluminum demand tied to electric vehicles and renewable infrastructure. These actions show that management is taking proactive steps to strengthen the company’s competitive position.

This article explores where Wall Street analysts expect Alcoa’s stock to trade by 2027. We’ve combined consensus price targets and TIKR’s valuation model to outline potential upside and risks ahead. These figures reflect current analyst estimates and are not TIKR’s own predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Modest Upside

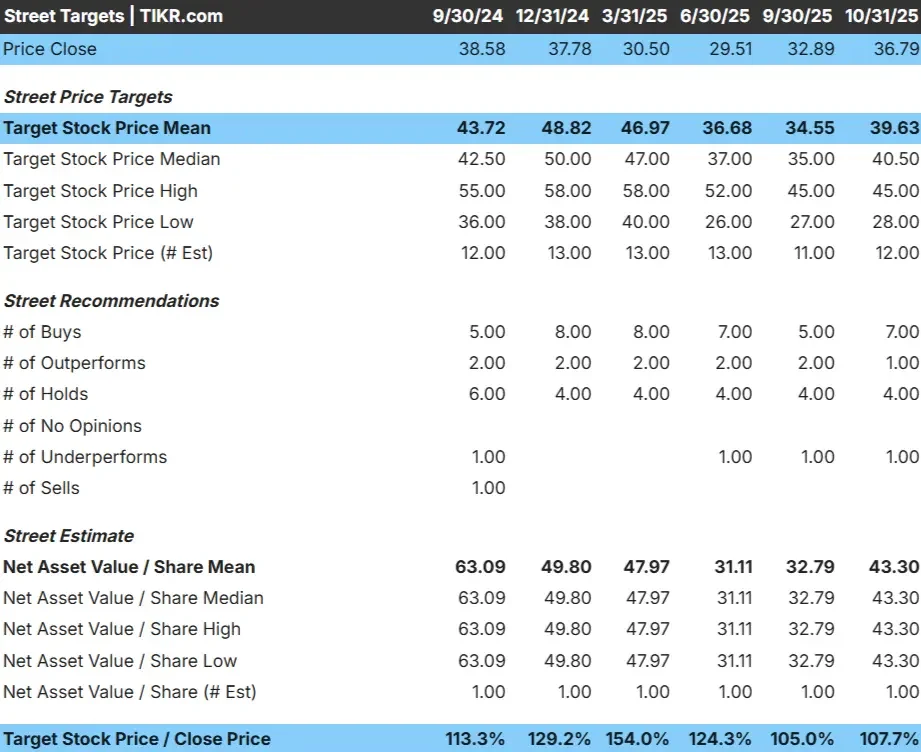

Alcoa trades near $37/share today. The average analyst price target is $40/share, suggesting roughly 8% upside over the next year.

- High estimate: ~$45/share

- Low estimate: ~$28/share

- Median target: ~$41/share

- Ratings: 7 Buys, 2 Outperforms, 6 Holds, 1 Sell

Analysts see modest upside as aluminum prices stabilize and cost controls take hold. For investors, this means Alcoa could outperform if commodity prices recover or global demand strengthens, but the near-term story remains cautious given slower industrial activity.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

Alcoa: Growth Outlook and Valuation

The company’s fundamentals are improving, but not rapidly enough to spark a major re-rating:

- Revenue is projected to grow about 3.7% annually through 2027

- Operating margins are expected to recover to around 11.6%

- Shares trade at roughly 10.5x forward earnings, slightly below historical averages

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 10.5x forward P/E suggests around $33/share by 2027

- That implies about 10% downside, or roughly –4.6% annualized

For investors, this points to limited near-term return potential. The market appears to already price in gradual margin recovery, meaning stronger aluminum prices or cost improvements would be needed to unlock meaningful upside.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

Alcoa remains one of the world’s most efficient aluminum producers, supported by a vertically integrated structure that spans mining, refining, and smelting. This gives the company strong control over costs and supply. Its disciplined approach to capital spending and energy efficiency has helped preserve margins even in a volatile pricing environment.

Long-term demand tailwinds are another positive. Aluminum is a key input for electric vehicles, renewable energy, and lightweight construction, all of which are expected to grow meaningfully over the next decade. For investors, these factors show that Alcoa’s fundamentals remain intact, positioning it well for an eventual recovery in global industrial activity.

Bear Case: Pricing Pressure and Volatility

Even with these strengths, Alcoa’s earnings are highly exposed to commodity cycles. Slower industrial demand from China and persistent global oversupply continue to pressure aluminum prices. Margins could remain constrained if energy costs rise or smelting capacity expands faster than demand.

For investors, this means Alcoa’s upside potential depends on external forces it cannot fully control. While the company’s balance sheet is strong, volatility is likely to remain a defining feature of its earnings profile in the near term.

Outlook for 2027: What Could Alcoa Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 10.5x forward P/E suggests Alcoa could trade near $33/share by 2027. That would represent roughly 10% downside from current levels.

For investors, this implies the stock is fairly valued given current market conditions. To outperform, Alcoa would need a sustained rebound in aluminum prices or stronger global demand from industrial sectors. Otherwise, the stock is likely to remain a steady but cyclical holding rather than a high-growth opportunity.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>