Key Takeaways:

- Scotts Miracle-Gro delivered exceptional point-of-sale performance, achieving 12.1% unit growth through the first half of fiscal 2025, which demonstrates strong consumer demand across key categories.

- The company reaffirmed its full-year guidance, with EBITDA expected to be between $570 million and $590 million, reflecting significant progress in margin recovery and operational efficiency.

- Management announced the successful completion of $75 million in supply chain cost savings for fiscal 2025, with an additional $75 million targeted for completion by the end of fiscal 2027.

- Get accurate financial data on over 100,000 global stocks for free on TIKR >>>

Valued at a market capitalization of $3.75 billion, The Scotts Miracle-Gro Company (SMG) operates as the leading provider of branded do-it-yourself lawn and garden products in the United States.

It maintains a comprehensive portfolio including lawn fertilizers, grass seed, garden soils, mulch, and control products through iconic brands such as Scotts, Miracle-Gro, Ortho, and Tomcat.

After underperforming the broader markets in recent years, SMG stock should demonstrate resilience amid challenging market conditions. The company is executing a comprehensive transformation strategy that positions it for sustainable growth and margin expansion.

The strong operational performance in fiscal 2025 (ending in September) reflects management’s disciplined approach to cost reduction, strategic brand investments, and supply chain optimization.

Scotts Miracle-Gro’s ability to maintain pricing power while driving volume growth showcases the strength of its market-leading brands and distribution advantages.

Let’s explore why you should consider adding this mid-cap stock to your equity portfolio today.

1. SMG Stock Benefits from Exceptional Demand

SMG stock benefits from robust consumer engagement as evidenced by its outstanding point-of-sale performance during the first half of fiscal 2025.

Consumer takeaway units increased 12.1% year-over-year, with robust performance in garden products growing 16% and the mulch business surging 46%.

The Tomcat and Ortho outdoor insect control brands each achieved 14% unit growth, indicating broad-based strength across their respective product portfolios.

SMG’s lawn care business showcased encouraging momentum, with total lawn products experiencing 4% unit growth, marking an improvement from previous declining trends.

This turnaround reflects management’s strategic shift to multi-feeding programs that educate consumers on the benefits of regular lawn applications throughout the growing season.

The Turf Builder Halts product, representing the first step in multi-feeding programs, increased 67% through the first half.

Scotts Miracle-Gro’s expansion into organic and natural products continues to gain traction, with management highlighting strong year-to-date momentum in the organic soil and plant food categories.

Its exclusive Costco Max line and expanded Miracle-Gro organic offerings, endorsed by Martha Stewart, have contributed meaningfully to revenue growth and category expansion.

Check out SMG’s full analyst estimates and growth forecast (It’s free) >>>

2. The Mid-Cap Stock Is Supported by Margin Recovery

The SMG stock price is yet to reflect investor confidence in its remarkable gross margin recovery trajectory.

Scotts Miracle-Gro achieved nearly 500 basis points of gross margin improvement through the first half, positioning the company to reach its 30% gross margin target by the end of the fiscal year.

This represents significant progress from the low-to-mid 20% levels experienced during the pandemic period.

SMG’s transformation initiative has delivered substantial results, with approximately two-thirds of the planned $75 million in supply chain cost savings already realized through the first half.

These improvements stem from increased automation, enhanced asset utilization, and strategic negotiations with vendors. Management’s commitment to achieving an additional $75 million in cost savings over the next two fiscal years provides clear visibility for continued margin expansion.

Scotts Miracle-Gro’s investment in supply chain modernization has created competitive advantages, particularly in e-commerce fulfillment capabilities.

It shipped approximately 12 million units directly to consumers year-to-date, compared to six million units in the prior year, reflecting strong growth in online marketplace participation. E-commerce now represents nearly 10% of total revenue, up from 8% in the previous year.

Find the best stocks to buy today with TIKR. (It’s free) >>>

3. A Focus on Balance Sheet Improvement

SMG stock gains support from management’s disciplined approach to capital allocation and balance sheet strengthening.

It reduced leverage to 4.41x net debt-to-adjusted EBITDA, showcasing meaningful progress toward the target leverage of 3.5x or below by fiscal 2027. Interest expense decreased $17 million year-to-date due to lower debt balances and more favorable interest rates.

Management’s plan to divest the Hawthorne Gardening business represents a strategic simplification to enhance focus on the core consumer lawn and garden franchise.

