Compounding machines often share a common trait: they don’t need heavy factories, massive inventories, or billions in capital expenditures to grow.

Instead, they run “asset-light” business models, where most of the value comes from intellectual property, software, networks, or services rather than physical assets.

This model can be especially powerful in finance, where companies can scale revenues without tying up much balance sheet capital. The result is high returns on invested capital (ROIC), strong free cash flow conversion, and the ability to reinvest in growth or return cash to shareholders.

In this article, we’ll look at five asset-light financial compounders that consistently generate 20%+ ROIC. These businesses have proven they can reinvest at high rates, expand their competitive moats, and reward long-term shareholders with attractive compounding potential.

| Company Name (Ticker) | Analyst Upside | P/E Ratio |

| Visa (V) | 12.2% | 28.15 |

| Mastercard (MA) | 8.5% | 33.71 |

| Fair Isaac (FICO) | 33.0% | 42.39 |

| MSCI Inc. (MSCI) | 8.1% | 31.70 |

| S&P Global (SPGI) | 12.4% | 30.33 |

Unlock our Free Report: 5 undervalued compounders with upside based on Wall Street’s growth estimates that could deliver market-beating returns (Sign up for TIKR, it’s free) >>>

Growing international interest highlights the scalability of their models and the global relevance of their advantages. For investors seeking resilience and long-term wealth creation, these companies stand out as top favorites among today’s most compelling opportunities.

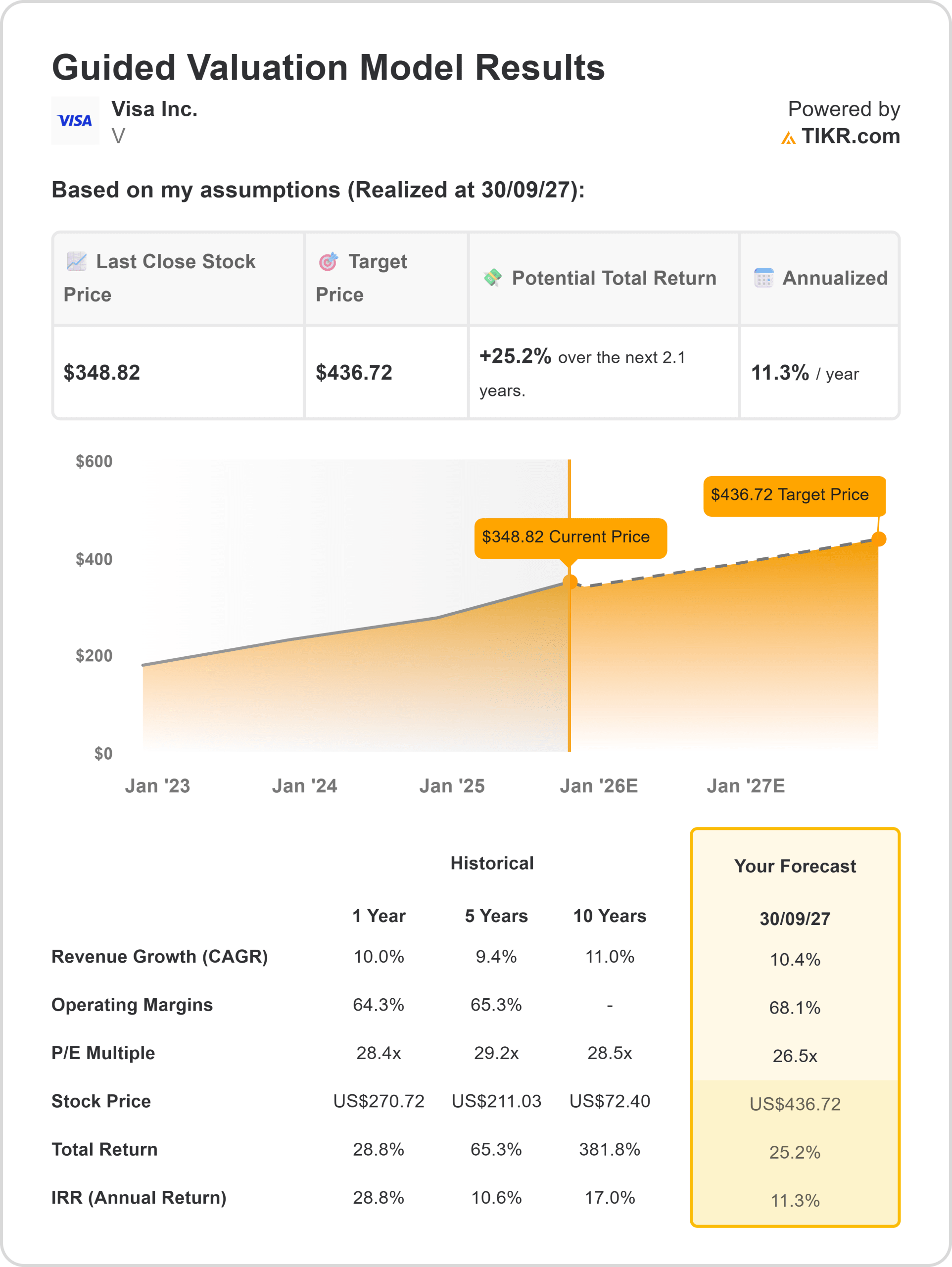

Visa Inc. (V)

Visa is the prototype asset-light compounder: it doesn’t underwrite loans or hold inventory it operates a payments network that connects cardholders, issuers and merchants and collects fees on transaction volume.

That business structure produces very high incremental margins because each additional swipe mostly adds revenue without meaningful incremental invested capital; the company’s ROIC sits well above the 20% threshold in recent TTM calculations.

What makes that return durable is a two-sided network effect (more merchants → more card acceptance → higher card usage → more issuer distribution), massive scale across geographies, and growing value-added services (tokenization, data services, B2B rails) that lift take-rates without materially increasing fixed capital.

Visa converts a large share of revenue into free cash flow, which it returns via buybacks and selective M&A, reinforcing per-share economics rather than raising the company’s capital base.

Regulation, interchange pressure, or alternative rails (real-time payments / new rails) are the principal risks, but Visa’s scale, entrenched processing relationships, and data advantages make it one of the cleanest asset-light 20%+ ROIC

Value any stock in under 30 seconds with TIKR’s new Valuation Model (it’s free) >>>

Mastercard (MA)

Mastercard’s economics are structurally similar to Visa’s, a high-take, low-capex payments network that benefits from two-sided network effects and strong operating leverage. Empirical ROIC/ROC metrics show Mastercard running materially above 20% historically, because the company doesn’t carry consumer credit risk and its model converts transaction volume to fee revenue; incremental volumes flow almost straight to the bottom line once fixed costs are covered.

Mastercard also leverages product diversification (data & analytics, enterprise software, cross-border, tokenization) to raise revenue per transaction and reduce sensitivity to cyclical merchant volumes.

That gives the firm multiple durable levers to sustain high returns: pricing power through productized services, continuous tech investment (not heavy physical capex), and capital allocation that compounds returns via buybacks.

Regulatory scrutiny and merchant/issuer pricing battles are the main threats, but Mastercard’s long track record of high ROC/ROIC and low incremental capital intensity makes it a textbook asset-light.

Find stocks that we like even better than Mastercard today with TIKR (It’s free) >>>

Fair Isaac (FICO)

Fair Isaac is an asset-light, data-platform compounder built on an industry standard (credit scores) and a broader decision-analytics suite. Its revenues are heavily recurring (scores, subscriptions, decisioning software), margins are high, and measured ROIC figures have been well north of the 20% bar in multiple public datasets, reflecting the very low invested capital required to scale scoring and cloud software.

The business captures value through pricing power (lenders and large enterprises tolerate fees for an accepted, regulatory-backed benchmark) and extraordinary operating leverage once models and data pipelines are in place.

The moat logic here is classic data + regulatory path-dependence: FICO’s scores are embedded into lenders’ underwriting, regulatory defenses (and customer inertia) make switching costly, and the firm’s proprietary data and models improve as usage grows, creating a rising-return dynamic.

Risks include regulatory scrutiny around fairness/transparency, potential competitive scoring models, and pressure if lenders adopt alternative decision engines.

Value stocks like Fair Isaac quicker with TIKR >>>

Wall Street Analysts Are Bullish on These 5 Undervalued Compounders With Market-Beating Potential

TIKR just released a new free report on 5 compounders that appear undervalued, have beaten the market in the past, and could continue to outperform on a 1-5 year timeline based on analysts’ estimates.

Inside, you’ll get a breakdown of 5 high-quality businesses with:

- Strong revenue growth and durable competitive advantages

- Attractive valuations based on forward earnings and expected earnings growth

- Long-term upside potential backed by analyst forecasts and TIKR’s valuation models

These are the kinds of stocks that can deliver massive long-term returns, especially if you catch them while they’re still trading at a discount.

Whether you’re a long-term investor or just looking for great businesses trading below fair value, this report will help you zero in on high-upside opportunities.

Click here to sign up for TIKR and get our full report on 5 undervalued compounders completely free.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!