The divestiture is expected to accelerate tax benefits of up to $100 million over the next few years while eliminating cannabis-related banking complications. Hawthorne achieved EBITDA-positive results for two consecutive quarters, positioning it attractively for potential buyers.

SMG’s commitment to shareholder-friendly capital allocation includes plans to resume dividend payments and share repurchases once leverage targets are achieved.

Free cash flow generation of approximately $250 million provides substantial capacity for debt reduction and eventual capital returns. Management’s conservative approach to leverage and M&A reflects lessons learned from previous acquisition experiences.

Valuation Setup for SMG Stock

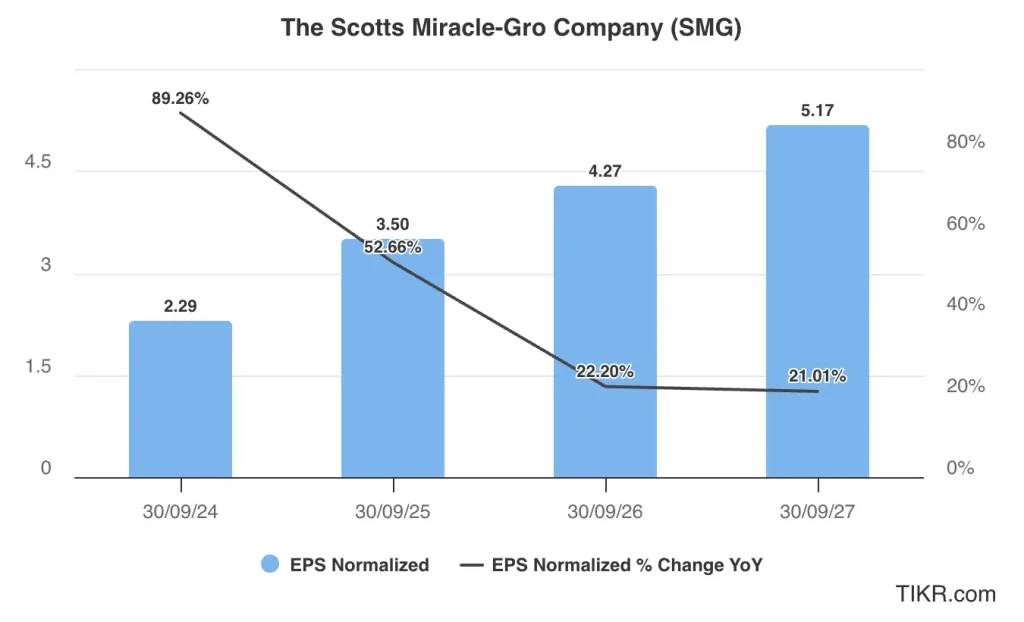

Analysts tracking SMG stock expect its sales to rise from $3.55 billion in fiscal 2024 to $3.58 billion in fiscal 2027, a relatively modest increase. Comparatively, adjusted earnings are forecast to expand from $2.29 per share to $5.17 per share in this period.

SMG stock currently trades at a forward price-to-earnings multiple of 17x, which is above its five-year average multiple of 21x.

If the mid-cap stock is priced at a multiple of 17x and reaches its projected $5.17 in normalized EPS, it will trade around $88/share in early 2027, indicating an upside potential of 35% from current levels.

Value stocks quicker with TIKR (It’s free, no card required) >>>

Average Analyst Price Target for SMG Stock

While Wall Street remains bullish on SMG stock, with a consensus price target of $70/share, analysts expect the stock to rise around 8% from current levels.

This really isn’t a lot of upside. However, the mid-cap stock would likely surpass these price targets if it can meet consensus earnings forecasts through fiscal 2027.

Notably, SMG stock currently has a high target price of $90 and a low target price of $54.

Of the 11 analysts tracking the mid-cap stock, eight recommend “Buys”, and three recommend “Hold.” There are no “Sell” recommendations for the stock in June 2025.

TIKR Takeaway for SMG Stock

SMG stock represents a compelling turnaround story as Scotts Miracle-Gro executes a comprehensive transformation strategy while maintaining its leadership position in essential consumer categories.

Its dominant market share, trusted brands, and extensive retail relationships create sustainable competitive advantages that support pricing power and market expansion opportunities.

Trading at attractive valuations relative to its recovery potential, SMG stock offers exposure to the resilient lawn and garden category, which consumers view as a necessity for spending.

A focus on operational excellence, margin expansion, and balance sheet improvement creates multiple pathways for value creation as management executes its strategic roadmap toward financial targets and enhanced shareholder returns.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!